- Investors may be wondering if Peoples Bancorp at around US$33.56 is offering fair value today, or if the current price is leaving some potential upside on the table.

- The stock has had a mixed run lately, with a 1.8% decline over the last 7 days, an 8.8% gain over 30 days, 11.3% year to date, and 8.6% over the past year, while the 3 year and 5 year returns sit at 28.1% and 39.4% respectively.

- Recent attention on Peoples Bancorp has centered on ongoing corporate developments and sector wide sentiment around regional banks. These factors can influence how investors think about risk and pricing for smaller financial institutions. That backdrop helps explain why the share price has been moving in fits and starts rather than in a straight line.

- On our checks, Peoples Bancorp scores a 5 out of 6 valuation score, which suggests it screens as undervalued on most of the standard yardsticks discussed next, and also sets up a discussion later on about a more complete way to think about what the stock might be worth.

Find out why Peoples Bancorp's 8.6% return over the last year is lagging behind its peers.

Approach 1: Peoples Bancorp Excess Returns Analysis

The Excess Returns model looks at how much profit a company can generate above the return that equity investors typically require, and then capitalizes those extra profits into a per share value. For Peoples Bancorp, the starting point is its book value of US$34.53 per share and a stable book value estimate of US$36.54 per share, based on forecasts from 7 analysts.

Analysts estimate stable earnings of US$3.53 per share, drawn from future Return on Equity expectations from 6 analysts. The model applies a cost of equity of US$2.66 per share, which leaves an excess return of US$0.87 per share. That excess, combined with an average Return on Equity of 9.65%, is used to estimate how much value the bank might add over time on top of its equity base.

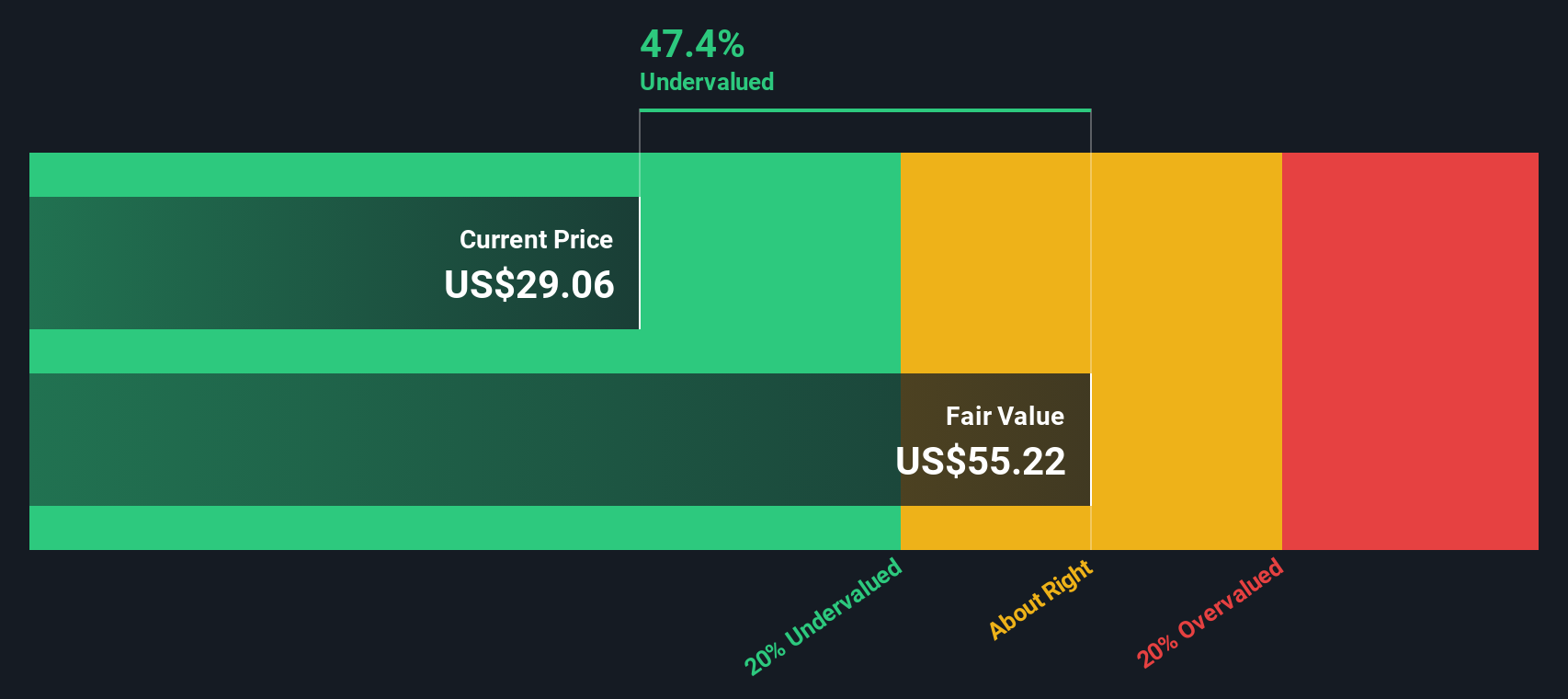

Putting those inputs together, the Excess Returns approach arrives at an intrinsic value estimate of about US$58.91 per share. Compared with the recent share price around US$33.56, this implies the stock screens as 43.0% undervalued under this framework.

