Can Kaltura (KLTR) Narrowing Losses Reshape Its Path to Sustainable Profitability?

- Kaltura, Inc. recently reported its third-quarter 2025 results, showing revenue of US$43.87 million and a reduced net loss of US$2.63 million, alongside issuing updated guidance for the year and confirming no additional share repurchases in the recent quarter.

- A key insight from these announcements is the narrowing of Kaltura’s net loss year-over-year and modest nine-month revenue growth, suggesting some progress in controlling costs and supporting overall financial stability.

- We’ll examine how the improvement in net loss and updated full-year revenue guidance may influence Kaltura’s current investment narrative.

We've found 15 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

Kaltura Investment Narrative Recap

For investors considering Kaltura, the primary thesis centers on the company’s ability to reduce losses, stabilize earnings, and capture growth as organizations adopt AI-driven video platforms. The recent quarterly report shows improved net loss and modest revenue growth but only marginally impacts the short-term catalyst of bookings acceleration from new AI products, while persistent customer concentration risk remains front and center and is largely unaddressed by this update.

The updated full-year revenue guidance of US$180.3 million to US$181.0 million is most relevant to current investors, clarifying expectations for near-term performance. With losses narrowing but little shift in overall top-line momentum, this guidance provides some visibility into Kaltura’s execution but does not alleviate concerns about larger structural pressures facing the business.

However, investors should be especially aware that despite visible progress on costs, the risk of a sudden revenue setback from major client changes is...

Read the full narrative on Kaltura (it's free!)

Kaltura is projected to reach $209.7 million in revenue and $27.5 million in earnings by 2028. This outlook assumes a 5.0% annual revenue growth and a $46.6 million increase in earnings from the current $-19.1 million.

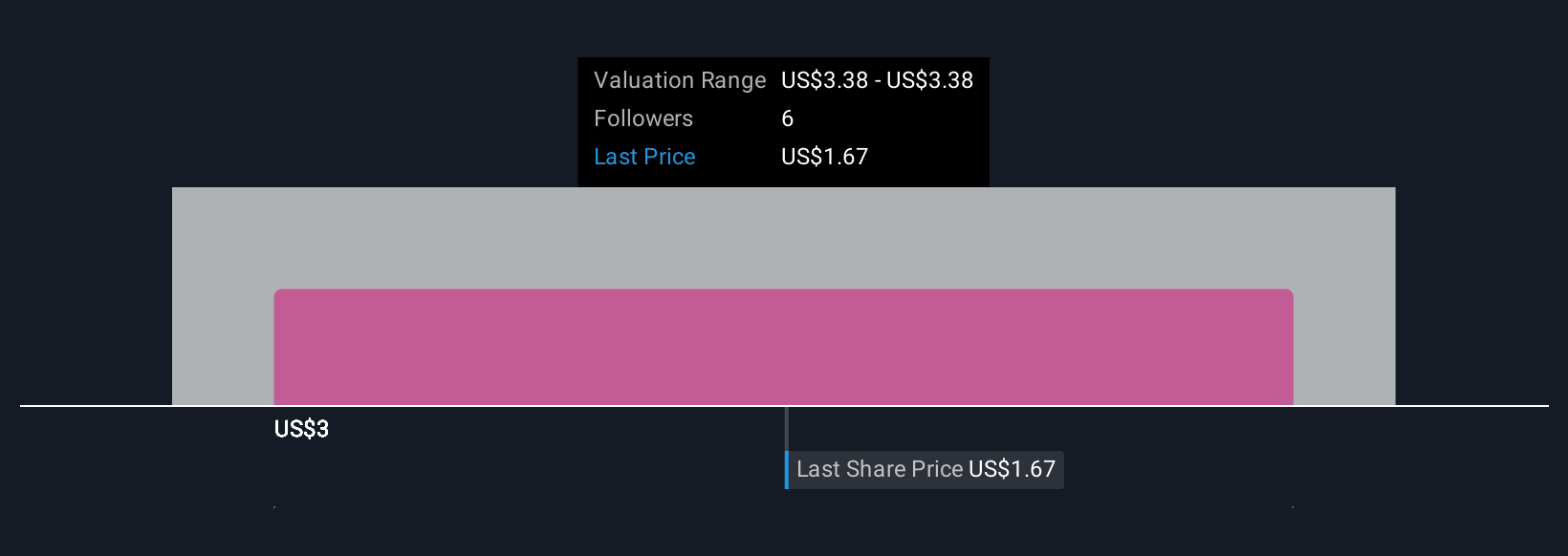

Uncover how Kaltura's forecasts yield a $3.38 fair value, a 89% upside to its current price.

Exploring Other Perspectives

Only one fair value estimate from the Simply Wall St Community puts Kaltura at US$3.38 per share. Persistent revenue concentration risk could affect future growth and profitability, highlighting why opinions can diverge, explore several viewpoints to understand all sides.

Explore another fair value estimate on Kaltura - why the stock might be worth just $3.38!

Build Your Own Kaltura Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Kaltura research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Kaltura research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Kaltura's overall financial health at a glance.

Searching For A Fresh Perspective?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- The end of cancer? These 29 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

- Find companies with promising cash flow potential yet trading below their fair value.

- These 15 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com