A Look At OUTFRONT Media (OUT) Valuation After New ANA Partnership Spurs Investor Interest

What the ANA partnership means for OUTFRONT Media

OUTFRONT Media (OUT) has joined the Association of National Advertisers as a 2026 Strategic Partner, becoming the first out of home media company in the program and securing a seat at key brand marketing forums.

For you as an investor, this is less about a single contract and more about access. The company is positioning itself directly in front of senior marketers who control large advertising budgets, while showcasing its in real life media capabilities across ANA events.

See our latest analysis for OUTFRONT Media.

At a share price of $24.61, OUTFRONT Media has a 90 day share price return of 34.04%, while its 1 year and 5 year total shareholder returns of 40.11% and 86.75% point to momentum that has been building over time rather than fading.

If this ANA partnership has you thinking about where advertising and media exposure can lead next, it could be a good moment to look beyond a single stock and check out fast growing stocks with high insider ownership.

With OUTFRONT Media trading at $24.61, close to its $24.20 analyst price target, and showing a 40.11% one-year total return along with a 39.79% intrinsic discount, is there still a buying opportunity here, or is the market already pricing in future growth?

Price-to-Earnings of 35.7x: Is it justified?

At a share price of $24.61, OUTFRONT Media is on a P/E of 35.7x, which sits above both its Specialized REITs industry average and its peer group, even though it screens as good value against an estimated fair P/E of 43.5x.

The P/E multiple tells you how much investors are paying for each dollar of current earnings, which is especially watched for REITs where income and cash generation are key. A higher P/E often reflects expectations that earnings will grow faster than the broader market or that the quality of those earnings is seen as relatively strong.

For OUTFRONT Media, forecasts point to earnings growth of 23.2% per year, which is faster than the expected 16.1% per year for the US market, and its earnings are described as high quality. That kind of outlook helps explain why the market is prepared to pay more than the peer average today, and the fair P/E estimate suggests there is room for the multiple to move closer to that higher level if those expectations hold.

Compared with the US Specialized REITs industry P/E of 29.9x and a peer average P/E of 23.8x, OUTFRONT Media clearly trades at a premium, which signals investors are attaching a stronger earnings profile to this company than to many of its closest comparables.

Explore the SWS fair ratio for OUTFRONT Media

Result: Price-to-Earnings of 35.7x (ABOUT RIGHT)

However, you also need to keep an eye on execution risk around those high expectations and on any shift in advertiser budgets away from out of home formats.

Find out about the key risks to this OUTFRONT Media narrative.

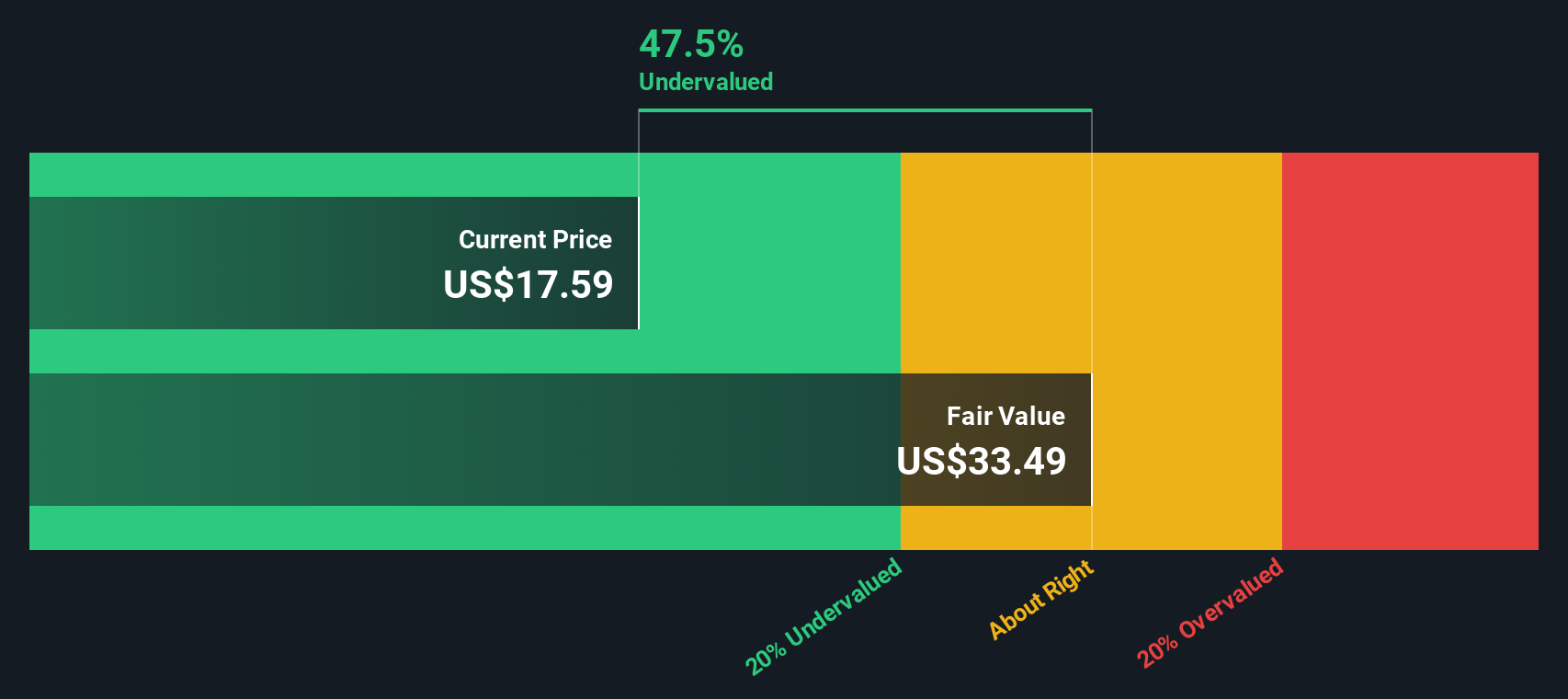

Another View: DCF points to deeper undervaluation

While the 35.7x P/E suggested OUTFRONT Media was roughly in line with expectations, our DCF model comes in very differently, with an estimated fair value of $40.88 versus the current $24.61. That 39.8% discount raises a simple question for you: is this caution or opportunity?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out OUTFRONT Media for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 877 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own OUTFRONT Media Narrative

If this perspective does not fully match your own view, or you would prefer to test the numbers yourself, you can build a custom thesis in just a few minutes by starting with Do it your way.

A great starting point for your OUTFRONT Media research is our analysis highlighting 2 key rewards and 3 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If OUTFRONT Media has sharpened your thinking, do not stop here. Your next strong idea could easily sit in one of these focused stock groups.

- Target income potential by checking out these 13 dividend stocks with yields > 3% that concentrate on companies offering yields above 3%.

- Spot growth stories early with these 23 AI penny stocks that bring together smaller AI focused names in one place.

- Position ahead of structural change through these 19 cryptocurrency and blockchain stocks that track businesses linked to cryptocurrency and blockchain themes.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com