Adient (NYSE:ADNT) is back in focus after raising its fiscal 2026 revenue guidance to US$14.6b, updating investors on first quarter results, and confirming completion of a sizeable multi year share repurchase program.

See our latest analysis for Adient.

The stronger fiscal 2026 guidance, multi year buyback completion, and recent analyst target price increases have come alongside a 90 day share price return of 35.31% and a 1 year total shareholder return of 58.05%. However, the 3 year total shareholder return of negative 39.26% shows the longer term picture is still catching up. Momentum in the last month and year to date has been positive, with the share price recently closing at US$27.09.

If this kind of rebound catches your eye, it could be a good moment to broaden your search and check out our screener of 23 top founder-led companies as potential next ideas.

With guidance now pointing to US$14.6b in fiscal 2026 revenue, a completed US$490.06m buyback, and the stock trading below the average analyst target, is Adient still undervalued, or has the market already priced in future growth?

Most Popular Narrative: 8.1% Overvalued

Adient's most followed narrative places fair value at $25.05, slightly below the recent $27.09 close. This frames the current rally as a stretch above that estimate.

Adient's robust free cash flow generation and ongoing debt reduction, coupled with disciplined capital allocation (including continued share buybacks), are likely to enhance EPS and shareholder returns over time, reducing balance sheet risk and supporting a sustainable long-term earnings trajectory.

Want to see what is sitting behind that fair value call? Revenue assumptions are restrained, margin repair is central, and the future earnings multiple may surprise you.

Result: Fair Value of $25.05 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, there are still real pressure points, including margin weakness in Europe and uncertainty around China volumes, that could upset the current fair value story.

Find out about the key risks to this Adient narrative.

Another Angle on Value

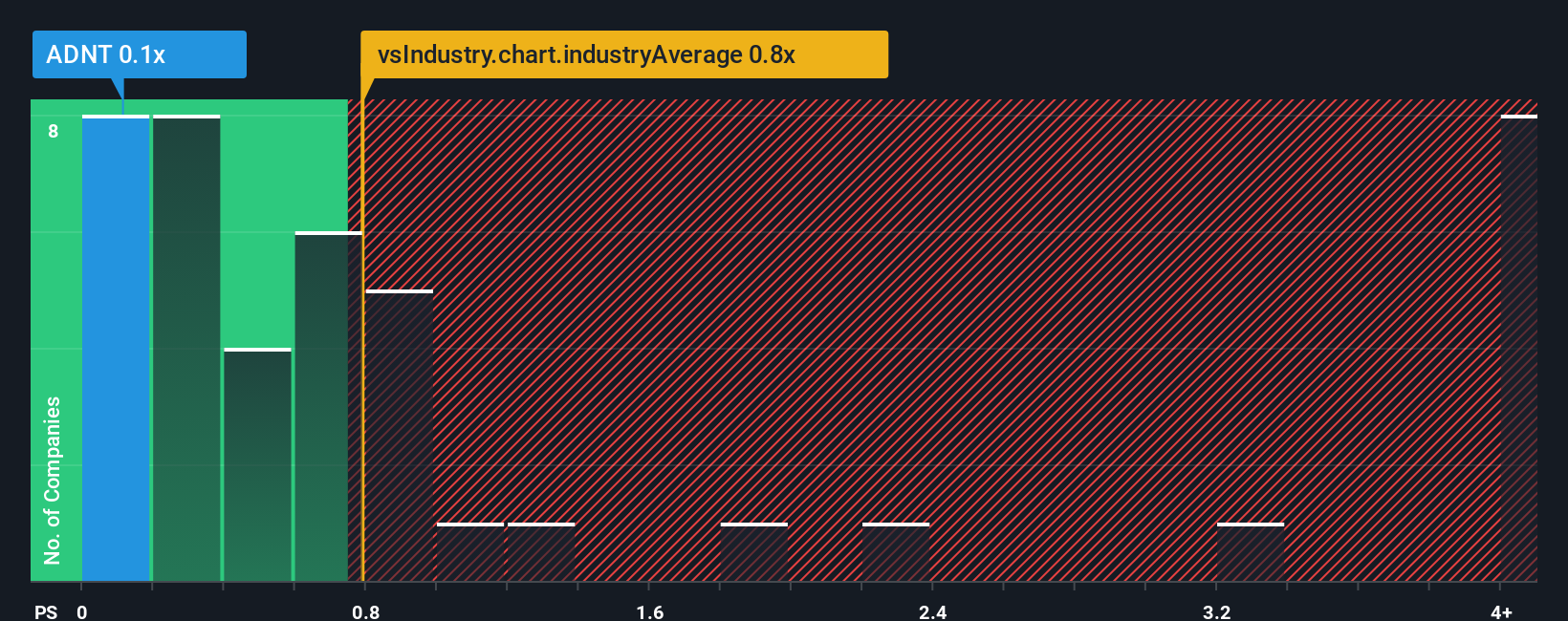

The narrative model says Adient looks about 8.1% overvalued around $27.09, with fair value at $25.05. Yet on simple pricing, the stock trades on a P/S of roughly 0.1x against an industry average of 0.8x and a fair ratio of 0.4x, which hints at a very different story.

That gap suggests the market could be pricing in a lot of execution risk, or it is overlooking potential recovery in earnings power. Which side of that trade do you feel more comfortable with?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Adient Narrative

If you see the numbers differently or prefer to stress test your own assumptions, you can build a custom view in just a few minutes: Do it your way.

A good starting point is our analysis highlighting 3 key rewards investors are optimistic about regarding Adient.

Looking for more investment ideas?

If Adient has you thinking about where else value could be hiding, do not stop here. Use the tools available to you and keep building your watchlist.

- Spot potential value opportunities quickly by checking companies our screener tags as 53 high quality undervalued stocks based on their fundamentals.

- Prioritize balance sheet strength and financial resilience by reviewing stocks in our solid balance sheet and fundamentals stocks screener (44 results) that may handle tougher conditions more comfortably.

- Hunt for lesser known opportunities by scanning our screener containing 23 high quality undiscovered gems that combine quality metrics with limited market attention.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com