Assessing OUTFRONT Media (OUT) Valuation After Strong Recent Share Price Momentum

What OUTFRONT Media’s recent performance tells you

With no single headline event driving attention to OUTFRONT Media (OUT), investors are instead looking at its recent performance and fundamentals, including a last close of $24.58 and reported revenue of $1.81b.

See our latest analysis for OUTFRONT Media.

At a share price of $24.58, OUTFRONT Media’s recent 90-day share price return of 38.95% and 1-year total shareholder return of 41.91% suggest momentum has been building rather than fading.

If OUTFRONT’s move has caught your attention, this can be a good moment to broaden your watchlist with fast growing stocks with high insider ownership.

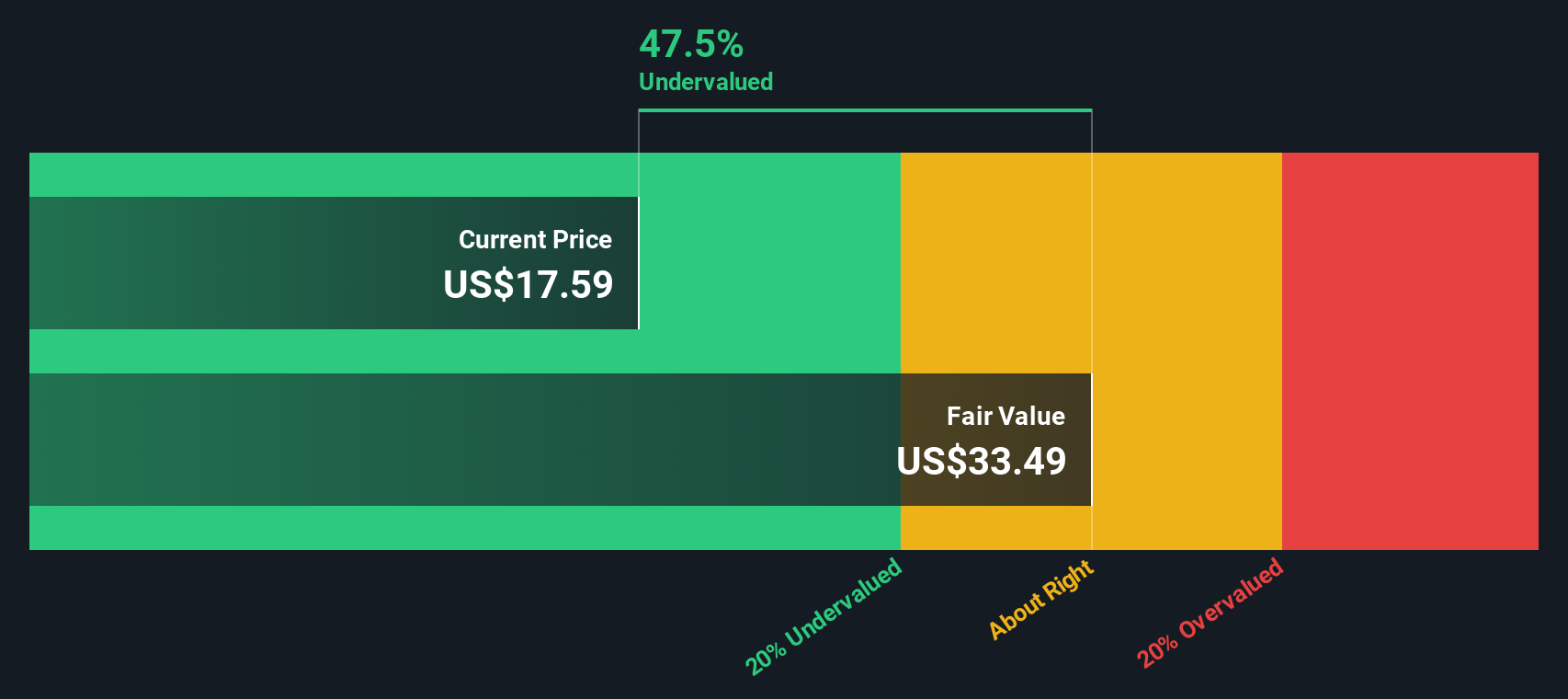

With the stock up strongly over the past year, a reported intrinsic discount of about 40% and a share price close to analysts’ target, is there still a buying opportunity here, or is the market already pricing in future growth?

Most Popular Narrative: 2% Overvalued

OUTFRONT Media’s most followed narrative places fair value at $24.20, slightly below the $24.58 last close. This keeps expectations and reality very close together.

OUTFRONT's ongoing digital conversion of static billboards and transit assets to digital displays enables higher ad rotation, dynamic content, and premium pricing, directly supporting accelerated top-line growth and long-term margin expansion.

Curious what kind of revenue path and margin rebuild has to line up for that fair value, and what future earnings multiple ties it all together? The full narrative spells out the growth, profitability and valuation balance behind that $24.20 figure without leaving those assumptions to guesswork.

Result: Fair Value of $24.20 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, you still need to weigh risks such as weaker demand for traditional out of home assets and the capital intensity of digital conversions potentially squeezing margins.

Find out about the key risks to this OUTFRONT Media narrative.

Another way of looking at value

While the narrative pegs fair value at $24.20 and labels OUTFRONT Media as slightly overvalued, our SWS DCF model points in the other direction, with a future cash flow value of $40.87. This suggests the shares are trading at a sizeable discount. Which set of assumptions do you find more realistic?

Look into how the SWS DCF model arrives at its fair value.

Build Your Own OUTFRONT Media Narrative

If you are not fully on board with these assumptions or prefer to work from your own research, you can build a custom view of OUTFRONT’s story in just a few minutes, starting with Do it your way.

A great starting point for your OUTFRONT Media research is our analysis highlighting 2 key rewards and 3 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Once you have formed a view on OUTFRONT Media, do not stop there. Broaden your opportunity set by stress testing ideas across different themes and sectors.

- Spot potential mispricings by scanning these 868 undervalued stocks based on cash flows that line up with your return and risk expectations.

- Ride emerging technology trends by checking out these 23 AI penny stocks that link artificial intelligence to real revenue streams.

- Tap into income-focused opportunities by reviewing these 14 dividend stocks with yields > 3% that may complement a long term total return approach.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com