Should Polaris's (PII) Sanpan and Monaco Redesign Spur a Rethink of Its Competitive Edge?

- Godfrey Pontoon Boats, a Polaris brand, recently announced a complete redesign of its Sanpan and Monaco pontoon series for the 2026 model year, introducing modernized features and enhanced technology aimed at elevating comfort and versatility for on-water activities.

- This overhaul not only refreshes two cornerstone product lines but also introduces the Click & Cruise modular accessory system, enabling customizable boating experiences and potentially strengthening Polaris's position in the marine market.

- We'll now examine how innovation such as the Click & Cruise system could shift Polaris's investment narrative in the context of recent analyst expectations.

The latest GPUs need a type of rare earth metal called Neodymium and there are only 35 companies in the world exploring or producing it. Find the list for free.

Polaris Investment Narrative Recap

To be a Polaris shareholder, one must believe the company can manage external pressures such as tariffs and shifting consumer trends, while leveraging innovation to grow sales and improve profitability. The recent Godfrey Sanpan and Monaco redesign, including the modular Click & Cruise system, may enhance Polaris’s appeal in the marine segment, but the announcement does not materially change the primary short-term catalyst, which remains the company's efforts to offset gross tariff costs. The biggest risk, potential for margin compression from high tariff expenses, remains in focus.

Among Polaris’s recent announcements, the October update for its RZR and RANGER off-road lineups aligns closely with its emphasis on product innovation. New digital features in these models echo the technological upgrades seen in its marine products, reinforcing the company’s push to drive demand through elevated user experience. This innovation remains a key catalyst supporting the company’s near-term narrative.

However, investors should also be aware that significant uncertainty related to future revenues and earnings persists if tariff costs escalate...

Read the full narrative on Polaris (it's free!)

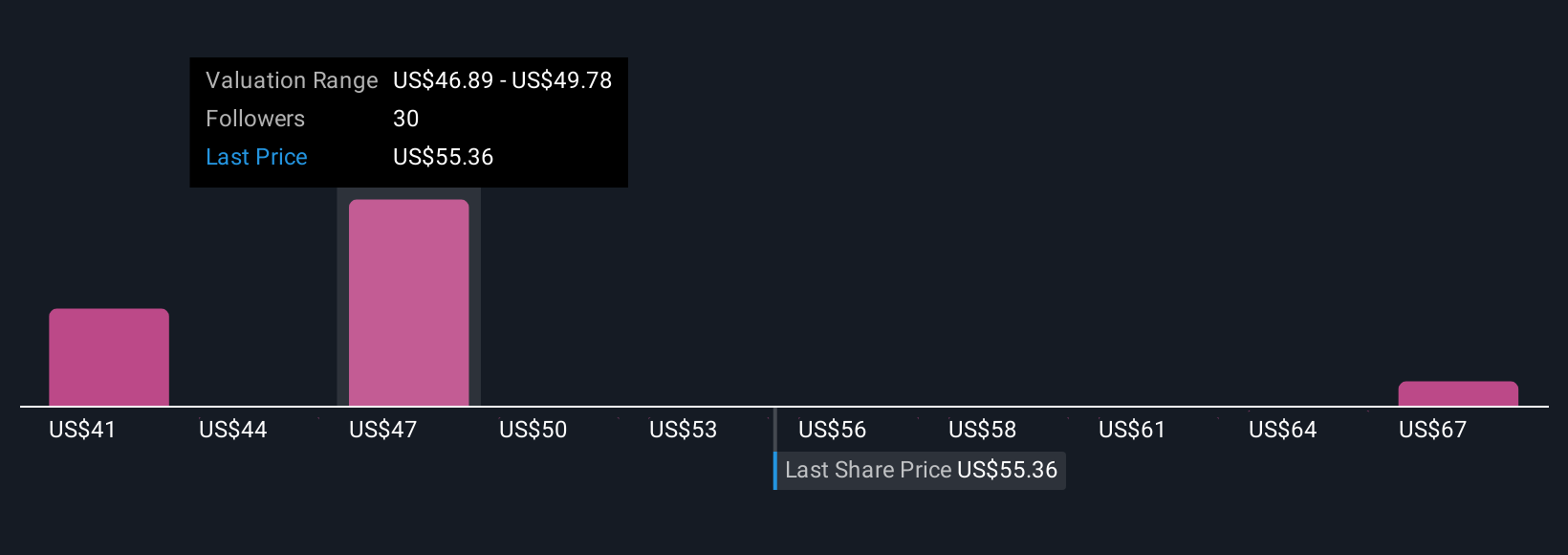

Polaris' narrative projects $7.5 billion in revenue and $224.6 million in earnings by 2028. This requires 2.4% yearly revenue growth and a $332.4 million earnings increase from the current earnings of -$107.8 million.

Uncover how Polaris' forecasts yield a $65.83 fair value, in line with its current price.

Exploring Other Perspectives

Six separate fair value estimates from the Simply Wall St Community range widely between US$7.23 and US$70, showing sharply different outlooks for Polaris. While these opinions reflect a broad spectrum, the primary current risk highlighted by analysts, tariff-related margin pressures, can have major effects on performance and is vital for investors to consider as they compare viewpoints.

Explore 6 other fair value estimates on Polaris - why the stock might be worth less than half the current price!

Build Your Own Polaris Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Polaris research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Polaris research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Polaris' overall financial health at a glance.

Ready For A Different Approach?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- Find companies with promising cash flow potential yet trading below their fair value.

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

- Trump has pledged to "unleash" American oil and gas and these 22 US stocks have developments that are poised to benefit.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com