Hilltop Holdings (HTH) has drawn investor interest after recent trading left the shares near $38.60, with mixed short term returns but comparatively stronger gains over the past 3 months and over the past year.

See our latest analysis for Hilltop Holdings.

That recent pullback, including a 1-day share price return of a 1.3% decline and 7-day share price return of a 3.1% decline, sits against a stronger 30-day share price return of 10.2% and 1-year total shareholder return of 23.7%. This suggests momentum has been building over time even with short term volatility.

If Hilltop’s mix of banking and capital markets has your attention, it could be a good moment to broaden your search with our screener of 23 top founder-led companies.

So with Hilltop trading close to its US$38.67 analyst target and recent returns already in double digits, is there still mispricing to uncover here or are markets already factoring in most of the future growth?

Most Popular Narrative: 20% Undervalued

At a last close of $38.60 versus a most followed fair value estimate of $38.67, Hilltop Holdings is framed as modestly undervalued in the current narrative, with that view built on detailed assumptions about capital returns, margins and measured growth.

Management's disciplined approach to balance sheet and credit quality, characterized by declining nonperforming assets and ongoing loan portfolio upgrades, positions Hilltop to generate lower credit losses and stable net income, even during uncertain or adverse macroeconomic cycles.

Want to see what is behind that calm earnings profile? The narrative leans heavily on measured revenue growth, tighter margins and a richer future earnings multiple. Curious which exact trade offs were baked in to reach that $38.67 figure?

Result: Fair Value of $38.67 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, you still need to weigh up pressure on mortgage origination and higher noninterest costs, which could strain margins and unsettle that calm earnings story.

Find out about the key risks to this Hilltop Holdings narrative.

Another Angle: Earnings Multiple Sends A Different Signal

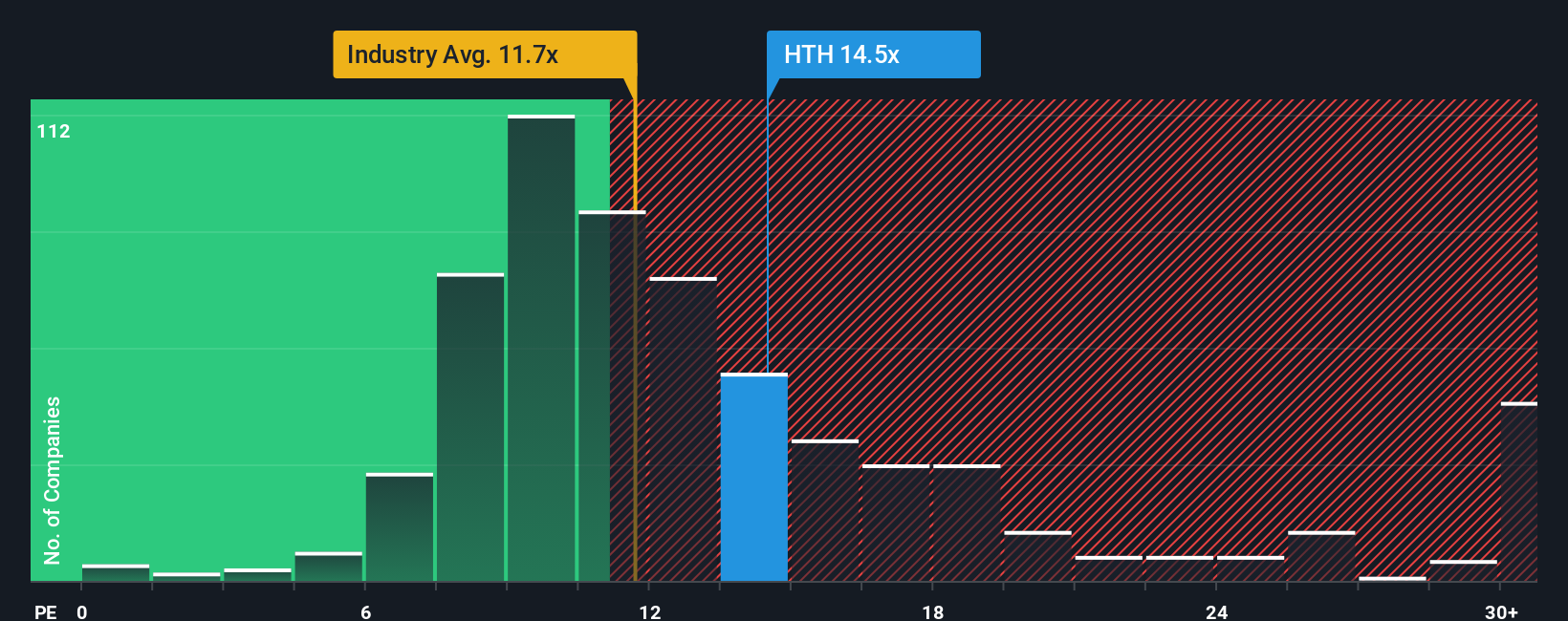

The fair value story you saw earlier leans on detailed forecasts and a richer future P/E. Yet on current numbers, Hilltop trades at a P/E of 13.9x, slightly above both US Banks at 11.8x and its peer average of 13.7x, and above a fair ratio of 9.1x.

That gap suggests the market is already paying a premium for Hilltop’s earnings, which could limit upside if growth or returns soften, or create room for a reset if expectations shift. With earnings forecast to decline by 10.6% a year, do you see that premium as justified or as valuation risk?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Hilltop Holdings Narrative

If parts of this story do not quite fit your view, or you would rather test every assumption yourself, you can build a custom Hilltop thesis in just a few minutes by starting with Do it your way.

A great starting point for your Hilltop Holdings research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Ready For More Investment Ideas?

If Hilltop has sharpened your thinking, do not stop here. Broaden your watchlist with focused stock ideas pulled from our data driven screeners.

- Target dependable income by reviewing 16 dividend fortresses that could appeal if you want yields above 5% with an emphasis on resilience.

- Hunt for potential mispricing with 55 high quality undervalued stocks that combine quality metrics and discounted valuations in one place.

- Prioritise capital preservation by checking 85 resilient stocks with low risk scores where our risk scoring highlights companies with steadier profiles.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com