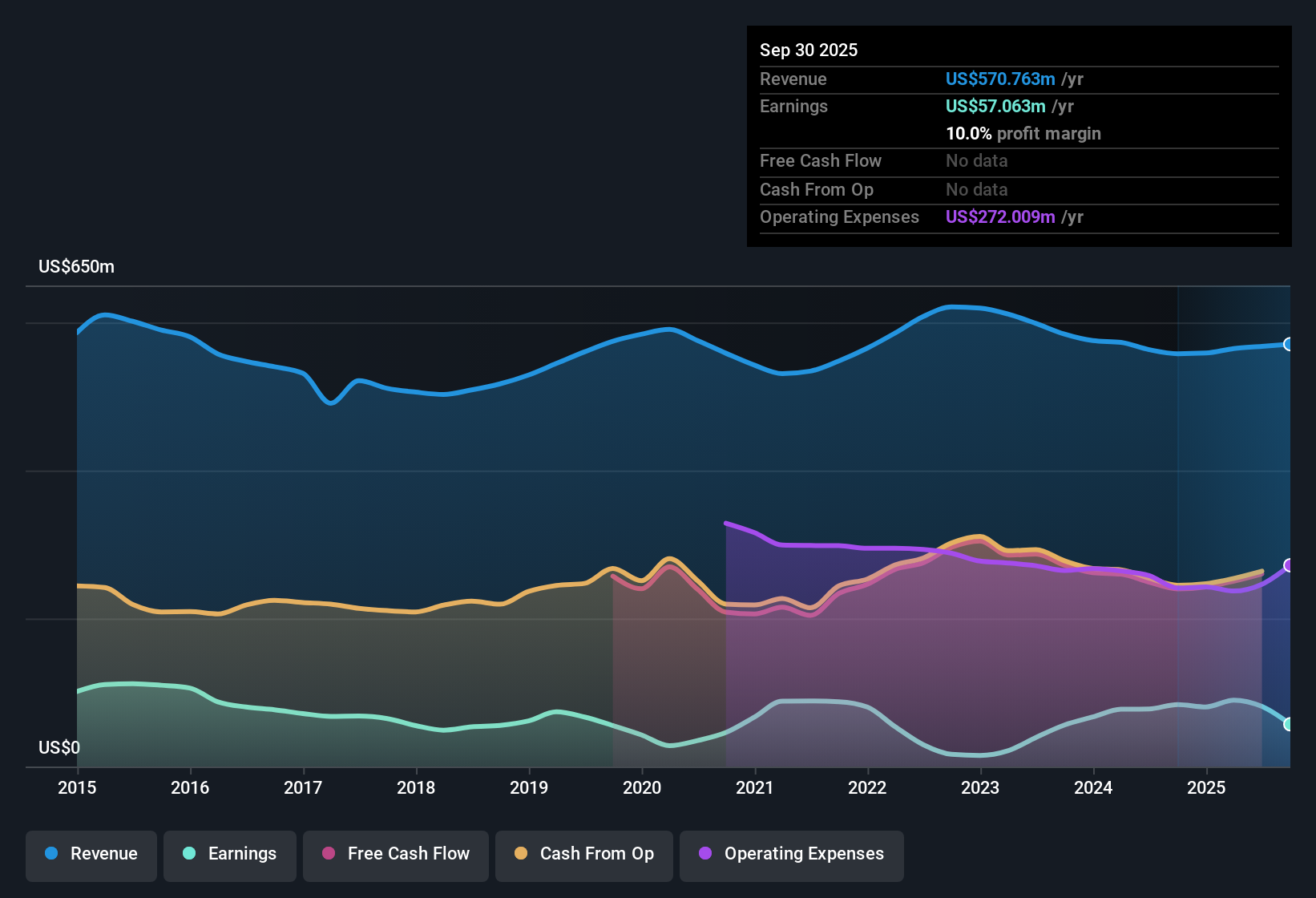

World Acceptance (WRLD) has just reported Q3 2026 results with total revenue of US$141.3 million and a basic EPS loss of US$0.19, while trailing twelve month EPS stands at US$8.47 on revenue of US$573.4 million. The company has seen quarterly revenue move from US$131.4 million in Q2 2025 to US$138.6 million in Q3 2025 and then to US$141.3 million in Q3 2026, with quarterly basic EPS shifting from US$4.05 to US$2.46 and then to a loss of US$0.19 over the same periods. For investors, a key consideration is how this mix of higher revenue, softer EPS and pressure on margins fits with the longer term growth narrative.

