Gorman-Rupp (GRC) is back on investors’ radar after reporting fourth quarter and full year 2025 results, with both sales and net income above the prior year, and analysts lifting earnings expectations.

See our latest analysis for Gorman-Rupp.

The share price has reacted strongly to the earnings beat, with a 31.07% 1 month share price return and 48.36% 3 month share price return helping lift the 1 year total shareholder return to 79.88%. This points to accelerating momentum off a higher base.

If strong recent gains in an industrial name have you thinking about where else growth stories might be emerging, our 24 power grid technology and infrastructure stocks is a straightforward way to uncover other infrastructure linked opportunities.

With the shares up sharply and trading close to the current US$67.50 analyst price target, the key question now is whether Gorman-Rupp is still undervalued or if the market is already pricing in future growth.

Price to earnings of 33.2x: Is it justified?

On earnings alone, Gorman-Rupp looks expensive at a P/E of 33.2x, especially with the last close at $66.82 sitting just below the $67.50 analyst target and our DCF estimate of $59.97.

The P/E ratio compares what you pay today to the company’s current earnings. A higher multiple usually signals the market is willing to pay up for profit quality or future growth. For Gorman-Rupp, that richer multiple sits against a reported backdrop of 32.2% earnings growth over the past year, high quality earnings, and profit growth that has been running at 17.3% per year over the past 5 years.

That said, the current 33.2x P/E is above the estimated fair P/E of 20.9x and also above the wider US Machinery industry average of 29.8x. This suggests the market is placing a premium on the company that could compress if expectations cool. At the same time, Gorman-Rupp’s P/E screens as good value relative to a peer group average of 51.5x, which shows how different investor expectations can be within the same space and gives a sense of where the multiple could reasonably reset over time.

Explore the SWS fair ratio for Gorman-Rupp

Result: Price-to-earnings of 33.2x (OVERVALUED)

However, if earnings expectations ease or sector sentiment turns, the current premium P/E and tight gap to the US$67.50 target could quickly look stretched.

Find out about the key risks to this Gorman-Rupp narrative.

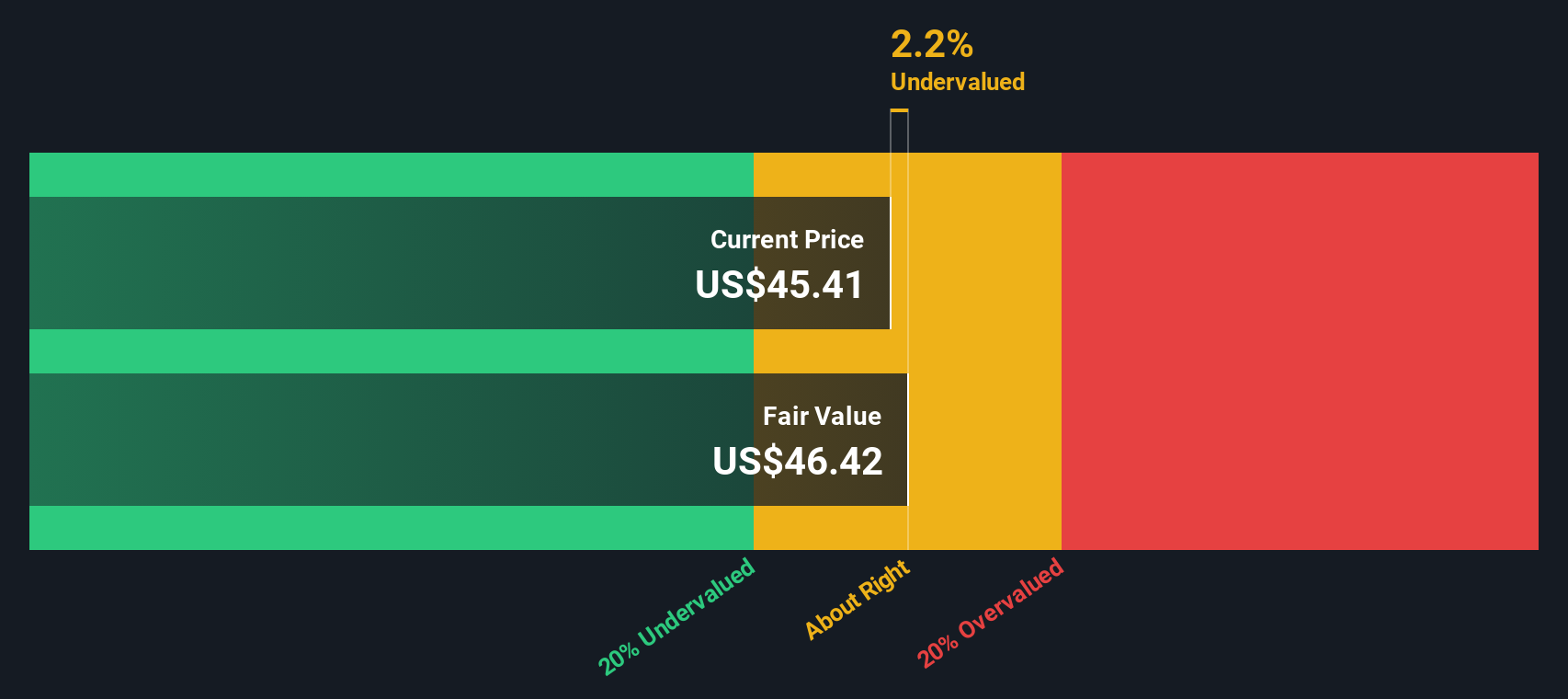

Another view: our DCF suggests less upside

While the 33.2x P/E already looks rich, our DCF model paints a similar picture, with a value of $59.97 versus the $66.82 share price. That gap implies limited margin for disappointment if growth, returns or sentiment come in softer than hoped.

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Gorman-Rupp for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 55 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Gorman-Rupp Narrative

If you see the numbers differently or simply prefer to test your own view against the data, you can build a personalised narrative in just a few minutes, starting with Do it your way.

A great starting point for your Gorman-Rupp research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If Gorman-Rupp has sharpened your focus, do not stop here; use the Simply Wall St Screener to uncover fresh ideas that match your investing style.

- Spot potential mispricings early by scanning our list of 55 high quality undervalued stocks that pair solid fundamentals with appealing price tags.

- Secure income focused ideas by reviewing 16 dividend fortresses, built for investors who care about yield and staying power.

- Prioritise resilience by checking 85 resilient stocks with low risk scores, so you are not missing companies with steadier risk profiles.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com