What triggered fresh attention on Corteva stock?

Corteva (CTVA) has come back into focus after fourth quarter 2025 earnings, where EPS matched expectations but revenue missed forecasts, and management outlined plans to separate its Seed and Crop Chemicals businesses.

See our latest analysis for Corteva.

The share price has been steadily stronger, with a 16.53% 90 day share price return and 14.63% year to date share price return. The 1 year total shareholder return of 24.95% suggests momentum has been building over a longer stretch, even as the planned business separation, recent analyst downgrades and the latest share buyback activity keep attention on execution risks.

If Corteva's reshaping of its business has you thinking about where growth could come from next, it may be worth scanning 24 power grid technology and infrastructure stocks as another way to look at essential infrastructure plays.

With Corteva trading near its analyst price target and showing solid recent returns, the key question now is whether the planned breakup and buybacks leave upside on the table or if the market already reflects the growth story.

Most Popular Narrative: 6.2% Undervalued

With Corteva closing at $77.67 against a narrative fair value estimate of $82.76, the widely followed view is that the shares sit below modeled value, driven by specific assumptions about demand, margins and future earnings.

Advancements in Corteva's innovation pipeline, including premium trait launches (Vorceed, PowerCore), expansion of biological products, and gene editing, enable premium pricing, secure market share, and improve product mix, translating into higher gross margins and earnings growth.

Want to see what is baked into that premium product story? The narrative leans on measured revenue growth, higher profitability, and a richer earnings mix over time. Curious which specific earnings and margin paths pull Corteva toward that $82.76 fair value, and what future multiple is being used to get there? The full narrative lays out those building blocks in detail.

Result: Fair Value of $82.76 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, that upside story can be knocked off course if price pressure in Crop Protection persists, or if tougher regulations and shifts toward organic and non GMO products bite harder.

Find out about the key risks to this Corteva narrative.

Another way to look at Corteva's valuation

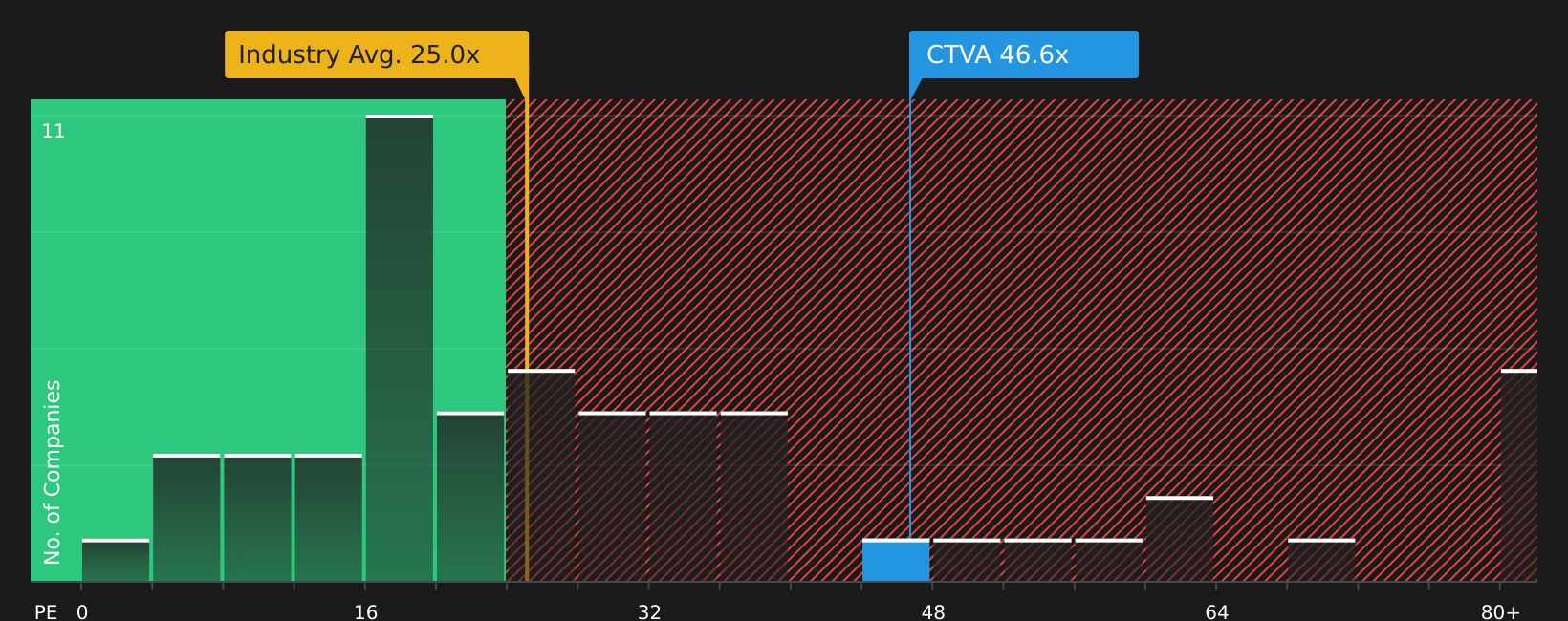

The narrative fair value suggests Corteva is 6.2% undervalued, but the P/E tells a different story. At 43.8x earnings versus a fair ratio of 28.5x, the gap is wide. It also sits above the US Chemicals industry on 25.3x and peers on 20x, which raises the question of how much optimism is already in the price.

See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

All of this leaves a mixed picture, so if you feel torn between the upside story and the concerns, it is worth checking the data yourself and deciding quickly where you stand, starting with 2 key rewards and 1 important warning sign.

Looking for more investment ideas?

If Corteva has sharpened your focus, do not stop here. Use this momentum to refresh your watchlist with a few focused, data backed stock ideas.

- Target value opportunities by scanning 53 high quality undervalued stocks that pair stronger balance sheets and cash flows with prices that sit below their assessed worth.

- Strengthen your income stream by reviewing 15 dividend fortresses with higher yields that still keep an eye on balance sheet support and payout consistency.

- Limit unpleasant surprises by checking 80 resilient stocks with low risk scores that screen for steadier fundamentals, cleaner finances, and fewer red flags in one place.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com