Weibo’s AI-Powered Profit Surge Might Change the Case for Investing in WB

- Weibo Corporation recently announced its third-quarter 2025 results, reporting US$442.31 million in revenue and US$221.09 million in net income, with earnings per share from continuing operations rising significantly year-over-year despite a decrease in overall revenue.

- This performance was shaped by increased AI integration to boost user and advertiser engagement, alongside sector-specific advertising growth in e-commerce and automotive, even as other categories and overall advertising revenue declined.

- We'll examine how Weibo's AI-driven product revamps and improved profitability could reshape its investment narrative and growth prospects.

We've found 16 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

Weibo Investment Narrative Recap

To be a Weibo shareholder, you would need to believe that increased AI integration and product innovation can drive user engagement and maximize advertising effectiveness, compensating for revenue pressures from competition and shifting client spending. The latest results do not dramatically change the most pressing near-term catalyst, AI-driven engagement growth, or address the ongoing risk of heavy reliance on advertising revenue, which remains pronounced despite profitability gains.

Weibo’s recent launch of an annual cash dividend policy stands out, reflecting management’s commitment to shareholder returns amidst earnings volatility. This move may enhance confidence even as advertising-driven volatility remains a key challenge.

Yet, in contrast, investors should be aware of the persistent revenue instability tied to cyclical advertising spend and how this risk could…

Read the full narrative on Weibo (it's free!)

Weibo's outlook anticipates $1.9 billion in revenue and $416.6 million in earnings by 2028. This reflects a forecast annual revenue growth rate of 2.8% and an earnings increase of $44.5 million from current earnings of $372.1 million.

Uncover how Weibo's forecasts yield a $11.96 fair value, a 24% upside to its current price.

Exploring Other Perspectives

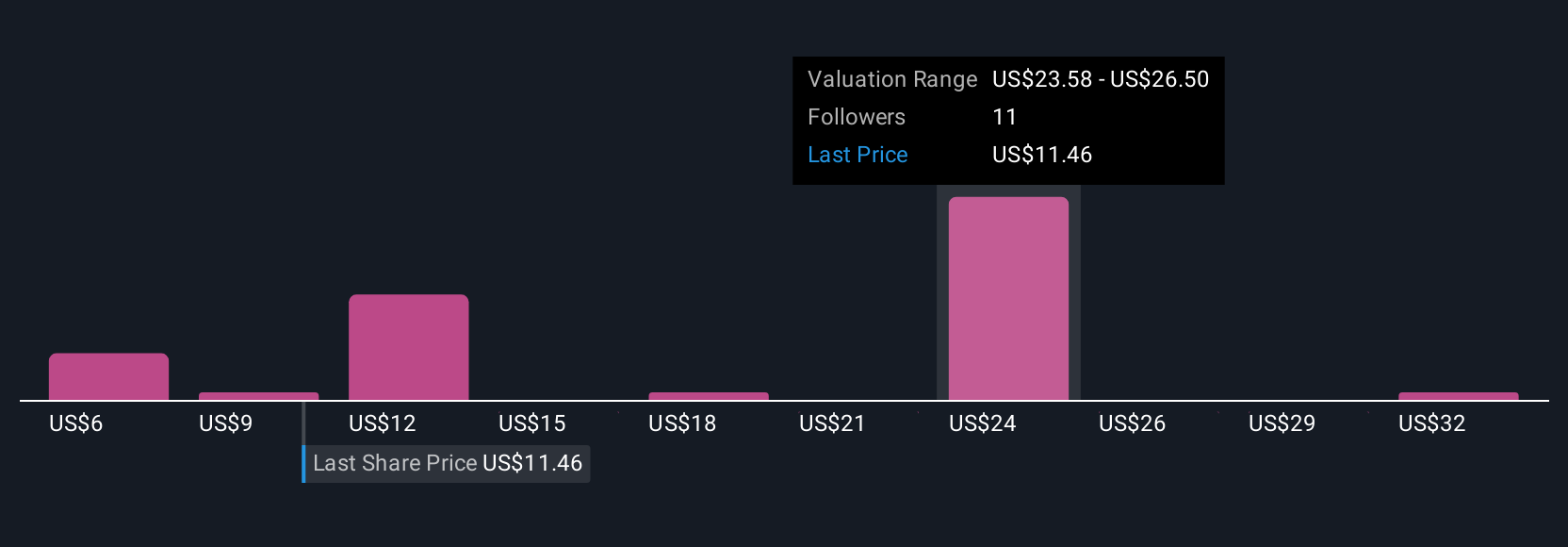

Simply Wall St Community valuations for Weibo swing from US$6.08 to US$35.25 across 9 perspectives. With ongoing AI investments aimed at boosting engagement, you are encouraged to consider how such a wide range of views could shape your opinion on the company’s potential.

Explore 9 other fair value estimates on Weibo - why the stock might be worth over 3x more than the current price!

Build Your Own Weibo Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Weibo research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Weibo research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Weibo's overall financial health at a glance.

Interested In Other Possibilities?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

- The end of cancer? These 29 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

- Trump's oil boom is here - pipelines are primed to profit. Discover the 22 US stocks riding the wave.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com