Manitowoc Company's FY 2025 Earnings Snapshot

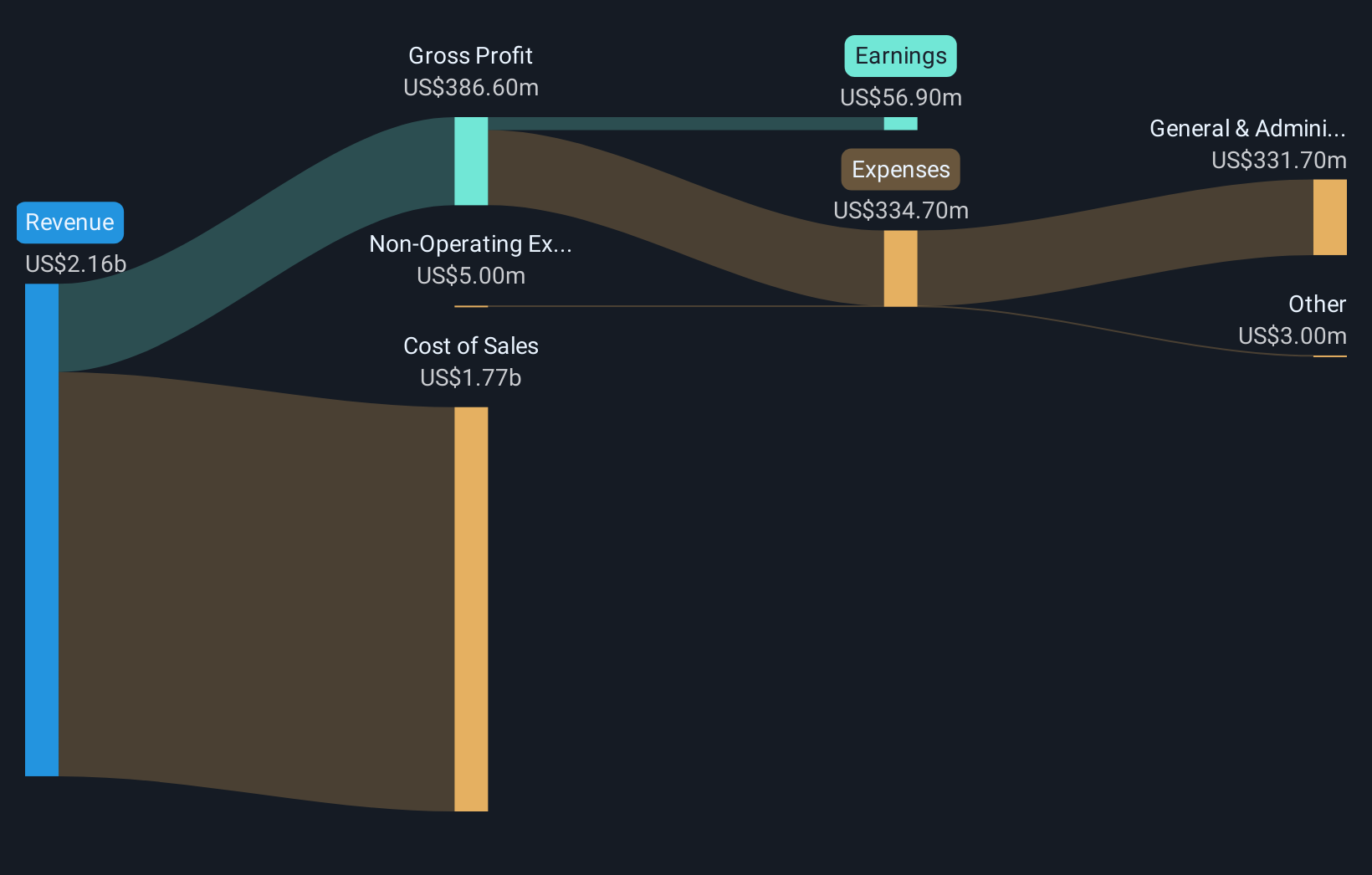

Manitowoc Company (MTW) closed out FY 2025 with Q4 revenue of US$677.1 million and basic EPS of US$0.20, alongside net income of US$7 million, against a backdrop of thin trailing profitability and a current share price of US$15.15. The company has seen quarterly revenue range from US$470.9 million in Q1 2025 to US$677.1 million in Q4 2025. EPS moved from a loss of US$0.18 in Q1 2025 to a profit of US$0.20 in Q4 2025, and trailing twelve month EPS stood at US$0.20 on revenue of US$2.2 billion. With net margin recently at 0.3% on trailing data and a large one off loss affecting the last year, investors are likely to read these results through the lens of fragile margins and the potential for earnings improvement.

