What TreeHouse Foods stock data suggests today

TreeHouse Foods (THS) shares closed at $24.65, and recent returns show mixed signals, with gains over the past month and past 3 months alongside a 1-year total return decline.

See our latest analysis for TreeHouse Foods.

The recent 90 day share price return of 35.44% contrasts sharply with the 1 year total shareholder return decline of 29.71%. This suggests that short term momentum has picked up even as longer term holders remain under pressure.

If TreeHouse Foods has you rethinking your portfolio, this could be a good moment to widen your search with fast growing stocks with high insider ownership and see what else is catching investors’ attention.

With TreeHouse Foods trading at $24.65, an intrinsic value estimate suggesting a 15% discount and a recent 35.44% 90 day return, is this a genuine value opportunity, or is the market already pricing in future growth?

Most Popular Narrative: 16% Overvalued

Compared with the $24.65 share price, the most followed narrative fair value of about $21.31 points to a valuation that sits above those expectations.

The ongoing expansion of value-focused shopping and persistent demand for private label/store brands is supporting share gains for TreeHouse Foods, with numerous retail partners (e.g., ALDI, Walmart) investing heavily in private label strategy. This structural shift should drive resilient volume and revenue growth, especially as economic uncertainty and inflation continue to reinforce value-oriented consumer behavior.

Curious what kind of revenue mix, margin rebuild, and earnings path underpin that fair value? The narrative leans on gradual volume support and a re-rated profit profile. The full story joins these moving parts into one valuation path.

Result: Fair Value of $21.31 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, there are still clear watchpoints, including weak consumption trends and modest expected organic sales growth around 1%, which could challenge the earnings path behind that fair value.

Find out about the key risks to this TreeHouse Foods narrative.

Another View: Cash Flows Point the Other Way

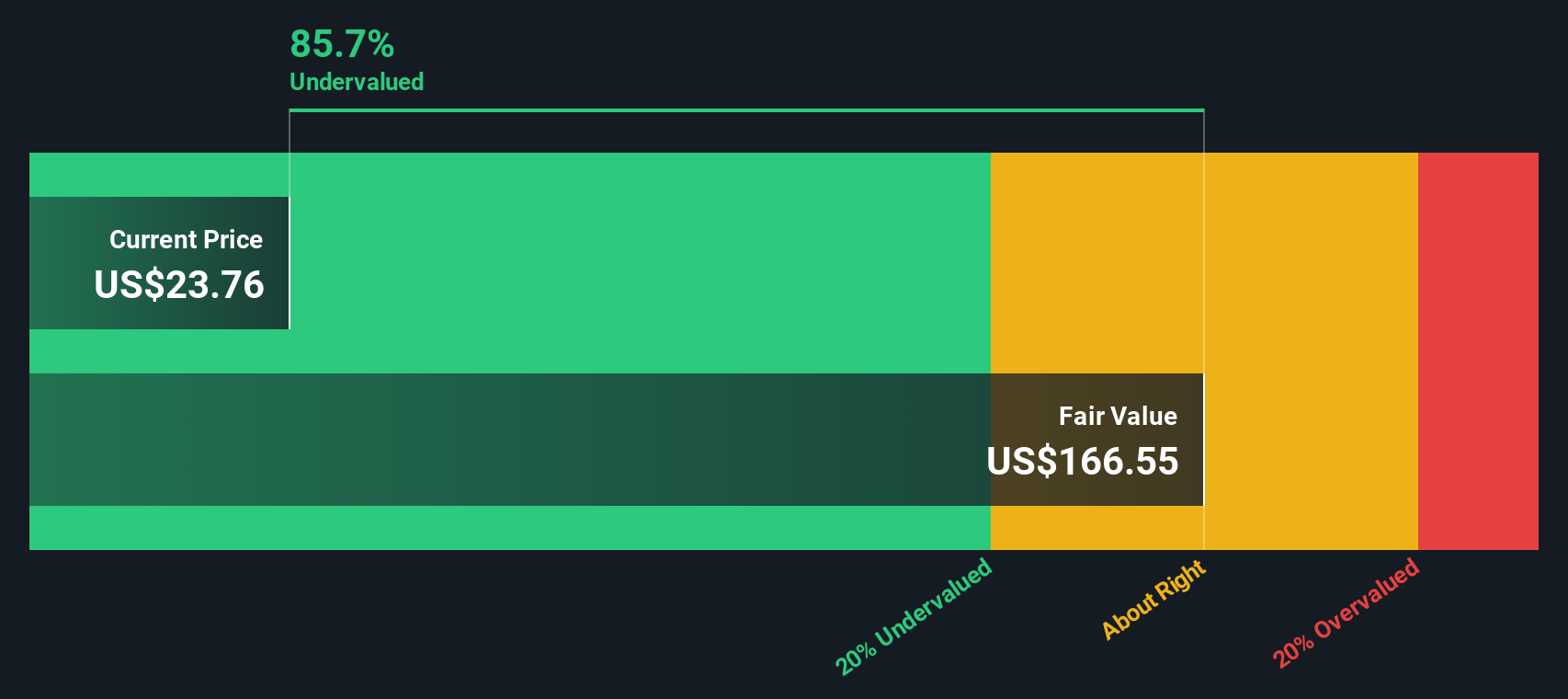

While the most popular narrative suggests TreeHouse Foods is about 16% overvalued at $24.65 versus a fair value of roughly $21.31, our DCF model lands in a very different place. It prices the shares at $160.42 based on future cash flows, implying a very large gap to today’s market price.

For you as an investor, that kind of spread raises a simple question: is the market underestimating TreeHouse’s long term cash generation, or is the DCF leaning too much on assumptions that may not play out?

Look into how the SWS DCF model arrives at its fair value.

Build Your Own TreeHouse Foods Narrative

If this view does not line up with your own, or you prefer to weigh the numbers yourself, you can build a complete narrative in just a few minutes by starting with Do it your way.

A good starting point is our analysis highlighting 3 key rewards investors are optimistic about regarding TreeHouse Foods.

Looking for more investment ideas?

If TreeHouse Foods has sharpened your thinking, do not stop here. Give yourself more options by scanning other themes before you decide where to focus next.

- Jump on early growth stories by checking out these 3524 penny stocks with strong financials that pair smaller share prices with solid financial footing.

- Position your portfolio for the future of automation and data by reviewing these 24 AI penny stocks that are tied to real business models, not just hype.

- Target value driven opportunities by scanning these 866 undervalued stocks based on cash flows that align current prices with underlying cash flows and fundamentals.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com