A Look At OUTFRONT Media (OUT) Valuation After Expanded Formula E And Major Sports Collaborations

OUTFRONT Media (OUT) is back on investors’ radar after being named the Official OOH Advertising Partner of the 2026 ABB FIA Formula E Miami E-Prix and Associate Partner of Change. Accelerated.

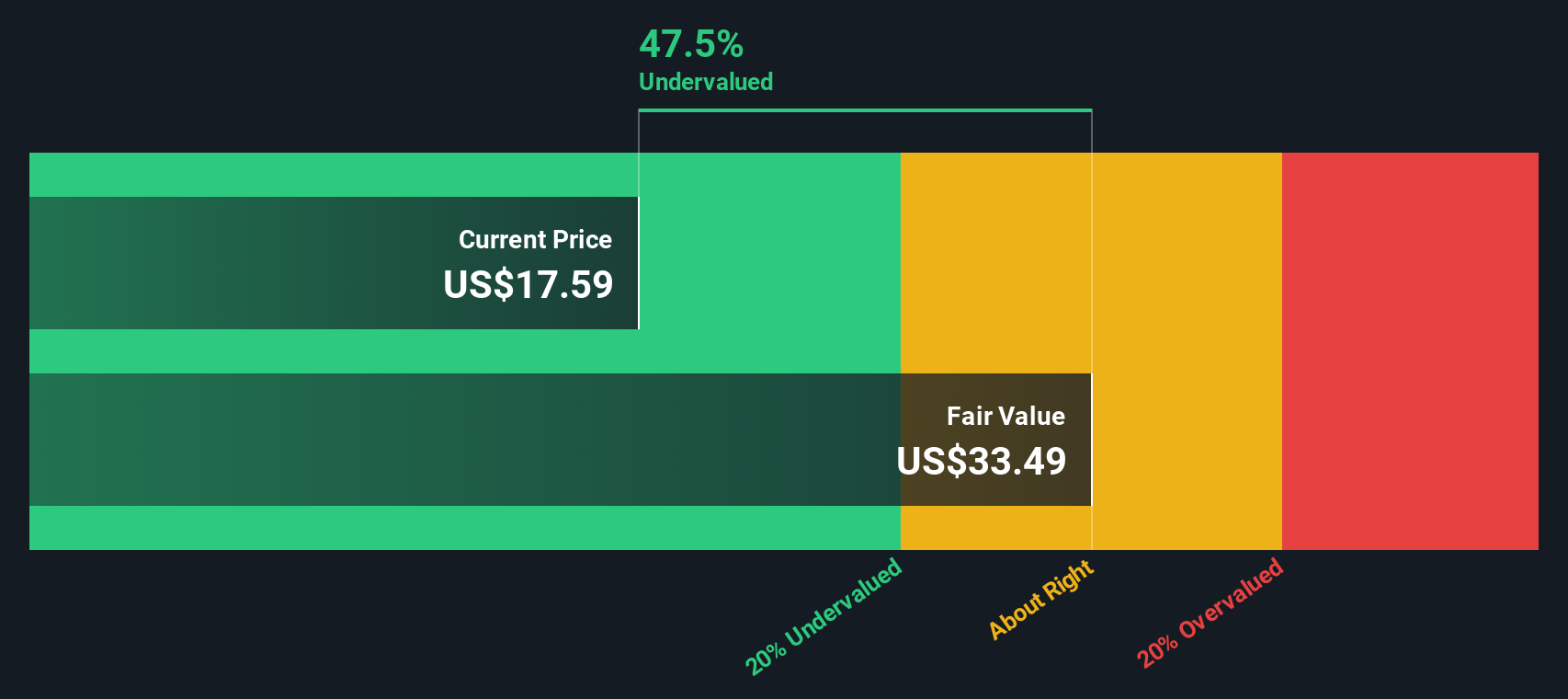

See our latest analysis for OUTFRONT Media.

The Formula E partnership comes as OUTFRONT Media’s share price sits at $26.89, with a 90-day share price return of 33.32% and a 1-year total shareholder return of 53.01%. This indicates that momentum has been building over both shorter and longer periods.

If this kind of event driven story has your attention, it could be a good moment to widen your watchlist with 22 top founder-led companies as potential long term compounders to research next.

With the shares at $26.89, trading above the latest analyst price target yet showing an estimated 37% intrinsic discount, the key question is whether OUTFRONT Media is still undervalued or whether the market is already pricing in future growth.

Most Popular Narrative: 11.1% Overvalued

At $26.89, the most widely followed narrative pegs OUTFRONT Media's fair value at $24.20, putting sentiment slightly ahead of that modeled estimate using a 9.11% discount rate.

OUTFRONT's ongoing digital conversion of static billboards and transit assets to digital displays enables higher ad rotation, dynamic content, and premium pricing, directly supporting accelerated top-line growth and long-term margin expansion. The company's enhanced focus on data analytics, programmatic buying, and improved audience measurement (via investment in ad tech and centralized operations) positions it to capture more digital ad budgets, driving higher occupancy rates and increased revenue per asset.

Curious what kind of revenue path, margin uplift, and future earnings multiple are baked into that fair value? The narrative leans on a very specific growth glide path, a tighter cost base, and a premium yet moderated P/E assumption that differs from current market pricing. If you want to see exactly how those moving parts fit together, the full story lays out the numbers step by step.

Result: Fair Value of $24.20 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, there are still clear pressure points, including ongoing shifts in ad budgets toward digital and social media, as well as the capital intensive nature of OUTFRONT Media's asset base.

Find out about the key risks to this OUTFRONT Media narrative.

Another Take: Cash Flows Point in the Other Direction

While the consensus narrative frames OUTFRONT Media as about 11.1% overvalued at $26.89 versus a $24.20 fair value, our DCF model paints a very different picture, with a future cash flow value of $42.74, or a 37.1% discount. When two methods disagree this much, which one do you lean on?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out OUTFRONT Media for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 52 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own OUTFRONT Media Narrative

If your view of OUTFRONT Media’s future looks different, or you simply prefer to rely on your own homework, you can sketch out a custom thesis in just a few minutes and Do it your way.

A great starting point for your OUTFRONT Media research is our analysis highlighting 2 key rewards and 3 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If OUTFRONT Media has sparked your interest, do not stop there. Broaden your opportunity set with a few focused stock ideas that could reshape your watchlist.

- Zero in on potential value candidates by scanning our list of 52 high quality undervalued stocks that pair appealing prices with underlying business strength.

- Strengthen your income game by reviewing 14 dividend fortresses that combine 5%+ yields with a focus on resilience.

- Keep your downside in check by filtering for 82 resilient stocks with low risk scores that our models flag with lower overall risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com