- PDF Solutions, Inc. reported past fourth-quarter 2025 revenue of US$62.4 million and a small net loss, while full-year revenue reached US$219.02 million alongside a modest loss, and management projected 2026 revenue growth consistent with its 20% long-term target.

- Brown Capital Management’s decision to add PDF Solutions to its Small Company Fund highlights growing institutional interest in the company’s semiconductor data analytics platform despite its shift from profitability to a small loss in 2025.

- Now we’ll examine how reaffirmed 2026 revenue growth guidance shapes PDF Solutions’ existing investment narrative and risk‑reward profile.

Invest in the nuclear renaissance through our list of 84 elite nuclear energy infrastructure plays powering the global AI revolution.

PDF Solutions Investment Narrative Recap

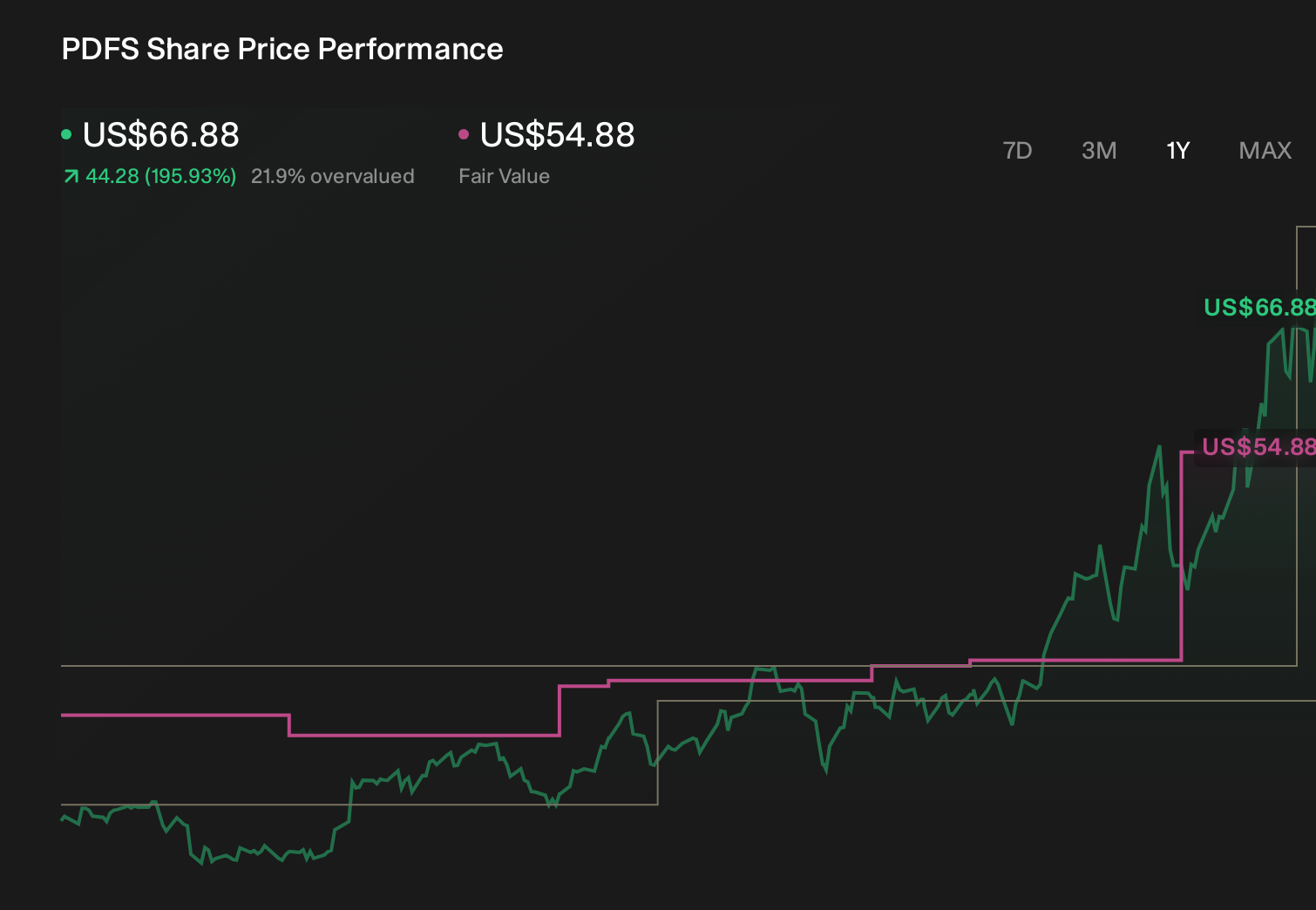

To be a shareholder in PDF Solutions, you need to believe that its semiconductor data analytics platform can translate strong top line growth into durable, software like profitability. The reaffirmed 2026 revenue growth guidance in line with a 20% long term target supports the near term growth catalyst, while the small 2025 net loss keeps execution risk on margins and spending discipline very much in focus.

The most relevant update here is management’s 2026 revenue outlook, which reiterates a growth profile consistent with that 20% long term target despite PDF Solutions posting a modest net loss in 2025. This guidance matters because it underpins the case that rising adoption of Exensio and related platforms can offset risks such as customer concentration and heavy R&D investment, even as the company sits close to breakeven.

But against this solid growth message, investors should still be aware of the risk that sustained spending outpaces demand and...

Read the full narrative on PDF Solutions (it's free!)

PDF Solutions’ narrative projects $330.7 million revenue and $47.9 million earnings by 2028.

Uncover how PDF Solutions' forecasts yield a $36.00 fair value, a 8% upside to its current price.

Exploring Other Perspectives

By contrast, the most cautious analysts framed heavy China exposure and data privacy rules as potential brakes, even while assuming revenue could reach about US$339.3 million and earnings US$45.6 million by 2028, reminding you that views on PDF Solutions can differ sharply and may shift again after this latest update.

Explore 5 other fair value estimates on PDF Solutions - why the stock might be worth as much as 31% more than the current price!

Form Your Own Verdict

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your PDF Solutions research is our analysis highlighting 1 key reward that could impact your investment decision.

- Our free PDF Solutions research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate PDF Solutions' overall financial health at a glance.

Curious About Other Options?

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

- This technology could replace computers: discover 22 stocks that are working to make quantum computing a reality.

- Capitalize on the AI infrastructure supercycle with our selection of the 34 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- The future of work is here. Discover the 33 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com