ConnectOne Bancorp (CNOB) is in focus after releasing fourth quarter and full year 2025 results that included higher net interest income and net income, alongside increased net loan charge-offs and fresh common and preferred dividend declarations.

See our latest analysis for ConnectOne Bancorp.

The recent earnings release, higher net interest income and dividend declarations appear to be feeding into improving momentum, with a 90 day share price return of 13.32% and a 5 year total shareholder return of 37.26% suggesting steady long term value creation.

If ConnectOne’s update has you watching regional banks more closely, it could be a good time to broaden your search with fast growing stocks with high insider ownership.

With the stock at US$27.82, a value score of 2, a roughly 14% gap to the average analyst target and an indicated intrinsic discount of about 57%, is the market overlooking ConnectOne or already pricing in its future growth?

Most Popular Narrative: 12.2% Undervalued

With ConnectOne Bancorp’s fair value estimate at about $31.70 against a last close of $27.82, the most followed narrative sees some upside still on the table.

The pipeline for commercial, SBA, construction, and residential loans is described as "strong," with loan growth opportunities and high current loan yields, highlighting potential for future revenue growth and improved earnings as the expanded footprint leverages secular economic and population growth in the New York and New Jersey regions.

Curious what kind of revenue lift and margin profile that strong pipeline is assumed to support? The narrative leans on aggressive earnings expansion and a future valuation multiple that looks very different to where the stock trades today.

At the core of this fair value is a story about how quickly revenues and earnings could build off the current base, how much of that drops through to profit, and what price investors might be willing to pay for those earnings in a few years. If you want to see the specific growth, margin and P/E assumptions behind the $31.70 anchor, the full narrative lays them out step by step.

Result: Fair Value of $31.70 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, that story can shift quickly if commercial real estate credit losses climb or if integration and regulatory costs after the merger reduce those assumed margins.

Find out about the key risks to this ConnectOne Bancorp narrative.

Another View: Earnings Multiple Sends A Different Signal

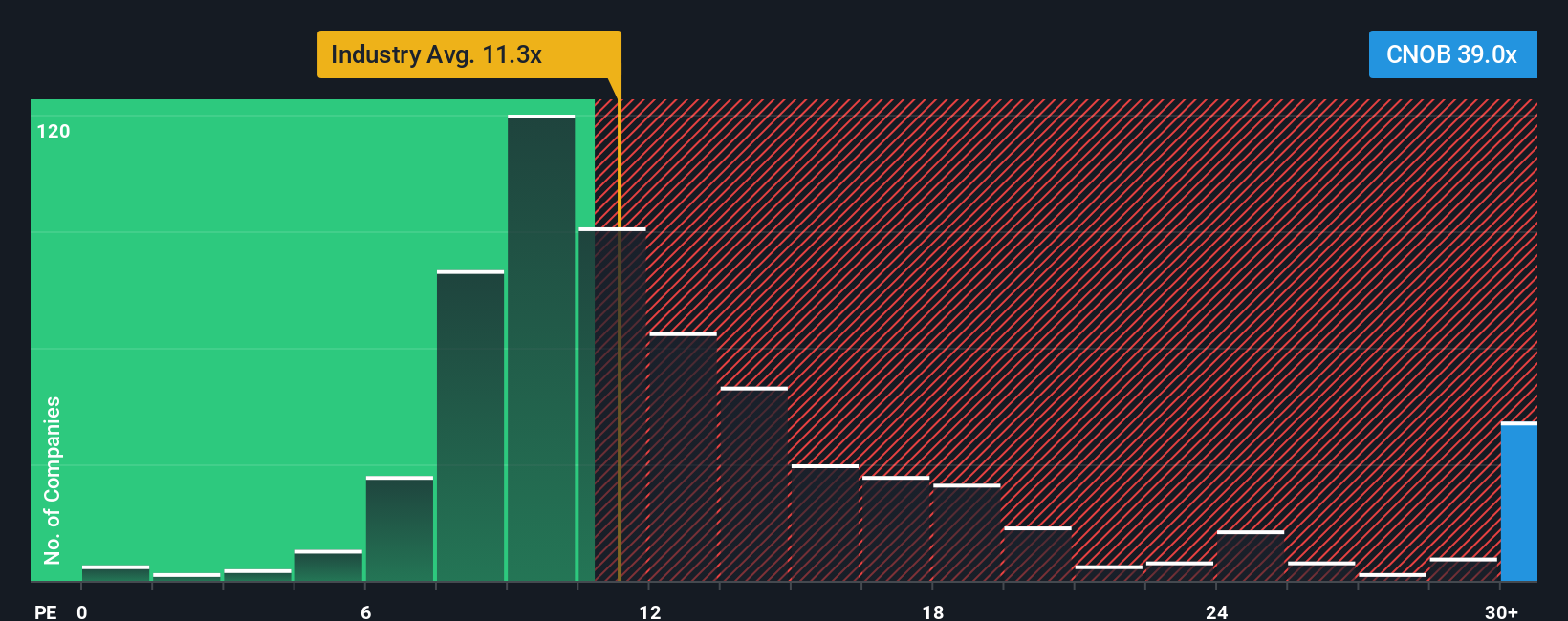

Our model flags ConnectOne as cheap against its own fair value, yet the current P/E of 18.8x is higher than both the US Banks industry at 11.9x and peers at 14.6x, and slightly above a fair ratio of 18.4x. Is the discount story really so straightforward?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own ConnectOne Bancorp Narrative

If you look at the numbers and come to a different conclusion, that is the point. You can test your own view in minutes with Do it your way.

A great starting point for your ConnectOne Bancorp research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If ConnectOne has sharpened your focus, do not stop here. Broaden your watchlist so you are not missing opportunities sitting in plain sight.

- Spot potential growth stories early by checking out these 3533 penny stocks with strong financials targeting smaller companies with stronger balance sheets and cash generation than many expect.

- Position your portfolio for long term tech themes by scanning these 27 AI penny stocks that link artificial intelligence with real business traction and fundamentals.

- Hunt for possible mispricing by reviewing these 868 undervalued stocks based on cash flows that screen for stocks where cash flow based valuations and current prices tell very different stories.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com