Assessing Camping World Holdings (CWH) Valuation After Recent Share Price Momentum And Conflicting Fair Value Signals

Recent Performance Snapshot for Camping World Holdings

Camping World Holdings (CWH) has drawn investor attention after a mixed stretch in the stock, with gains over the past month and year to date, alongside weaker returns in the past 3 months and over the past year.

See our latest analysis for Camping World Holdings.

With the share price at US$11.01, a 13.16% 7 day share price return and a 13.39% year to date share price return contrast with a 48.61% 1 year total shareholder return decline, suggesting momentum has picked up recently after a tougher stretch.

If Camping World’s recent swings have you reassessing your watchlist, this could be a good moment to broaden your search with fast growing stocks with high insider ownership.

With Camping World shares at US$11.01 and trading below analyst targets, the key question is whether the recent weakness leaves the stock undervalued or if the current price already reflects any future recovery in the business.

Most Popular Narrative Narrative: 37.4% Undervalued

With Camping World’s fair value estimate at about US$17.58 versus the US$11.01 last close, the popular narrative sees considerable upside embedded in its assumptions.

The growing trend of remote work and flexible living is expanding the pool of potential RV customers, which is likely to drive ongoing increases in unit volumes, new customer acquisitions, and broader adoption of Camping World's products and membership ecosystem. This supports top-line revenue growth and recurring earnings through lifetime customer value.

Curious what underpins that gap between fair value and today’s price? Revenue compounding, margin rebuild, and a future earnings multiple all sit at the core, with the exact mix only clear once you see the full narrative.

Result: Fair Value of $17.58 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, there are still clear risks here, including pressured RV demand and elevated used inventory, which could challenge margins and delay any recovery narrative.

Find out about the key risks to this Camping World Holdings narrative.

Another View: DCF Paints a Very Different Picture

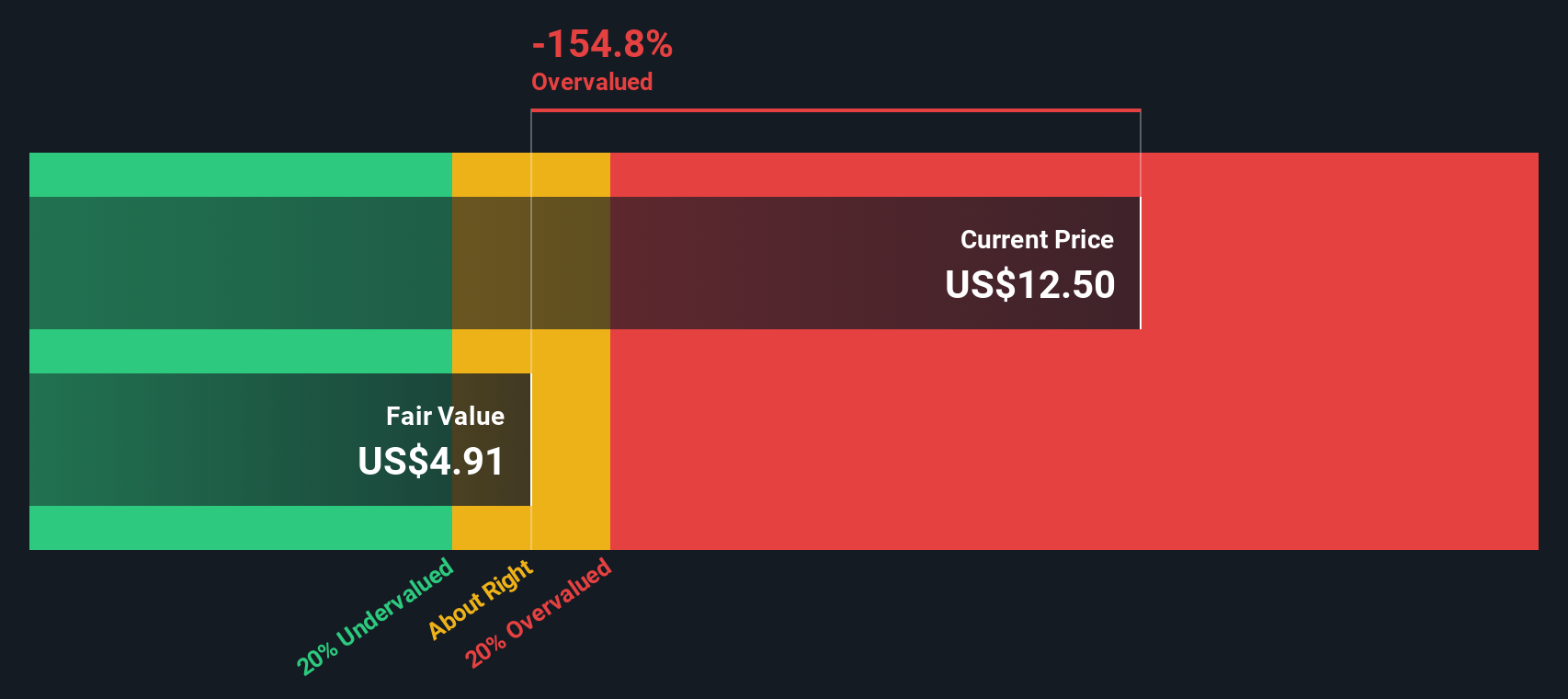

While the popular narrative leans on a fair value of about US$17.58, the SWS DCF model tells a much harsher story. On that measure, Camping World, at US$11.01, sits well above an estimated fair value of roughly US$3.85. This suggests meaningful downside risk if cash flows disappoint.

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Camping World Holdings for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 886 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Camping World Holdings Narrative

If parts of this story do not quite line up with your own view, or you would rather test the numbers yourself, you can build a tailored thesis in just a few minutes with Do it your way.

A great starting point for your Camping World Holdings research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

Ready For More Investment Ideas?

If Camping World has you thinking carefully about risk and reward, do not stop here. Widen your search and pressure test your next move with fresh ideas.

- Target income-focused opportunities by checking out these 12 dividend stocks with yields > 3% that might suit a portfolio built around regular payouts.

- Explore potential growth by scanning these 26 AI penny stocks where companies are tied to artificial intelligence themes and related demand trends.

- Identify possible mispriced names through these 886 undervalued stocks based on cash flows that screen on cash flow based measures, so you can see which ideas justify a deeper look.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com