Result: UNDERVALUED

Our Excess Returns analysis suggests Peoples Bancorp is undervalued by 43.0%. Track this in your watchlist or portfolio, or discover 53 more high quality undervalued stocks.

Approach 2: Peoples Bancorp Price vs Earnings

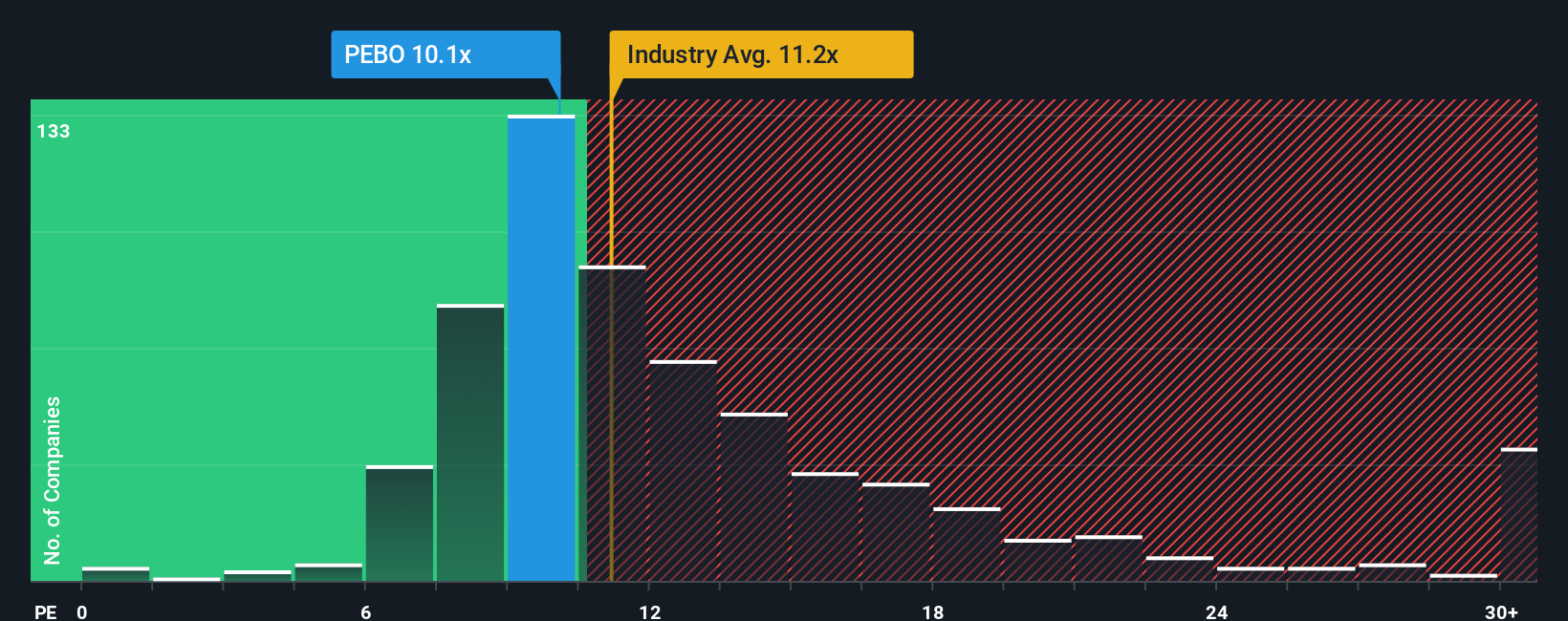

For a bank that is generating profits, the P/E ratio is a useful shorthand for how much investors are paying for each dollar of earnings. It ties directly to what you see on the income statement and is one of the most common ways the market compares banks of different sizes.

What feels like a normal or fair P/E often comes down to two things: how fast earnings are expected to grow and how risky those earnings appear to be. Higher expected growth or lower perceived risk can support a higher multiple, while slower growth or higher uncertainty usually lines up with a lower one.

Peoples Bancorp currently trades on a P/E of 11.08x. That sits below both the peer group average of 14.31x and the broader Banks industry average of 11.89x. Simply Wall St also calculates a Fair Ratio of 11.47x, which is the P/E level it would expect for Peoples Bancorp given factors such as its earnings profile, margins, market value, industry risks and company specific risks. This Fair Ratio can be more useful than a straight peer or industry comparison because it adjusts for those company specific features rather than assuming all banks deserve the same multiple. With the actual P/E at 11.08x versus a Fair Ratio of 11.47x, the stock screens as slightly undervalued on this basis.

Result: UNDERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 23 top founder-led companies.

Upgrade Your Decision Making: Choose your Peoples Bancorp Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives. These are simply your story about Peoples Bancorp linked directly to your own forecast for its revenue, earnings, margins and fair value. All of this is captured in an easy tool on Simply Wall St's Community page that compares your Fair Value to the current price and then updates automatically when new news or earnings arrive. One investor might build a more optimistic Peoples Bancorp Narrative around strong local economic trends, digital banking and credit quality improving over time, while another might focus on margin pressure, credit risks and funding costs. This can lead to a different fair value and a different view on whether the current price near the US$34.17 analyst target looks attractive or not.

Do you think there's more to the story for Peoples Bancorp? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com