See our full analysis for Manitowoc Company.With the FY 2025 scorecard on the table, the next step is to see how these numbers line up against the most common stories investors tell about Manitowoc, and where the latest results might push those narratives to shift.

See what the community is saying about Manitowoc Company

Margins Stay Thin With 0.3% Net Profit

- On a trailing basis, Manitowoc generated US$2.2b of revenue and US$7.2 million of net income, which works out to a 0.3% net margin, compared with 2.6% the prior year and affected by a US$5.5 million one off loss.

- Consensus narrative points to aftermarket services and more flexible manufacturing as potential margin supports. However, the current 0.3% margin and weak interest coverage show that, for now, earnings are still tight relative to the story of more resilient profitability.

- Analysts expect earnings to reach about US$40 million by 2028, while the latest trailing 12 months show only US$7.2 million of net income, so the margin improvement that consensus talks about is not visible in the recent reported numbers.

- With interest payments not well covered by earnings on trailing data, the idea that operational changes alone will smooth earnings has to be weighed against the fact that very thin margins leave limited room for shocks.

Revenue Grows, EPS Swings From Loss To Profit

- Quarterly revenue moved from US$470.9 million in Q1 2025 to US$677.1 million in Q4 2025, while EPS went from a loss of US$0.18 in Q1 2025 to a profit of US$0.20 in Q4 2025, highlighting how sensitive per share results have been to shifts in profitability over the year.

- Bullish views lean on global infrastructure and specialized crane demand to support steadier growth. The move from an EPS loss in early 2025 to a small profit in Q4 fits that story on the surface, but the size of the swing also shows how dependent the company still is on volume and mix.

- For example, Q2 and Q3 2025 both showed profits, but at modest levels, with EPS at US$0.04 and US$0.14 respectively, so the path from loss to profit has not been a straight climb and suggests that end market demand and project timing can quickly change the bottom line.

- Bulls highlight demand from areas like renewables and data centers, yet the recent 12 month net income of US$7.2 million on US$2.2b of revenue indicates that even with these supports, the earnings contribution so far has not matched the stronger margin expectations in those arguments.

P/E At 74.6x With Weak Interest Cover

- On trailing numbers, the stock trades on a P/E of 74.6x, compared with 29.4x for the US Machinery industry and 38.9x for peers, while earnings do not comfortably cover interest expense, so recent profitability does not leave much cushion against borrowing costs.

- Bears argue that tariffs, softer demand in key regions, and higher leverage make this combination of a high P/E and weak interest coverage particularly exposed, and the current figures give that concern concrete backing.

- Net margin dropping to 0.3% from 2.6% and the one off US$5.5 million loss in the last 12 months both show how quickly reported profitability can compress, which matters when interest payments are already not well covered.

- With the share price at US$15.15 and a bearish analyst price target of US$10.00, skeptics are effectively saying that the recent earnings profile and balance sheet risk do not sit comfortably with a P/E that is well above both the industry and peer group.

Next Steps

To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for Manitowoc Company on Simply Wall St. Add the company to your watchlist or portfolio so you'll be alerted when the story evolves.

See the numbers differently? If this data points you in another direction, shape that view into your own narrative in just a few minutes: Do it your way.

A great starting point for your Manitowoc Company research is our analysis highlighting 1 key reward and 3 important warning signs that could impact your investment decision.

See What Else Is Out There

Manitowoc's thin 0.3% net margin, high 74.6x P/E and weak interest coverage indicate that its earnings and balance sheet are not providing much support.

If those tight margins and limited interest coverage concern you, take a few minutes to scan companies in our solid balance sheet and fundamentals stocks screener (45 results) that aim to pair financial strength with earnings support.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com