Kulicke and Soffa (KLIC) Guides Higher for Q1 2026 After Returning to Profit and Completing Buybacks

- Kulicke and Soffa Industries reported its fourth quarter and full-year results, showing quarterly sales of US$177.56 million and a full-year return to profitability, while also providing first-quarter 2026 earnings guidance with anticipated revenue of approximately US$190 million plus or minus US$10 million.

- The company also completed a share repurchase program, buying back 1,786,177 shares for US$66.2 million, which reflects ongoing efforts to manage its capital allocation.

- We'll examine how guidance for improved earnings in early fiscal 2026 could shape Kulicke and Soffa's investment narrative.

Uncover the next big thing with financially sound penny stocks that balance risk and reward.

What Is Kulicke and Soffa Industries' Investment Narrative?

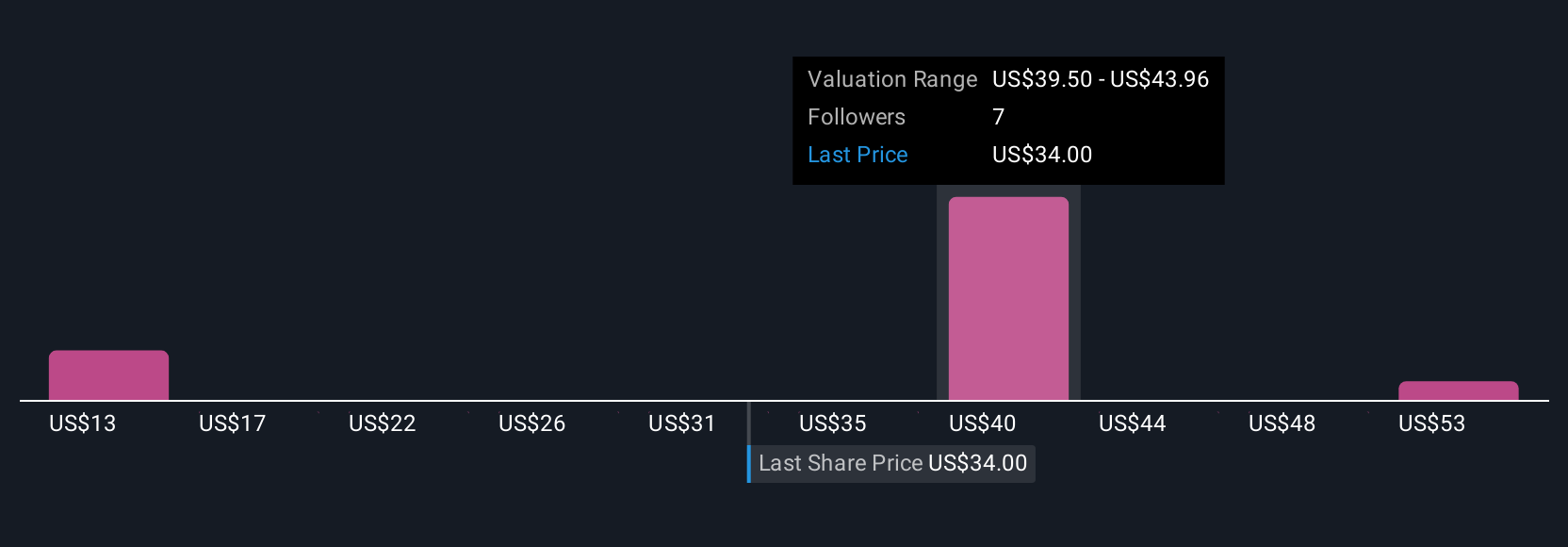

To be a shareholder in Kulicke and Soffa Industries, you need to believe in the company's ability to ride cycles in the semiconductor equipment market, capitalize on new product launches like the ACELON™ platform, and effectively manage capital allocation, as signaled by the completed buyback of over 1.78 million shares. The latest earnings report showed a modest return to profitability, though sales and net income were lower year-over-year. First quarter guidance for fiscal 2026 leans positive, with revenue expected to improve to around US$190 million. The buyback underscores management’s confidence, but the near-term picture remains influenced by broader industry trends and recent executive changes with an interim CEO stepping in. While the share price has recently rebounded, margin pressure and coverage of the dividend by earnings are still near-term risks to track. However, the share buyback itself is unlikely to significantly change the primary catalysts or shift the key risks facing the business right now.

But with recent management changes ahead, boardroom stability is something investors should be paying attention to.

Exploring Other Perspectives

Explore 3 other fair value estimates on Kulicke and Soffa Industries - why the stock might be worth less than half the current price!

Build Your Own Kulicke and Soffa Industries Narrative

Disagree with this assessment? Create your own narrative in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Kulicke and Soffa Industries research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Kulicke and Soffa Industries research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Kulicke and Soffa Industries' overall financial health at a glance.

Ready For A Different Approach?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

- We've found 15 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

- Find companies with promising cash flow potential yet trading below their fair value.

- The end of cancer? These 29 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com