See our full analysis for World Acceptance.With the numbers on the table, the next step is to see how this latest earnings profile lines up with the main narratives around World Acceptance, highlighting where the data supports the story and where it pushes back.

Curious how numbers become stories that shape markets? Explore Community Narratives

Margins Under Pressure At 7.5% Net

- Over the last 12 months, World Acceptance reported net income of US$42.8 million on US$573.4 million of revenue, which works out to a 7.5% net profit margin versus 14.4% a year earlier.

- What stands out for the bearish view is that this thinner 7.5% margin coincides with recent quarterly losses, including Q3 2026 net income of US$0.9 million loss, which critics link to pressure on profitability and argue could limit how quickly margins recover if costs stay where they are.

- Bears point to back to back quarterly losses in Q2 2026 and Q3 2026, with net income of US$1.9 million loss then US$0.9 million loss, as reinforcing the concern that the five year earnings growth rate of 0.8% per year masks a weaker recent picture.

- They also highlight that margins a year ago were reported at 14.4%, so the current 7.5% level lines up with the idea that profitability has been under pressure over the last year, even though trailing twelve month net income is still positive.

Forecast ~25% Earnings Growth Versus 2.4% Revenue

- Forecasts in the data call for earnings growth of about 25% per year over the next three years, while revenue is forecast to grow 2.4% per year compared with a higher US market forecast of 10.6% per year.

- What supports a bullish angle is that this 25% earnings growth forecast sits alongside positive trailing twelve month net income of US$42.8 million, yet the recent quarterly EPS loss of US$0.19 in Q3 2026 reminds you that the path to those forecasts is not smooth.

- Supporters focus on the fact that trailing twelve month EPS is US$8.47, which is well above the most recent quarterly loss figure and aligns with the idea that the negative Q3 2026 EPS sits within an otherwise profitable year.

- At the same time, the modest 2.4% revenue growth forecast next to a much higher earnings growth forecast means any bullish case leans heavily on margin improvement or efficiency gains, even though the latest reported net margin is 7.5% versus 14.4% a year earlier.

P/E Of 13.2x And DCF Fair Value At US$138.90

- World Acceptance trades on a trailing P/E of 13.2x, above the US consumer finance industry average of 8.7x but below a peer average of 18.5x, while a DCF fair value of US$138.90 compares with the current share price of US$117.51, about 15.4% lower than that DCF figure.

- For a bullish interpretation, supporters point out that the share price sitting below DCF fair value and below the peer P/E average fits with the idea that the market is weighing recent issues like weak interest coverage and lower margins more heavily than the longer term profile implied by the 25% earnings growth forecast.

- Backers of this view reference that trailing twelve month EPS of US$8.47, when paired with the 13.2x P/E, underpins the current US$117.51 price, while the DCF fair value of US$138.90 uses the same earnings base and points to room between price and model value.

- They also acknowledge that interest payments are reported as not well covered by earnings, which is a material financial risk that helps explain why the P/E is above the industry average but still below the peer average of 18.5x in spite of the stronger earnings growth forecast.

Next Steps

Don't just look at this quarter; the real story is in the long-term trend. We've done an in-depth analysis on World Acceptance's growth and its valuation to see if today's price is a bargain. Add the company to your watchlist or portfolio now so you don't miss the next big move.

See What Else Is Out There

World Acceptance is working through thinner margins, recent quarterly losses and weaker interest coverage, which all put its financial resilience under scrutiny.

If that mix of earnings swings and pressure on profitability makes you cautious, check out solid balance sheet and fundamentals stocks screener (388 results) to focus on companies built with stronger cushions and cleaner balance sheets.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com