Did Otter Tail’s (OTTR) Renewable-Focused Capex and Lower EPS Guidance Just Recast Its Investment Narrative?

- In February 2026, Otter Tail Corporation reported its fourth quarter and full-year 2025 results, showing higher quarterly sales of US$149.71 million but lower net income of US$51.77 million, alongside full-year diluted EPS from continuing operations of US$6.55 and new 2026 diluted EPS guidance of US$5.22 to US$5.62.

- The company also lifted its dividend for the 88th consecutive year and outlined a US$1.90 billion-plus capital plan centered on renewables, transmission, and battery storage, to be funded without issuing new equity while absorbing weaker earnings expected from its Plastics segment.

- Now, we'll assess how this fresh 2026 earnings guidance and large renewable-focused capital plan reshape Otter Tail's existing investment narrative.

Capitalize on the AI infrastructure supercycle with our selection of the 34 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

Otter Tail Investment Narrative Recap

To own Otter Tail today, you need to be comfortable with a story that pairs a regulated utility growth plan with more cyclical Manufacturing and Plastics earnings. The new 2026 EPS guidance, which sits below 2025’s US$6.55, reinforces that the key near term catalyst is execution on regulated rate base growth, while the biggest current risk remains pressure from normalization in Plastics profitability. This latest update does not meaningfully change that overall balance.

The reaffirmed US$1.90 billion-plus capital plan through 2030, focused on renewables, transmission, and battery storage, is the announcement that most directly frames this earnings release. It underpins management’s emphasis on utility investment and rate base growth as the primary driver of future results, even as the 2026 guidance acknowledges weaker Plastics earnings in the near term.

But investors should also be aware that reliance on Plastics cash flows to fund utility growth without new equity could...

Read the full narrative on Otter Tail (it's free!)

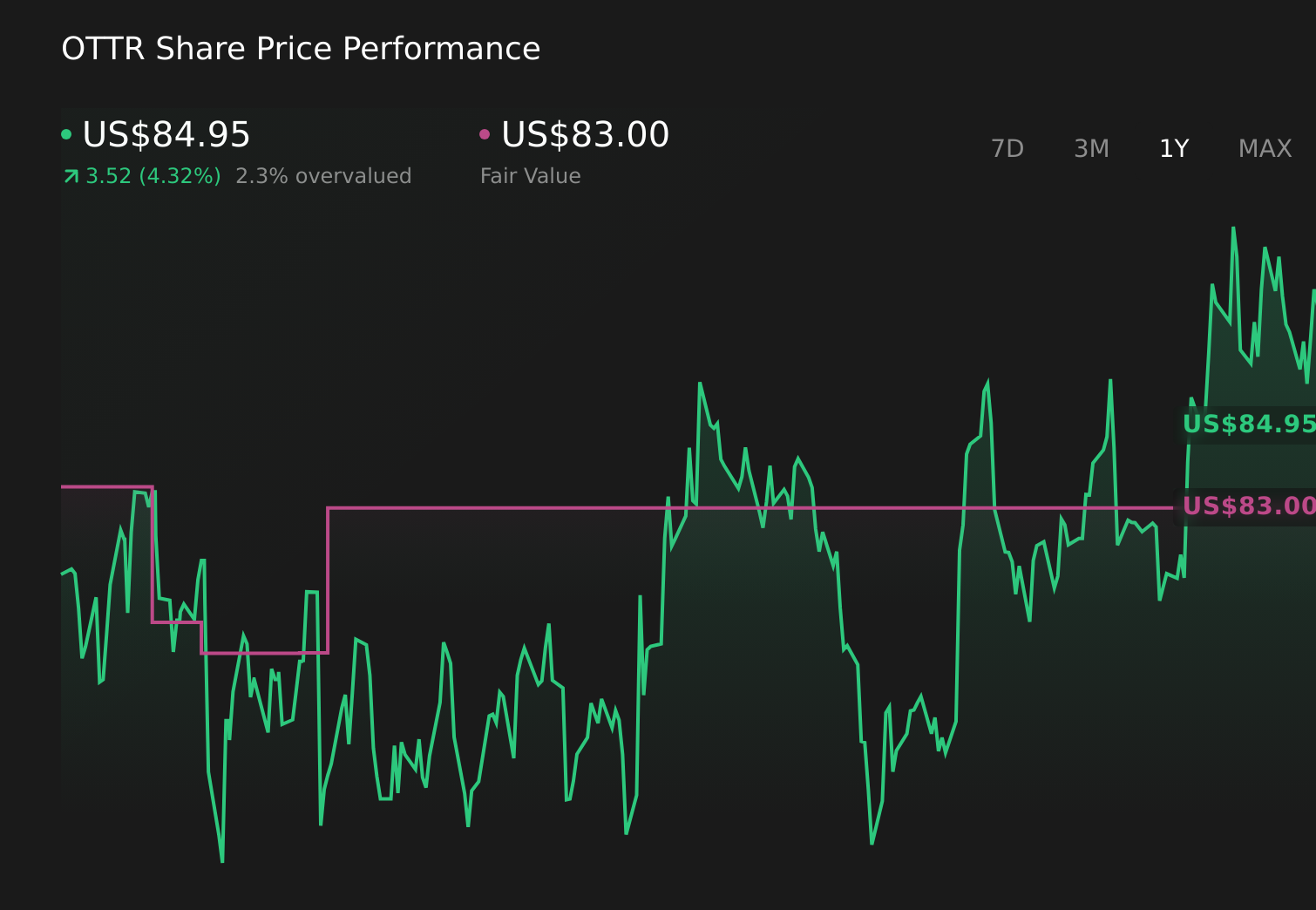

Otter Tail's narrative projects $1.4 billion revenue and $195.9 million earnings by 2028.

Uncover how Otter Tail's forecasts yield a $83.00 fair value, a 4% downside to its current price.

Exploring Other Perspectives

Four fair value estimates from the Simply Wall St Community span a wide range, from about US$2 to US$83 per share, underscoring very different expectations. When you set that against Otter Tail’s large renewable focused utility investment plan and near term earnings pressure in Plastics, it is worth exploring how different investors connect those factors to future performance.

Explore 4 other fair value estimates on Otter Tail - why the stock might be worth less than half the current price!

Form Your Own Verdict

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Otter Tail research is our analysis highlighting 1 key reward and 2 important warning signs that could impact your investment decision.

- Our free Otter Tail research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Otter Tail's overall financial health at a glance.

Ready To Venture Into Other Investment Styles?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

- This technology could replace computers: discover 24 stocks that are working to make quantum computing a reality.

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 30 best rare earth metal stocks of the very few that mine this essential strategic resource.

- We've uncovered the 13 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com