As February begins, major U.S. stock indexes have shown strong performance, with the Dow Jones Industrial Average climbing 515 points and the S&P 500 nearing a record high. Amid this positive momentum, investors may find opportunities in stocks that appear to be trading below their estimated fair value, potentially offering attractive entry points in a market characterized by robust gains and evolving economic conditions.

Top 10 Undervalued Stocks Based On Cash Flows In The United States

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Zeta Global Holdings (ZETA) | $15.31 | $29.52 | 48.1% |

| WesBanco (WSBC) | $36.61 | $70.40 | 48% |

| Viant Technology (DSP) | $9.20 | $17.87 | 48.5% |

| Peraso (PRSO) | $0.878 | $1.70 | 48.4% |

| Nutanix (NTNX) | $40.95 | $78.70 | 48% |

| Northwest Bancshares (NWBI) | $13.03 | $25.63 | 49.2% |

| Midland States Bancorp (MSBI) | $23.12 | $44.96 | 48.6% |

| First Busey (BUSE) | $26.54 | $51.50 | 48.5% |

| BioLife Solutions (BLFS) | $22.36 | $43.29 | 48.3% |

| Alphatec Holdings (ATEC) | $13.50 | $26.12 | 48.3% |

Underneath we present a selection of stocks filtered out by our screen.

AerSale (ASLE)

Overview: AerSale Corporation supplies aftermarket commercial aircraft, engines, and parts to a diverse range of clients globally, including airlines and government contractors, with a market cap of approximately $341.62 million.

Operations: The company's revenue segments consist of Tech Ops - MRO Services generating $95.08 million, Tech Ops - Product Sales contributing $25.34 million, Asset Management Solutions - Engine bringing in $185.29 million, and Asset Management Solutions - Aircraft accounting for $33.38 million.

