As the U.S. market kicks off February with a strong performance, highlighted by significant gains in major indices like the Dow Jones and S&P 500, investors are paying close attention to broader economic indicators such as manufacturing activity and trade agreements that could impact small-cap companies. In this dynamic environment, identifying stocks with solid fundamentals and growth potential becomes crucial for navigating the ever-evolving landscape of hidden opportunities within the U.S. market.

Top 10 Undiscovered Gems With Strong Fundamentals In The United States

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| First Bancorp | 66.33% | 1.28% | -2.88% | ★★★★★★ |

| Franklin Financial Services | 129.39% | 5.72% | -3.22% | ★★★★★★ |

| Southern Michigan Bancorp | 113.59% | 8.48% | 3.73% | ★★★★★★ |

| Cashmere Valley Bank | 30.46% | 5.25% | 1.74% | ★★★★★★ |

| Oakworth Capital | 26.12% | 15.98% | 13.01% | ★★★★★★ |

| ASA Gold and Precious Metals | NA | 12.65% | 41.20% | ★★★★★★ |

| First Northern Community Bancorp | NA | 7.79% | 11.96% | ★★★★★★ |

| Winchester Bancorp | 121.44% | 49.13% | 3283.33% | ★★★★★★ |

| Seneca Foods | 41.64% | 2.31% | -23.77% | ★★★★★☆ |

| Union Bankshares | 369.65% | 1.12% | -7.45% | ★★★★☆☆ |

Let's dive into some prime choices out of from the screener.

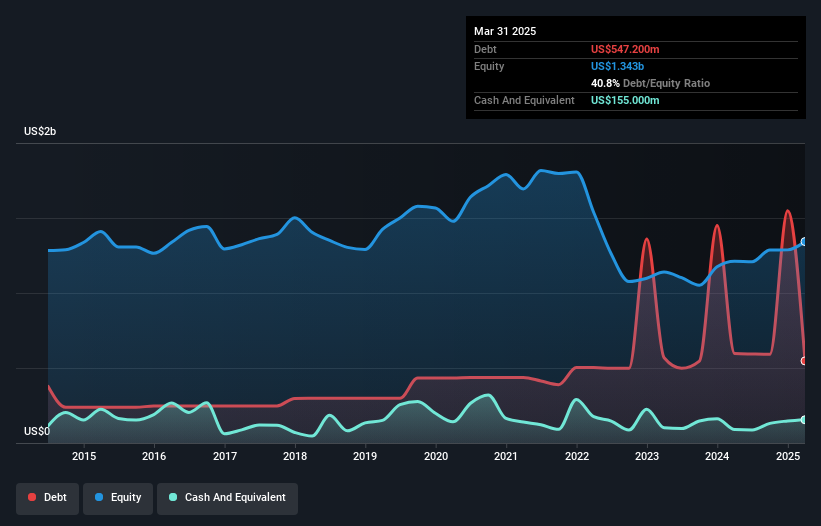

CRA International (CRAI)

Simply Wall St Value Rating: ★★★★☆☆

Overview: CRA International, Inc. offers economic, financial, and management consulting services globally and has a market capitalization of approximately $1.19 billion.

Operations: The primary revenue stream for CRA International comes from its professional and consulting services, generating approximately $731.05 million.

CRA International, a nimble player in the professional services sector, has showcased impressive earnings growth of 31% over the past year, outpacing its industry peers. Trading at 42% below estimated fair value suggests potential upside for investors. The company's net debt to equity ratio stands at a satisfactory 36%, with interest payments well covered by EBIT at 16.8 times. However, CRAI's reliance on antitrust work poses risks amidst competitive pressures that could impact profit margins slightly. Despite these challenges, strategic investments and talent acquisition seem poised to drive future growth in an evolving regulatory landscape.

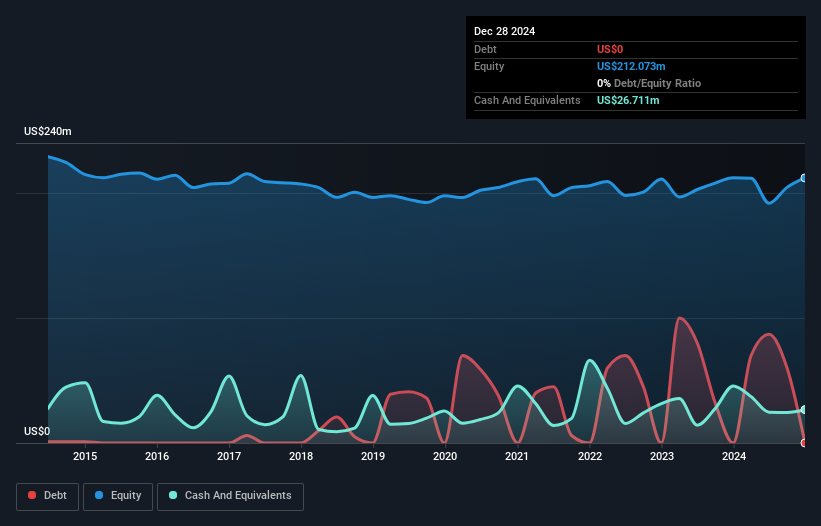

First Bancorp (FNLC)

Simply Wall St Value Rating: ★★★★★★

Overview: The First Bancorp, Inc. is a bank holding company for First National Bank, offering various banking products and services to individual and corporate clients, with a market cap of $326.80 million.

Operations: First Bancorp generates revenue primarily through its banking operations, totaling $92.87 million.

