Southside Bancshares (SBSI) shares are trading around $33.30 after the bank reported full year 2025 results, which showed higher net interest income but lower net income and earnings per share compared with 2024.

See our latest analysis for Southside Bancshares.

The stock’s recent performance reflects mixed sentiment, with a 15.54% 90 day share price return and 9.36% year to date share price return. The 3 year total shareholder return is slightly negative and the 5 year total shareholder return is positive, suggesting momentum has picked up more in the short term than over longer horizons as investors weigh the latest earnings, ongoing buybacks and the affirmed dividend.

If this bank update has you thinking about where else capital could work, consider widening your search with our 23 top founder-led companies as a starting list of ideas.

With earnings per share lower than last year, a regular dividend in place, and buybacks reducing the share count, the key question is simple: is Southside Bancshares quietly undervalued here, or is the market already pricing in future growth?

Most Popular Narrative: 4.1% Overvalued

Simply Wall St's most followed narrative puts Southside Bancshares' fair value at about $32 per share, slightly below the recent $33.30 close. This frames the current debate around upside versus patience.

The analysts have a consensus price target of $34.0 for Southside Bancshares based on their expectations of its future earnings growth, profit margins and other risk factors.

In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $337.1 million, earnings will come to $96.2 million, and it would be trading on a PE ratio of 12.7x, assuming you use a discount rate of 7.4%.

Want to see what is sitting behind that $32 fair value and the gap to $63 on the DCF side? The whole narrative leans on a specific earnings path, a firm view on margins and a future earnings multiple that is higher than today. Are you curious which of those levers really does the heavy lifting in this story?

Result: Fair Value of $32 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, this story can change quickly if commercial real estate pressures or rising unrealized losses in the AFS securities portfolio begin to have a greater impact than expected.

Find out about the key risks to this Southside Bancshares narrative.

Another Take: Big Gap In The DCF Math

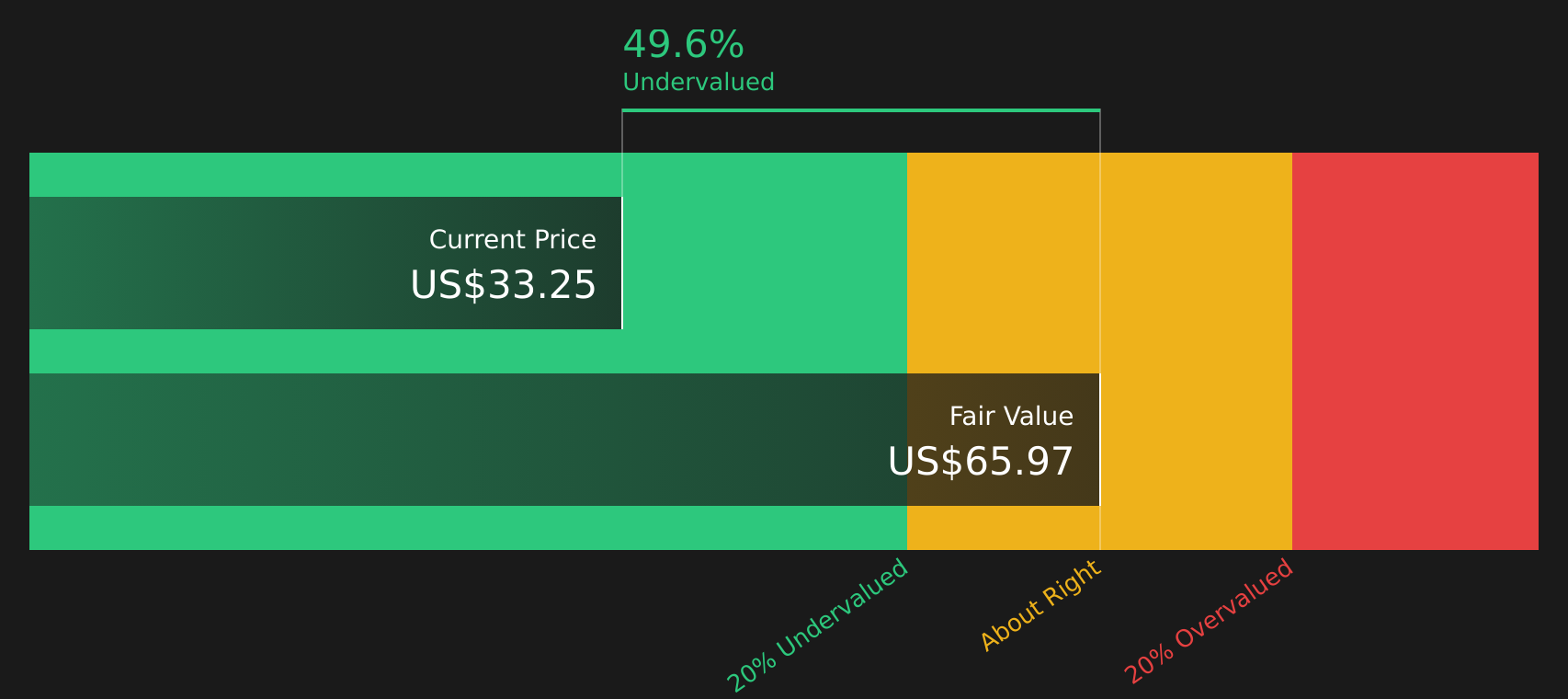

While the most followed narrative lands on a fair value of $32 per share and calls Southside Bancshares overvalued at $33.30, our DCF model points in the other direction and suggests a fair value of about $63.22 and a 47.3% discount. Which story do you find more reasonable?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Southside Bancshares for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 51 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Southside Bancshares Narrative

If you are not fully on board with these assumptions, or you would rather test your own, you can spin up a custom thesis in just a few minutes, starting with Do it your way.

A good starting point is our analysis highlighting 3 key rewards investors are optimistic about regarding Southside Bancshares.

Looking for more investment ideas?

If you are weighing what to do next with Southside Bancshares, it makes sense to line it up against a few other ideas on your radar.

- Target steadier returns by checking companies with reliable payouts through our 14 dividend fortresses and see how their income profiles compare.

- Hunt for potential value by scanning the 51 high quality undervalued stocks and see which names currently trade below our assessment of fair value.

- Prioritise resilience by reviewing companies in the 83 resilient stocks with low risk scores and focus on businesses that score better on our risk checks.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com