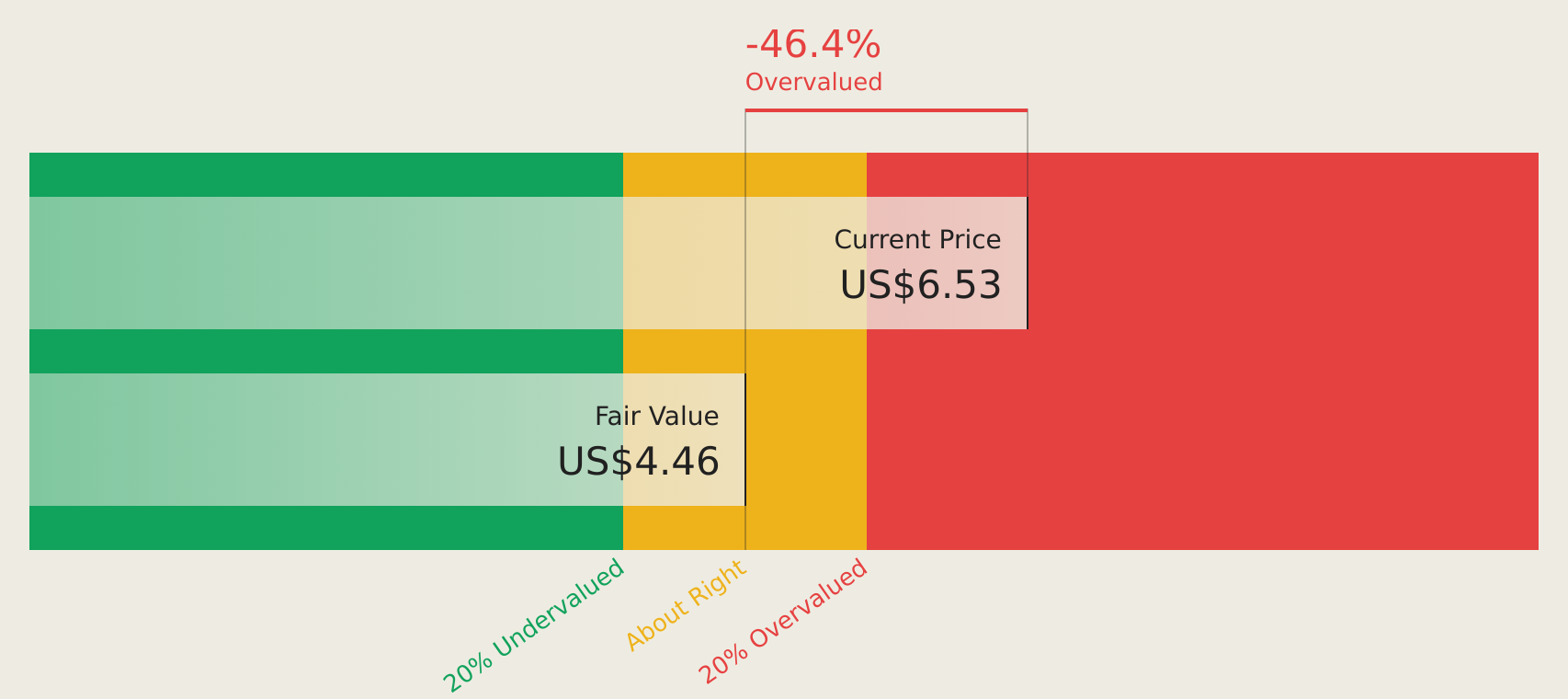

Estimated Discount To Fair Value: 44.5%

AerSale is trading at US$7.36, significantly below its estimated future cash flow value of US$13.26, suggesting it may be undervalued based on cash flows. Its earnings are forecast to grow significantly at 63.7% annually, outpacing the broader U.S. market's growth rate of 15.6%. Recent expansion with a new MRO facility in Florida enhances capacity and operational efficiency, potentially supporting future revenue growth despite slower expected revenue increases compared to its earnings trajectory.

- Our comprehensive growth report raises the possibility that AerSale is poised for substantial financial growth.

- Take a closer look at AerSale's balance sheet health here in our report.

Bank of Marin Bancorp (BMRC)

Overview: Bank of Marin Bancorp, with a market cap of $434.52 million, operates as the holding company for Bank of Marin and offers financial services to small to medium-sized businesses, not-for-profit organizations, and commercial real estate investors in the United States.

Operations: The company generates revenue primarily through its Community Banking segment, which accounted for $33.02 million.