With total assets of US$3.2 billion and equity of US$283.1 million, First Bancorp stands out with its robust financial foundation. It has a loan portfolio of US$2.4 billion backed by deposits totaling US$2.7 billion, indicating strong customer trust and low-risk funding primarily from deposits. The bank's allowance for bad loans is well-managed at 0.4%, reflecting prudent risk management practices. Recent executive changes bring fresh leadership with Brad Martin as the new Executive Vice President, enhancing their tech capabilities amidst industry challenges. Trading below estimated fair value by 41%, it presents a compelling investment opportunity in the banking sector.

- Click here and access our complete health analysis report to understand the dynamics of First Bancorp.

Examine First Bancorp's past performance report to understand how it has performed in the past.

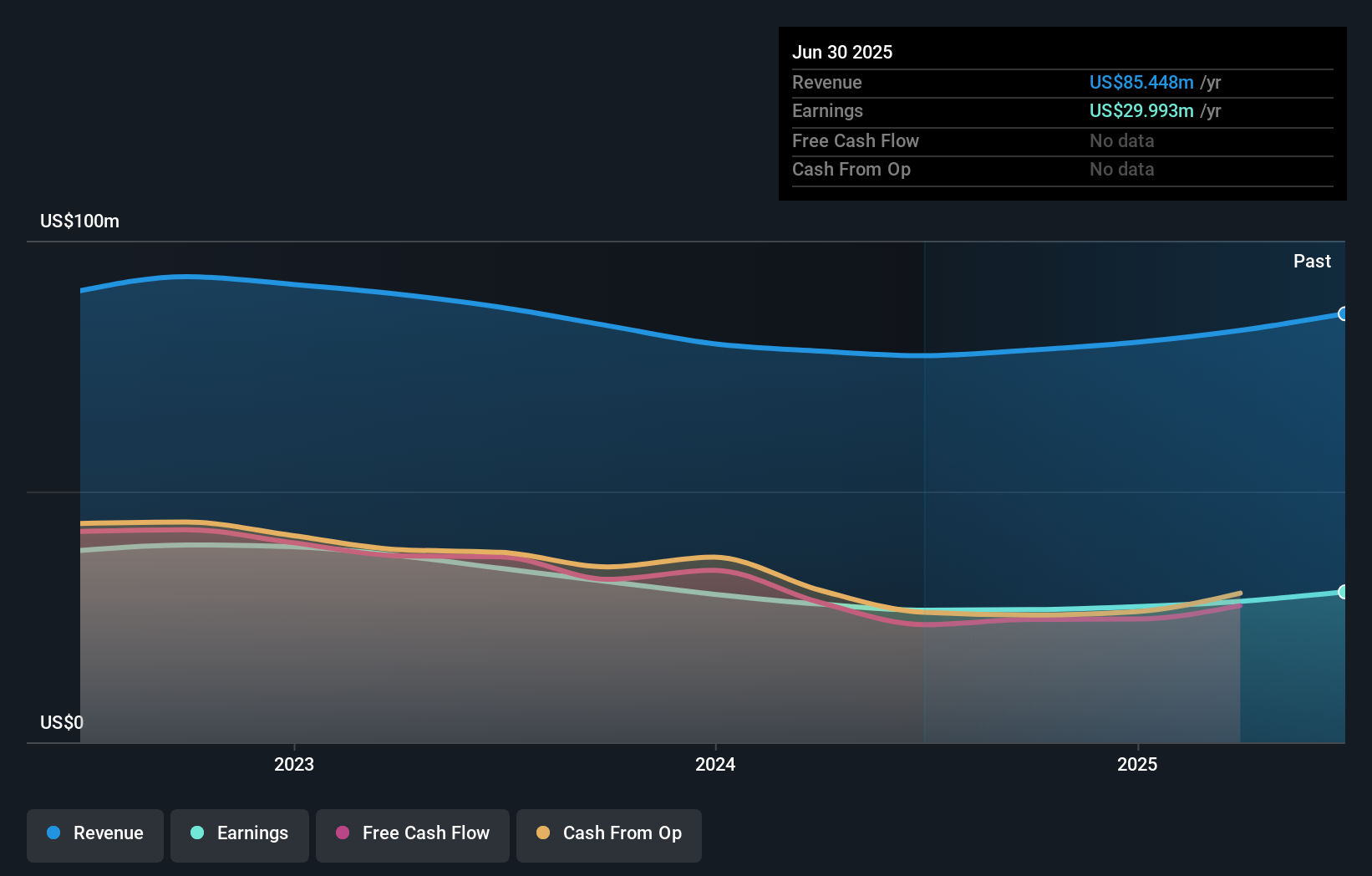

Horace Mann Educators (HMN)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Horace Mann Educators Corporation operates as an insurance holding company in the United States, with a market cap of $1.76 billion.

Operations: Horace Mann Educators generates revenue primarily through its insurance operations. The company's financial performance is influenced by various factors, including claims and underwriting expenses. Its net profit margin reflects the balance between revenue generation and cost management.

Horace Mann Educators, a niche player in the insurance sector, has shown notable financial resilience. With a net debt to equity ratio of 8.1%, it operates with satisfactory leverage, and its earnings grew by 57.7% over the past year, outpacing industry growth of 15.9%. The company's interest payments are well covered by EBIT at 6.5 times coverage, indicating strong financial health. Recent earnings results revealed a revenue increase to US$1.70 billion from US$1.60 billion last year and net income rose to US$162 million from US$103 million, reflecting robust profitability improvements for this small-cap entity focused on educators' needs.

Next Steps

- Discover the full array of 313 US Undiscovered Gems With Strong Fundamentals right here.

- Got skin in the game with these stocks? Elevate how you manage them by using Simply Wall St's portfolio, where intuitive tools await to help optimize your investment outcomes.

- Unlock the power of informed investing with Simply Wall St, your free guide to navigating stock markets worldwide.

Interested In Other Possibilities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com