How Arcos Dorados’ 2026 Restaurant Expansion Plan At Arcos Dorados Holdings (ARCO) Has Changed Its Investment Story

- Arcos Dorados Holdings Inc., the master franchisee for McDonald’s in Latin America and the Caribbean, has announced plans to open between 105 and 115 new restaurants across its operating footprint in 2026.

- This expansion plan highlights the company’s continued emphasis on unit growth, even as its margins and free cash flow levels have constrained its ability to fund major initiatives internally.

- We’ll now examine how this planned restaurant rollout for 2026 could influence Arcos Dorados’ investment narrative and longer-term growth profile.

Trump's oil boom is here - pipelines are primed to profit. Discover the 22 US stocks riding the wave.

What Is Arcos Dorados Holdings' Investment Narrative?

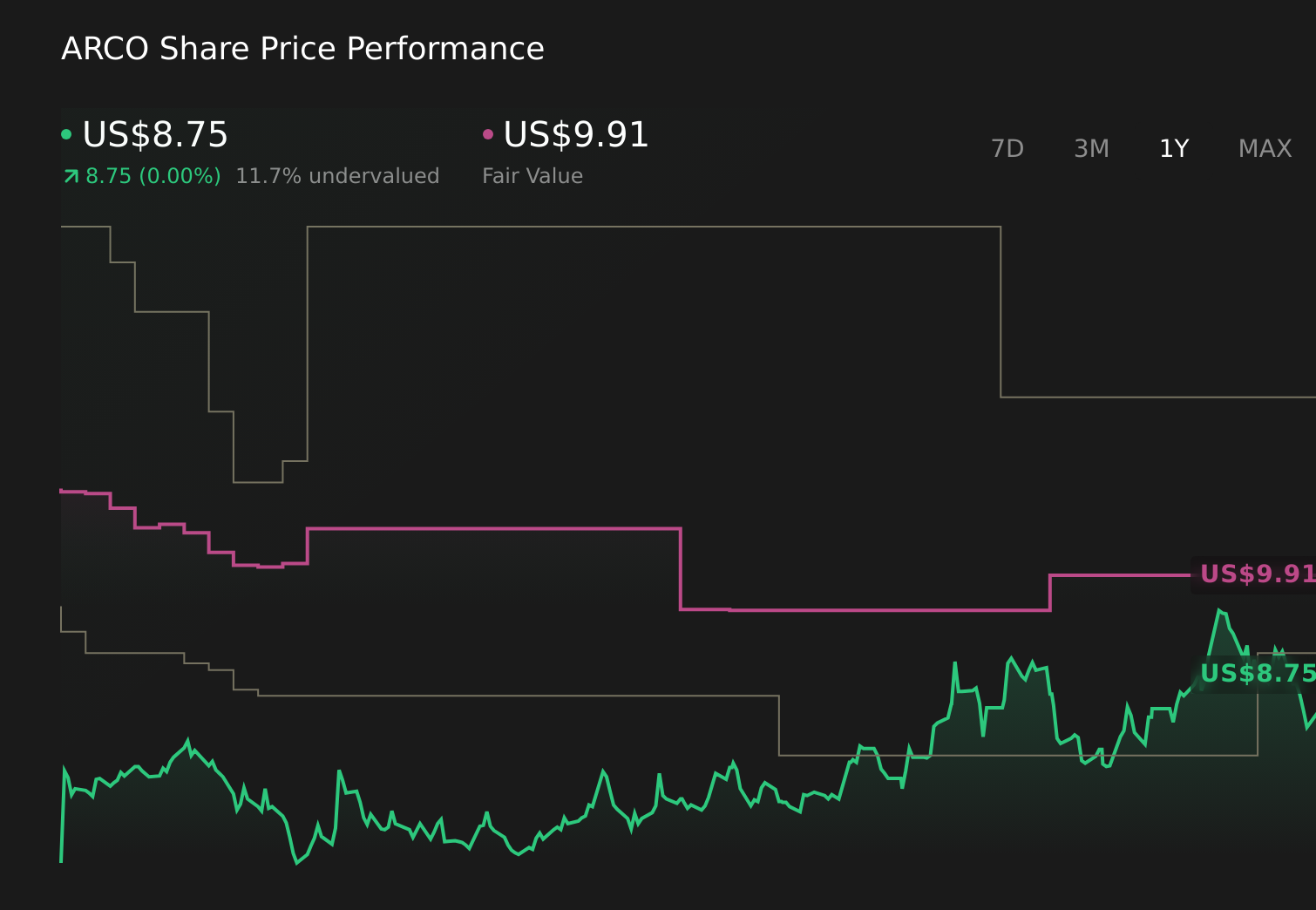

For someone owning Arcos Dorados, the big picture is still about believing that a focused McDonald’s operator across Latin America can translate its scale and long franchise runway into durable cash generation, despite structurally thin restaurant margins and a high debt load. The planned 105 to 115 new restaurants in 2026 leans into that belief: it reinforces the unit growth story but also raises near term questions around capital intensity and returns on invested capital at a time when free cash flow has been weak and earnings are expected to contract over the next few years. Recent share gains and a modest discount to analyst targets suggest the market is not treating this rollout as a game changer yet, but it does sharpen execution, balance sheet and franchise royalty risks.

However, investors should also factor in how higher royalties, leverage and weak free cash flow could interact. Arcos Dorados Holdings' shares are on the way up, but they could be overextended by 25%. Uncover the fair value now.Exploring Other Perspectives

Four fair value estimates from the Simply Wall St Community span roughly US$6.50 to US$12.35 per share, underscoring how differently people are weighing Arcos Dorados’ aggressive 2026 restaurant expansion against its thin margins and high debt, and inviting you to compare these views with your own expectations for execution and balance sheet resilience.

Explore 4 other fair value estimates on Arcos Dorados Holdings - why the stock might be worth as much as 52% more than the current price!

Build Your Own Arcos Dorados Holdings Narrative

Disagree with this assessment? Create your own narrative in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Arcos Dorados Holdings research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Arcos Dorados Holdings research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Arcos Dorados Holdings' overall financial health at a glance.

Seeking Other Investments?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

- The latest GPUs need a type of rare earth metal called Neodymium and there are only 33 companies in the world exploring or producing it. Find the list for free.

- These 12 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com