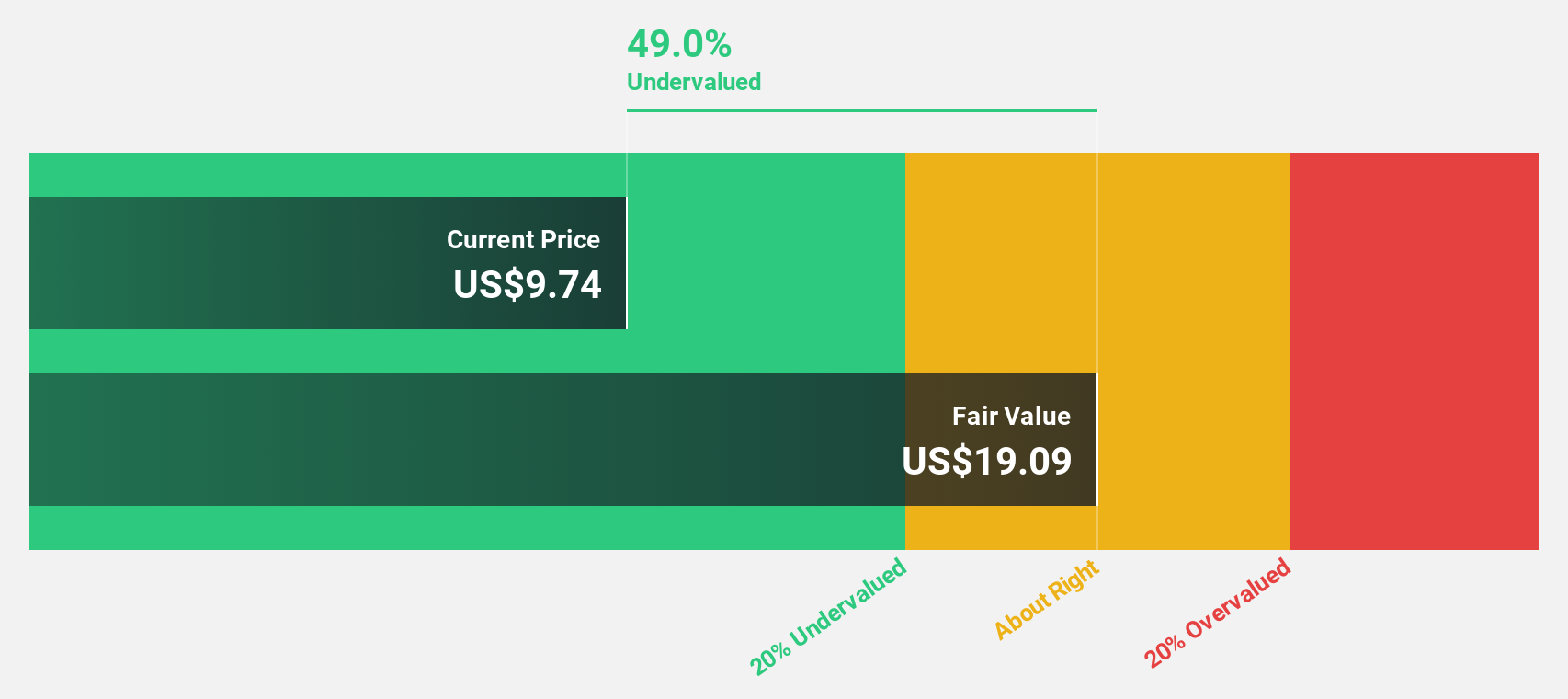

Estimated Discount To Fair Value: 38%

Bank of Marin Bancorp, trading at US$27.43, is valued below its estimated future cash flow value of US$44.21, indicating potential undervaluation based on cash flows. Despite a net loss of US$35.68 million in 2025 and recent impairments, revenue is forecast to grow significantly at 54.5% annually, surpassing the U.S. market average growth rate. However, the dividend sustainability remains questionable as it isn't well covered by earnings currently or in forecasts.

- The analysis detailed in our Bank of Marin Bancorp growth report hints at robust future financial performance.

- Navigate through the intricacies of Bank of Marin Bancorp with our comprehensive financial health report here.

Semrush Holdings (SEMR)

Overview: Semrush Holdings, Inc. operates an online visibility management SaaS platform across the United States, the United Kingdom, and internationally with a market cap of approximately $1.79 billion.

Operations: The company's revenue primarily comes from its Software & Programming segment, which generated $428.63 million.

Estimated Discount To Fair Value: 12.9%

Semrush Holdings, trading at US$11.81, is undervalued based on its future cash flow value of US$13.57. Despite recent volatility and significant insider selling, the company anticipates robust earnings growth of 118.22% annually over the next three years, outpacing market averages. The planned acquisition by Adobe for US$2 billion could further influence its valuation dynamics as it transitions into a wholly owned subsidiary, pending regulatory approvals and shareholder agreement completion in early 2026.

- In light of our recent growth report, it seems possible that Semrush Holdings' financial performance will exceed current levels.

- Click here to discover the nuances of Semrush Holdings with our detailed financial health report.

Seize The Opportunity

- Click this link to deep-dive into the 155 companies within our Undervalued US Stocks Based On Cash Flows screener.

- Already own these companies? Bring clarity to your investment decisions by linking up your portfolio with Simply Wall St, where you can monitor all the vital signs of your stocks effortlessly.

- Maximize your investment potential with Simply Wall St, the comprehensive app that offers global market insights for free.

Searching for a Fresh Perspective?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com