Assessing Certara (CERT) Valuation After Leerink Partners Upgrade To Outperform

Leerink Partners’ upgrade of Certara (CERT) to an Outperform rating, after a period of downward revisions, has put fresh attention on the biosimulation specialist and how investors might think about its risk and reward profile.

See our latest analysis for Certara.

At a share price of $9.49, Certara has recently seen a 7.72% 7 day share price return and a 4.40% 30 day share price return. However, its 1 year total shareholder return of 13.88% and 3 year total shareholder return of 44.41% point to a longer stretch of weaker investor outcomes. The recent upgrade and the sharp single session drop after earnings are landing against a backdrop where short term momentum is picking up while long term returns remain under pressure.

If this kind of sector reset has your attention, it might be a good moment to scan other healthcare stocks that could fit a similar thesis. You may find ideas with different risk profiles but linked to the same broad theme.

With Certara trading at US$9.49, sitting on weaker multi year returns but showing revenue and net income growth, the big question is simple: is this a reset that leaves the shares undervalued, or is the market already pricing in future growth?

Most Popular Narrative Narrative: 24.3% Undervalued

With Certara last closing at US$9.49 and the most followed narrative pointing to a higher fair value, the gap between story and price is clear and worth unpacking.

The upcoming commercial launch of Certara's next-generation, AI-enabled MIDD platform and CertaraIQ QSP software leverages advanced analytics and machine learning, providing differentiated capabilities that democratize access and increase the potential customer base, which should translate to higher recurring revenue and margin expansion through cloud-based SaaS models.

Curious what kind of revenue path and margin profile need to line up for that valuation gap to close? The narrative leans heavily on detailed growth, profitability and earnings multiple assumptions that most investors never see laid out this clearly.

Result: Fair Value of $12.54 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, this story can break if pharma customers stay cautious on R&D budgets, or if heavier spending on AI platforms fails to translate into solid earnings.

Find out about the key risks to this Certara narrative.

Another View: Expensive On Earnings

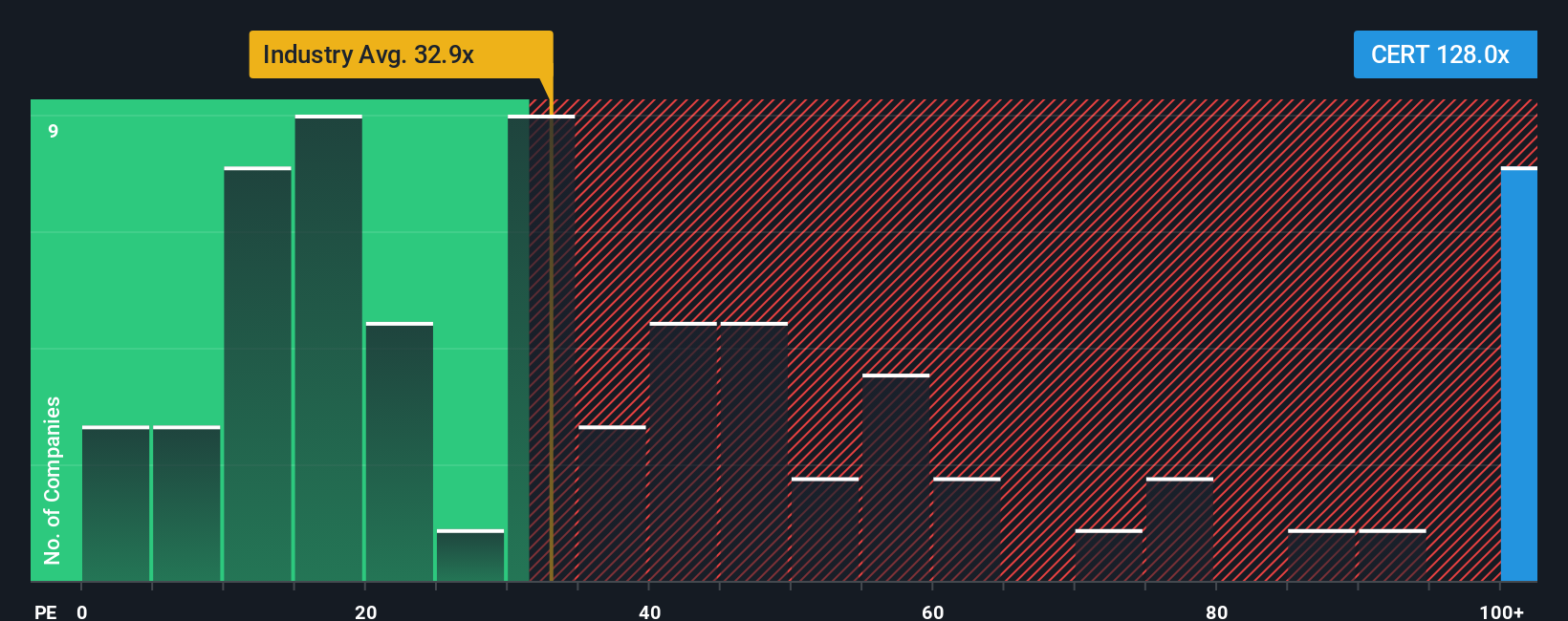

Our DCF model sees Certara as undervalued, but the picture looks very different when you look at the P/E ratio. At 139x earnings compared with 52.8x for peers, 32.8x for the global Healthcare Services group, and a fair ratio of 37.8x, the shares screen as expensive. If the market moves back toward that fair ratio instead, how comfortable are you with the downside this could imply?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Certara Narrative

If you look at these numbers and come to a different conclusion, or simply want to test your own view against the data, you can build a custom narrative in just a few minutes, starting with Do it your way.

A great starting point for your Certara research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If Certara has sharpened your thinking, do not stop here. Broaden your watchlist with focused stock ideas that match how you like to build a portfolio.

- Target higher growth potential by reviewing these 26 AI penny stocks that are leaning into artificial intelligence across different parts of the market.

- Strengthen your income focus by scanning these 12 dividend stocks with yields > 3% that may help you build more consistent cash returns from your holdings.

- Hunt for potential mispricing by studying these 886 undervalued stocks based on cash flows that could offer a different balance of risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com