Graco (GGG) Valuation Check After Q4 Growth, Margin Gains And Upbeat 2026 Sales Outlook

Graco (GGG) is back in focus after its fourth quarter and full year 2025 earnings, where sales, net income, and earnings per share all came in higher than the prior year’s levels.

See our latest analysis for Graco.

The earnings release and 2026 sales guidance have come alongside a 1-day share price return of 3.14%, adding to a 30-day share price return of 9.66% and a 1-year total shareholder return of 9.69%. Taken together, these figures suggest that momentum has been picking up recently.

If this kind of steady industrial story interests you, it may be a useful moment to broaden your watchlist and check out fast growing stocks with high insider ownership.

With the shares up in recent weeks and trading only slightly below the average analyst price target, the key question now is whether Graco still offers value or if the market is already pricing in its future growth.

Most Popular Narrative: 2% Undervalued

Graco's most followed narrative pegs fair value around $93.44, slightly above the last close at $91.58. This puts a modest valuation gap in focus.

The strategic decision to maintain a strong U.S. manufacturing footprint may give Graco an advantage over competitors who manufacture offshore, especially in light of ongoing trade tensions and tariffs, potentially improving net margins due to cost control and pricing power.

Want to see what is baked into that price tag? The narrative leans on measured revenue growth, firmer margins, and a future earnings multiple that has to stay elevated. Curious which assumptions really carry the fair value math?

Result: Fair Value of $93.44 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, this fair value story depends on tariffs and trade policies not cutting into revenue and margins, and on contractor demand holding up rather than softening.

Find out about the key risks to this Graco narrative.

Another View: Richer On Earnings

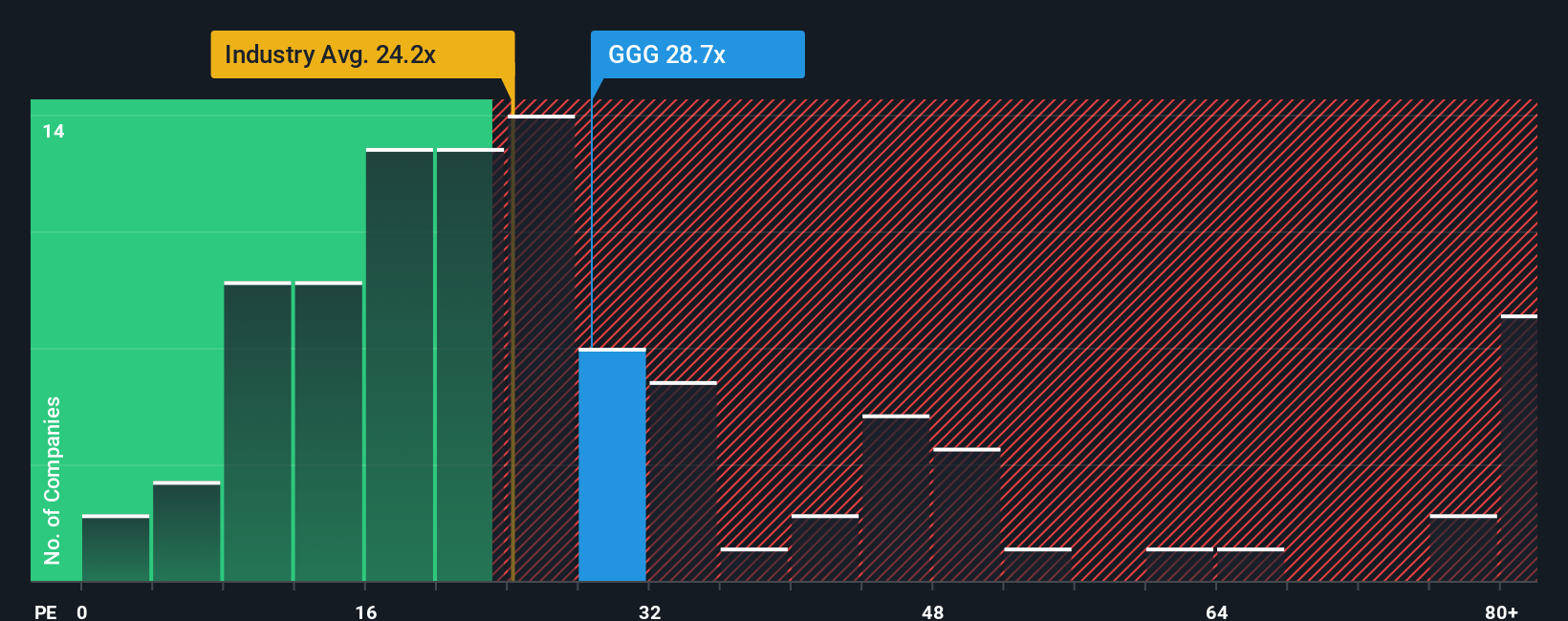

Those fair value narratives lean on future growth and cash flows, but the current P/E of 29x tells a tougher story. It sits above both the US Machinery industry at 28.2x and the estimated fair ratio of 23.3x. This points to valuation risk if expectations slip even a little.

For investors, that spread between 29x and a 23.3x fair ratio is not just a rounding error. It is the cushion that could evaporate first if sentiment cools. The question is whether you are comfortable paying more than peers and the fair ratio for Graco's earnings profile today.

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Graco Narrative

If you look at the numbers and reach a different conclusion, or simply prefer to test your own assumptions, you can build a custom thesis in just a few minutes with Do it your way.

A good starting point is our analysis highlighting 2 key rewards investors are optimistic about regarding Graco.

Looking for more investment ideas?

If Graco has your attention, do not stop there. Use the Simply Wall St Screener to spot other potential opportunities before they move without you.

- Capture potential mispricings by scanning these 865 undervalued stocks based on cash flows that may offer a wider margin between current prices and underlying cash flow estimates.

- Position your portfolio for long term technology shifts by reviewing these 30 AI penny stocks shaping applications of artificial intelligence across multiple industries.

- Strengthen your passive income stream by filtering for these 11 dividend stocks with yields > 3% that combine yield over 3% with consistent dividend profiles.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com