- In January 2026, Ameris Bancorp reported its fourth-quarter and full-year 2025 results, highlighting higher net interest income of US$245.31 million for the quarter and US$936.92 million for the year, alongside net income of US$108.36 million for the quarter and US$412.15 million for the year.

- Alongside this earnings growth, the bank disclosed higher quarterly net charge-offs of US$13.75 million and the completion of a long-running US$140.63 million share repurchase program retiring 2,707,987 shares.

- We’ll now examine how Ameris Bancorp’s earnings expansion, despite higher net charge-offs, shapes the company’s broader investment narrative for investors.

We've uncovered the 14 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

What Is Ameris Bancorp's Investment Narrative?

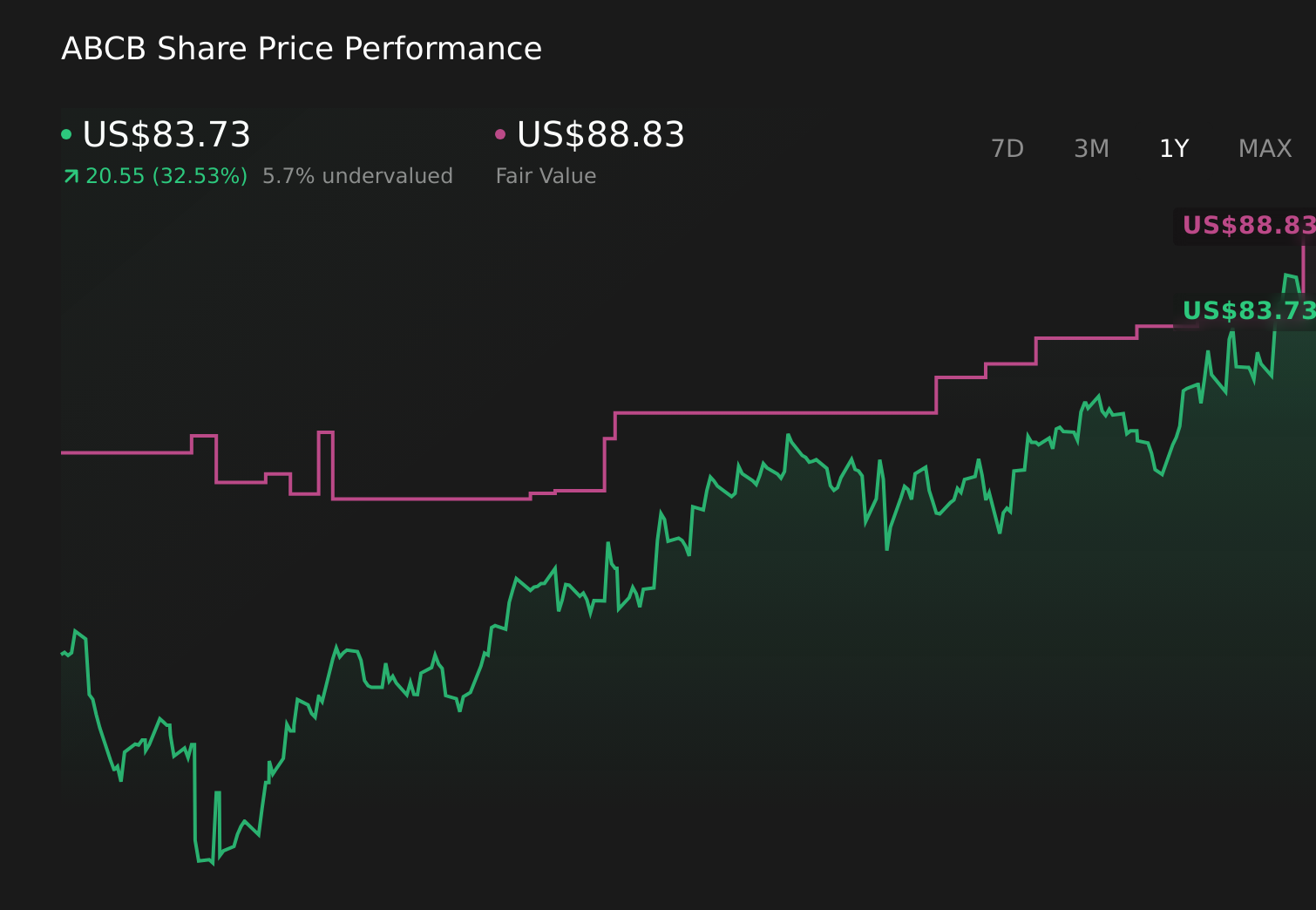

To own Ameris Bancorp today, you have to be comfortable backing a regional bank that is leaning into earnings growth, even as credit costs tick higher and the share price already reflects strong recent returns. The latest results reinforce that story: higher net interest income and net income in 2025, plus EPS at US$6.00, show the core franchise still producing, while the completed US$140.63 million buyback underscores management’s willingness to return capital at a time when the stock trades only modestly below consensus targets. The trade-off is that rising net charge-offs, at US$13.75 million in the fourth quarter, keep asset quality and future credit losses at the center of the short term risk picture. For now, this earnings beat slightly strengthens the positive catalysts without removing those credit concerns.

However, rising charge-offs could be a more persistent issue than the headline numbers suggest. Ameris Bancorp's shares have been on the rise but are still potentially undervalued by 35%. Find out what it's worth.Exploring Other Perspectives

Explore another fair value estimate on Ameris Bancorp - why the stock might be worth as much as $83.29!

Build Your Own Ameris Bancorp Narrative

Disagree with this assessment? Create your own narrative in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Ameris Bancorp research is our analysis highlighting 3 key rewards that could impact your investment decision.

- Our free Ameris Bancorp research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Ameris Bancorp's overall financial health at a glance.

No Opportunity In Ameris Bancorp?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- The future of work is here. Discover the 29 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- Explore 23 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- Uncover the next big thing with 25 elite penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com