A Look At ProFrac Holding (ACDC) Valuation After Recent Share Price Momentum And Conflicting Fair Value Estimates

ProFrac Holding (ACDC) has drawn attention after recent trading, with the stock closing at US$5.47 and showing sharply different results over the past month, past 3 months, and year.

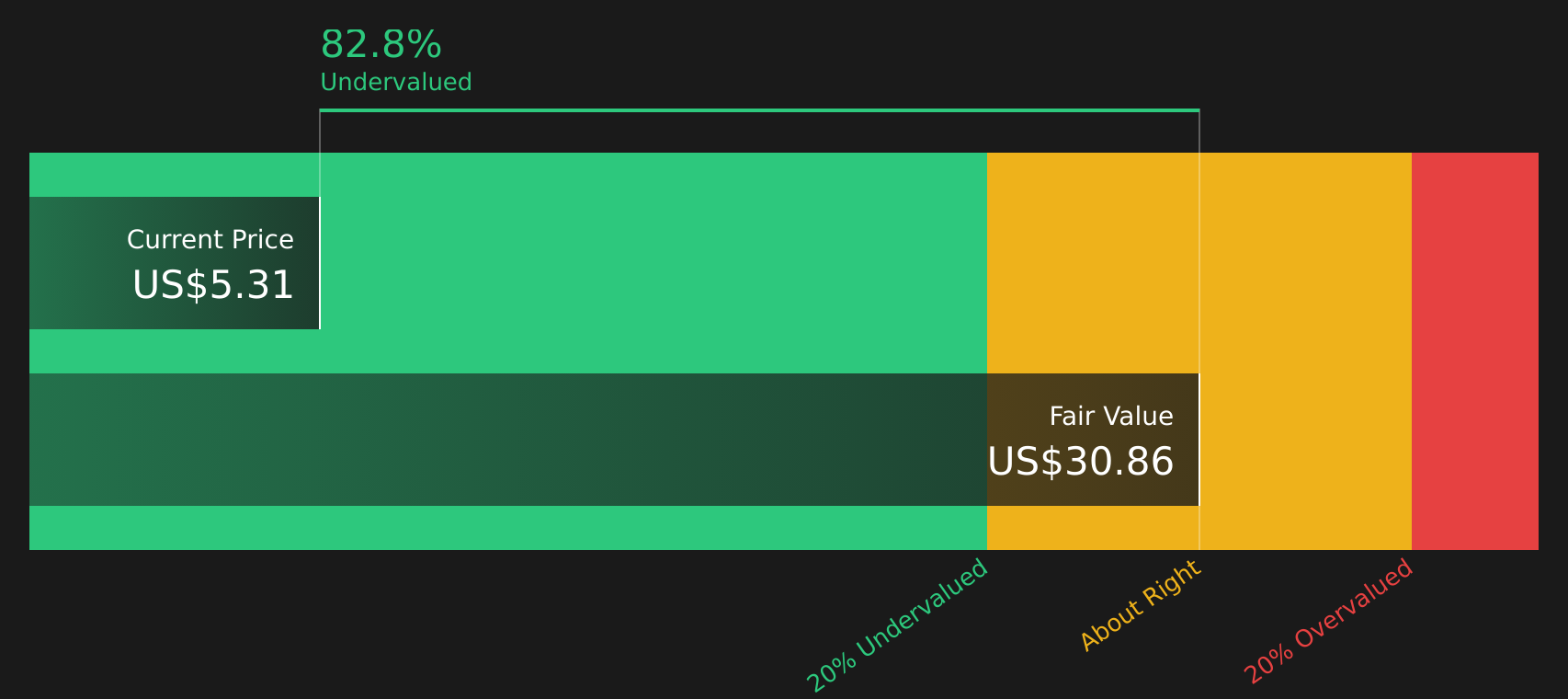

See our latest analysis for ProFrac Holding.

The recent 30-day share price return of 27.51% and 90-day share price return of 43.19% contrast with a 1-year total shareholder return decline of 31.02% and a 3-year total shareholder return decline of 74.22%. This suggests that short-term momentum has picked up after a difficult period for long-term holders.

If this swing in sentiment has you looking beyond a single name, it could be a good moment to broaden your search with our 23 top founder-led companies.

The stock trades around US$5.47 and sits at an estimated 82% discount to one intrinsic value estimate, even as analysts see downside to their US$4.00 target. Is this a contrarian opportunity, or is the market already pricing in future growth?

Most Popular Narrative: 36.7% Overvalued

ProFrac Holding last closed at $5.47, while the most followed narrative anchors fair value at $4.00. This implies a meaningful valuation gap that relies heavily on future margin and earnings assumptions.

Analysts are assuming ProFrac Holding's revenue will decrease by 0.5% annually over the next 3 years.

Analysts are not forecasting that ProFrac Holding will become profitable in the next 3 years. To represent the Analyst Price Target as a Future PE Valuation we will estimate ProFrac Holding's profit margin will increase from -13.1% to the average US Energy Services industry of 7.0% in 3 years.

If you want to see what bridges an unprofitable business to healthier margins and a re-rated earnings multiple in a few years, the full narrative spells out the revenue path, margin reset, and valuation math behind that $4.00 figure without assuming a smooth ride.

Result: Fair Value of $4.00 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, the story can change quickly if commodity price swings continue to pressure utilization or if high capital needs and US$1.11b of debt strain the balance sheet.

Find out about the key risks to this ProFrac Holding narrative.

Another Angle on Valuation

While the most followed narrative tags ProFrac Holding as 36.7% overvalued at a $4.00 fair value, the SWS DCF model points in the opposite direction, with an estimated future cash flow value of $30.98 per share. When one framework sees a discount of more than 80% and another signals downside, which set of assumptions do you find more convincing?

Look into how the SWS DCF model arrives at its fair value.

Build Your Own ProFrac Holding Narrative

If you look at these numbers and reach a different conclusion, or simply prefer to work from your own assumptions, you can build a personalised thesis in just a few minutes, starting with Do it your way.

A great starting point for your ProFrac Holding research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If ProFrac's mixed signals have you thinking about broader options, this is the moment to widen your watchlist and test a few different angles.

- Target dependable compounding potential by checking out companies with robust cash flows and attractive valuations using our 53 high quality undervalued stocks.

- Prioritise resilience by scanning for companies in our 85 resilient stocks with low risk scores that pair lower risk scores with fundamentals you can scrutinise in detail.

- Get ahead of the crowd by reviewing our screener containing 23 high quality undiscovered gems that highlight quality businesses the market may not be fully focused on yet.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com