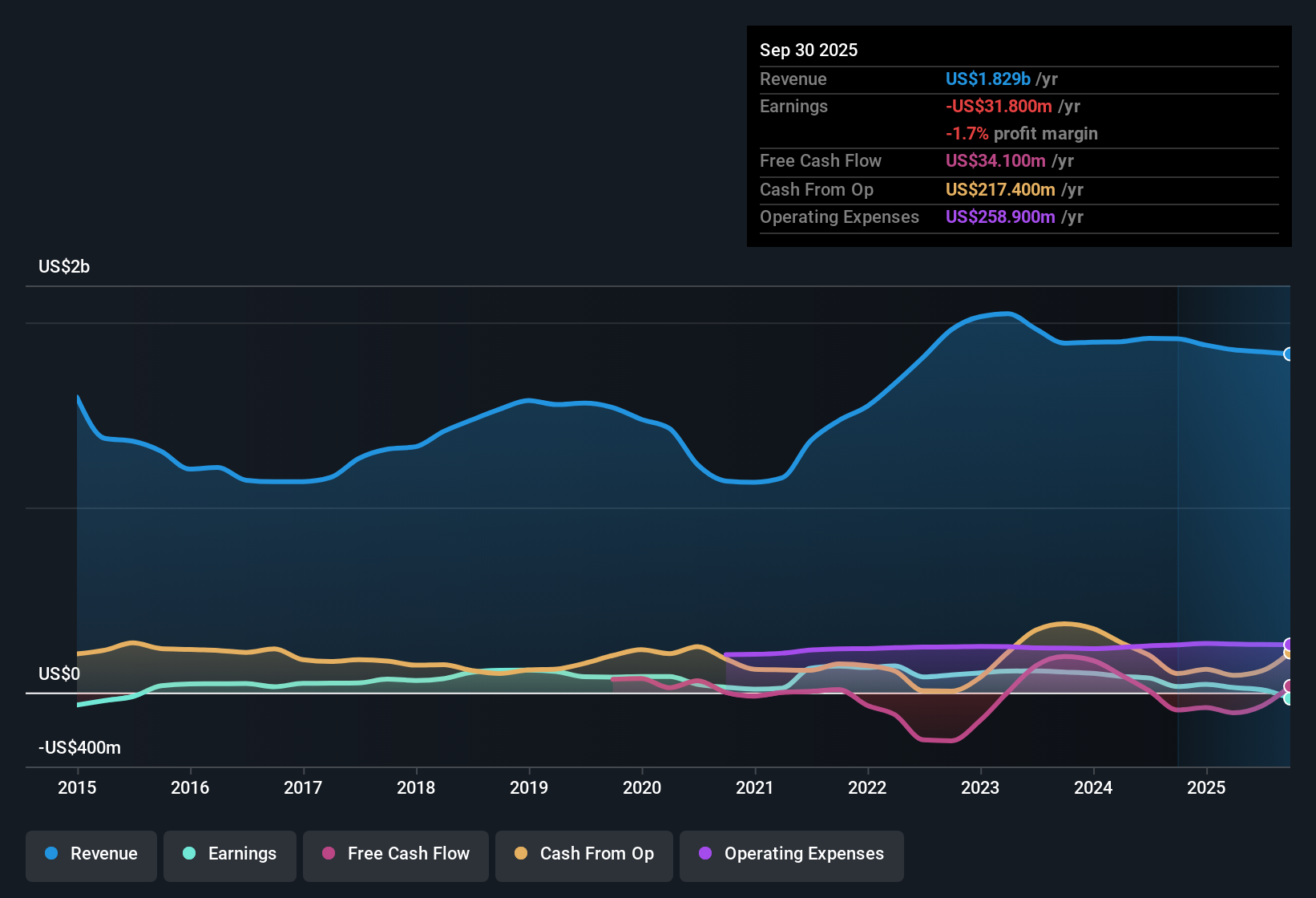

Orion (OEC) closed out FY 2025 with Q4 revenue of US$411.7 million and a basic EPS loss of US$0.38, alongside full year trailing revenue of about US$1.8 billion and a loss of US$1.24 per share. Over the past six quarters, the company has seen quarterly revenue move between US$434.2 million and US$477.7 million while basic EPS has swung from a profit of roughly US$0.30 per share to a loss of US$1.20 per share. This highlights a choppy earnings profile that feeds straight through to margins. With analysts in the dataset expecting strong earnings growth over time, this latest print puts the spotlight squarely on whether Orion can turn those volatile margins into a more reliable profit story.

See our full analysis for Orion.With the headline numbers on the table, the next step is to set these results against the widely followed market narratives around Orion to see which stories hold up and which start to look out of date.

See what the community is saying about Orion

Losses On A Trailing Basis Despite US$1.8b In Sales

- On a trailing 12 month view, Orion generated about US$1.8b of revenue but reported a net loss of US$70.1 million and basic EPS of US$1.24 loss, underlining that solid sales have not translated into profits recently.

- Consensus narrative talks about revenue growing 2.5% a year and margins lifting from 1.4% to 7.8%. However, the current loss and negative EPS show that any margin rebuild is starting from a period where trailing profits are still in the red, which may make the planned shift toward higher margin Specialty products more important than the headline growth rate.

Quarterly Swings Highlight Margin Volatility

- Over FY 2025, net income moved from US$9.1 million profit in Q1 to a US$67.1 million loss in Q3, then to a smaller US$21.1 million loss in Q4, with basic EPS ranging from US$0.16 profit to US$1.20 loss, which signals that earnings have been quite sensitive to short term factors.

- Bulls argue that operational upgrades and cost leadership can lift margins by up to 250 basis points. Yet the wide EPS range across just six quarters suggests that recurring equipment issues, maintenance needs or mix shifts can still swing results meaningfully from one quarter to the next, which is an important check on the more upbeat margin story.

Cheap Sales Multiple Versus DCF Signal

- Orion trades on a P/S of 0.2x versus 0.4x for peers and 1.2x for the wider US Chemicals group, yet the current share price of US$5.74 sits above the DCF fair value of about US$2.13, so relative and cash flow based signals are pointing in different directions.

- Bears highlight that trailing losses have grown at roughly 14.9% a year over five years and that interest payments and a 1.44% dividend are not well covered by earnings, which fits with a cautious read on the DCF gap where a higher market price than the DCF fair value may look hard to justify while profitability and coverage ratios remain weak.

Next Steps

To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for Orion on Simply Wall St. Add the company to your watchlist or portfolio so you'll be alerted when the story evolves.

If this mix of risks and potential rewards feels finely balanced, take a closer look at the numbers yourself and form your own stance. The quickest way to round out your view is to weigh up the 2 key rewards and 2 important warning signs.

See What Else Is Out There

Orion’s recent losses despite roughly US$1.8b in sales, margin volatility and uncovered dividend highlight that earnings quality and downside risk are key concerns for shareholders.

If that level of uncertainty feels uncomfortable, it could be worth scanning 81 resilient stocks with low risk scores today to focus on companies with steadier fundamentals and fewer surprises.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com