- In recent months, Vestis has been highlighted for weak long‑term revenue growth of about 1.8% annually, declining earnings that have turned negative over the past three years, and a high net‑debt‑to‑EBITDA ratio of 6 times, together pointing to rising financial strain.

- An interesting angle is that these pressures come despite earlier share price strength, underscoring how concerns about leverage and profitability can quickly refocus attention on balance‑sheet risk.

- Against this backdrop of high leverage, we’ll now examine how these concerns could reshape Vestis’s investment narrative and future risk profile.

Uncover the next big thing with 30 elite penny stocks that balance risk and reward.

Vestis Investment Narrative Recap

To own Vestis, you have to believe its uniform rental and workplace supplies model can eventually convert today’s weak growth, losses, and heavy debt load into steadier cash generation. The recent focus on negative earnings and a 6 times net‑debt‑to‑EBITDA ratio directly affects the key near term catalyst, which is any sign of margin stabilization, and amplifies the main risk right now, which is tighter financial flexibility if performance remains under pressure.

The Q1 2026 results are especially relevant here, with sales slipping to US$663.39 million from US$683.78 million and a net loss of US$6.39 million, alongside management reaffirming guidance for flat to down 2% revenue in fiscal 2026. That combination reinforces concerns about slowing demand and profitability at the same time leverage is elevated, keeping attention firmly on whether operational changes and pricing initiatives can gain traction before the balance sheet comes under more strain.

Yet behind the recent share price move, investors should also be aware of the possibility that high leverage and restrictive debt covenants could...

Read the full narrative on Vestis (it's free!)

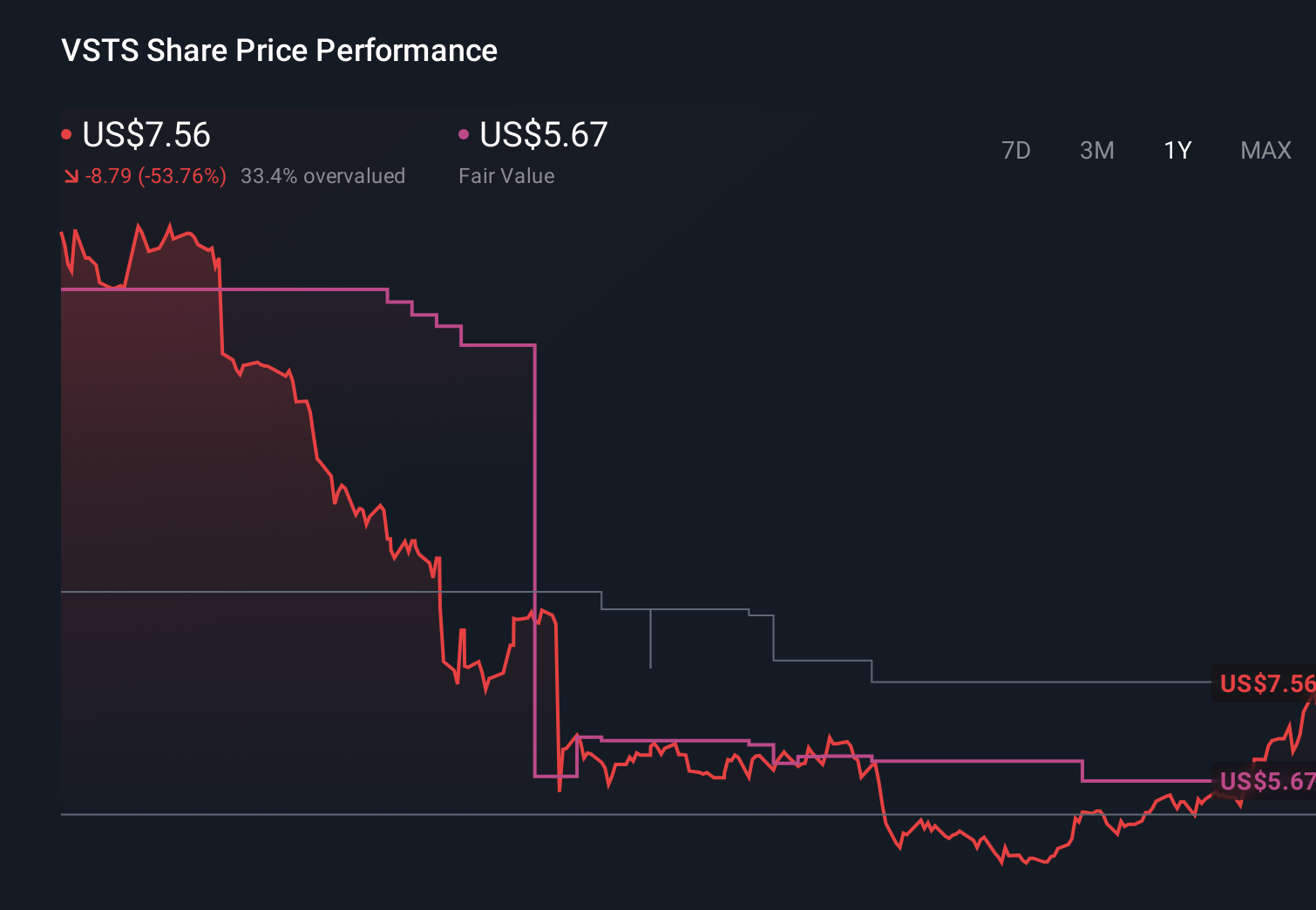

Vestis' narrative projects $2.9 billion revenue and $62.5 million earnings by 2028. This requires 1.9% yearly revenue growth and a $92.5 million earnings increase from $-30.0 million today.

Uncover how Vestis' forecasts yield a $5.67 fair value, a 26% downside to its current price.

Exploring Other Perspectives

Some of the lowest ranked analysts were already cautious, assuming only about 1.2% annual revenue growth and earnings of roughly US$73.2 million by 2028, which is far more pessimistic than the baseline view and could look even harsher in light of recent weak results if you think customer churn and leverage remain a concern.

Explore another fair value estimate on Vestis - why the stock might be worth just $10.00!

The Verdict Is Yours

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Vestis research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Vestis research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Vestis' overall financial health at a glance.

Ready To Venture Into Other Investment Styles?

Our top stock finds are flying under the radar-for now. Get in early:

- Outshine the giants: these 23 early-stage AI stocks could fund your retirement.

- AI is about to change healthcare. These 30 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- The latest GPUs need a type of rare earth metal called Neodymium and there are only 30 companies in the world exploring or producing it. Find the list for free.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com