A Look At CarMax (KMX) Valuation After Keith Barr Is Named New CEO

Why Keith Barr’s appointment matters for CarMax (KMX)

CarMax (KMX) has put leadership change at the center of its turnaround effort, appointing former InterContinental Hotels Group chief executive Keith Barr as president, CEO, and board member effective March 16, 2026.

The board is turning to Barr’s experience in large consumer businesses, digital transformation, and customer experience to address CarMax’s ongoing sales and profitability challenges and to help shape the company’s next phase of development.

See our latest analysis for CarMax.

Investors have reacted cautiously to the CEO news, with a 1 day share price return of 1.15% not offsetting a 7 day share price return decline of 10.83%. The 90 day share price return of 23.89% contrasts sharply with a 1 year total shareholder return decline of 53.40%, suggesting recent momentum has picked up after a much tougher period for long term holders.

If this leadership change has you thinking about where else management quality might matter, it could be a good moment to broaden your search and check out 23 top founder-led companies.

With CarMax shares down 53% over 1 year but up 24% over 90 days and trading at roughly a 38% discount to one intrinsic value estimate, you have to ask: is there still an entry point here, or is the market already pricing in a Keith Barr turnaround?

Most Popular Narrative: 8% Overvalued

The most followed narrative puts CarMax’s fair value at $38.31 per share, slightly below the last close at $41.43, and builds its case around credit risk and execution.

Macroeconomic and competitive pressures challenge CarMax's margins and growth, with rising inventory and loan costs and uncertainties affecting profitability and strategic clarity.

CarMax's initiative to broaden its full credit spectrum lending capabilities through CarMax Auto Finance (CAF) is expected to increase CAF income and net interest margins over time. This initiative aims to capture more sales and improve financing income, impacting earnings positively.

Want to see how a tougher credit backdrop and a bigger lending push can still support a premium valuation? The narrative leans heavily on steadier margins, modest top line progress, and a future earnings base that assumes cleaner execution than recent history. Curious which specific revenue and profit assumptions sit behind that $38.31 figure, and how sensitive it is to small changes in those inputs? Result: Fair Value of $38.31 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, there is still the risk that higher loan loss provisions at CarMax Auto Finance, along with ongoing pressure on wholesale unit margins, could weaken the case for a premium valuation.

Find out about the key risks to this CarMax narrative.

Another way to look at CarMax’s value

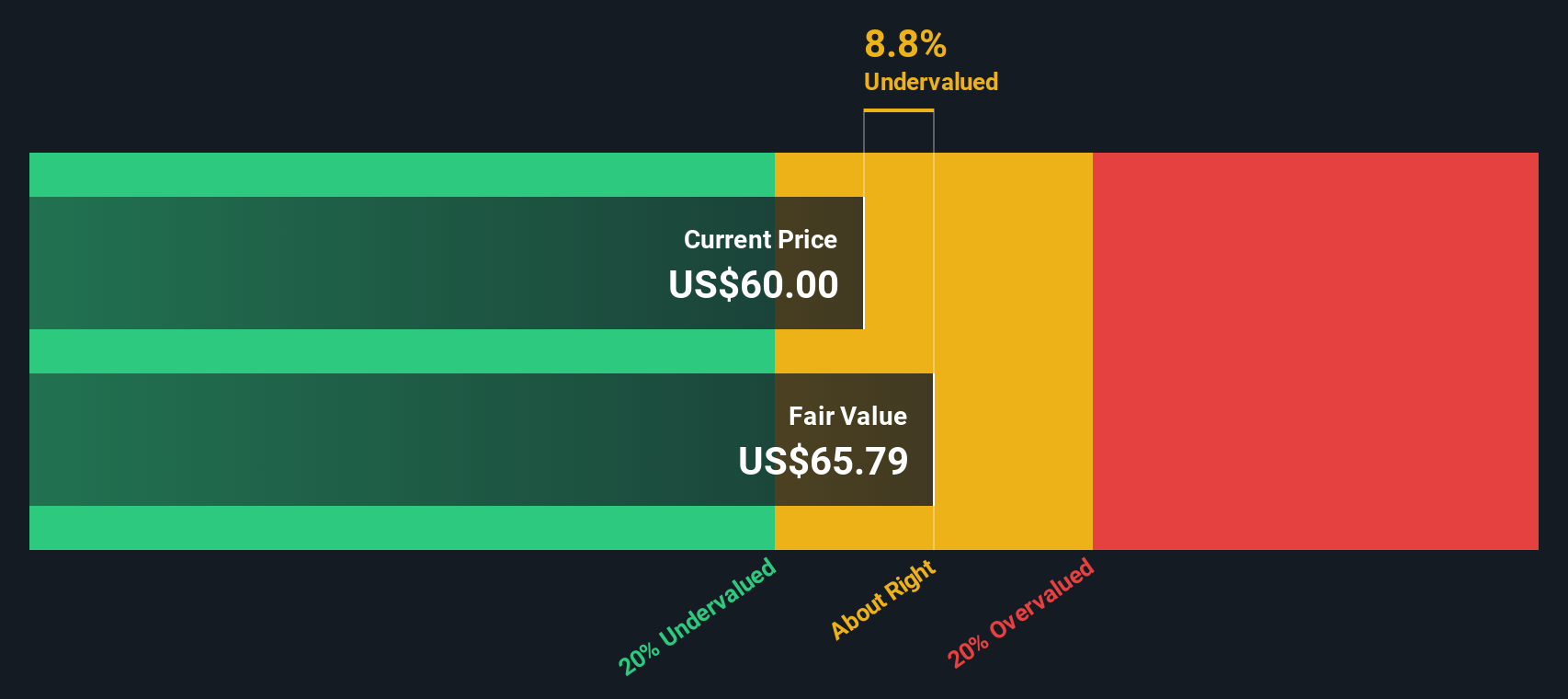

The narrative fair value of $38.31 suggests CarMax is slightly overvalued at $41.43. However, our DCF model comes to a very different conclusion, with an estimated future cash flow value of $66.38 per share, which points to meaningful upside instead. Which story do you think fits better with the risks you see?

Look into how the SWS DCF model arrives at its fair value.

Build Your Own CarMax Narrative

If you look at these numbers and feel you see a different story, you can test your own assumptions, shape your thesis, and Do it your way in just a few minutes.

A great starting point for your CarMax research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If CarMax has sharpened your thinking, do not stop here, broaden your watchlist with other ideas that line up with the kind of portfolio you want to build.

- Target quality at a discount by scanning 54 high quality undervalued stocks that combine solid fundamentals with prices that may sit below some intrinsic value estimates.

- Strengthen your income stream by reviewing 13 dividend fortresses that focus on higher yielding companies with an emphasis on stability.

- Dial back portfolio risk by checking 83 resilient stocks with low risk scores built around businesses with more resilient risk profiles.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com