- NPK International Inc. reported past fourth-quarter 2025 results with sales of US$75.2 million and net income of US$14.6 million, alongside full-year sales of US$277.04 million and a move from a US$150.26 million net loss to a US$38.94 million profit.

- The company also issued 2026 revenue guidance of US$305 million to US$325 million and confirmed completion of its share repurchase program, underscoring management’s confidence and capital-return focus.

- We’ll now explore how this stronger profitability and higher 2026 revenue guidance may reshape NPK International’s existing investment narrative.

Find 53 companies with promising cash flow potential yet trading below their fair value.

NPK International Investment Narrative Recap

NPK International’s story today is about whether you believe its rental focused infrastructure platform can translate stronger recent profitability into more durable earnings, despite exposure to project timing and sector cyclicality. The latest results and 2026 revenue guidance support the existing near term catalyst of infrastructure driven demand and rental utilization, while the key risk of revenue volatility from concentrated large projects and less predictable product sales remains largely unchanged by this update.

The completion of NPK’s US$20.29 million share repurchase program, alongside its 2026 revenue guidance of US$305 million to US$325 million, ties directly into the current catalyst of higher rental utilization and expanding infrastructure exposure by reinforcing management’s capital allocation toward the existing equity base. For investors, the combination of improving profitability and capital returns now sits against an unchanged backdrop of project concentration risk and potential swings in customer spending.

Yet behind the stronger 2025 results, investors should be aware of how dependent NPK still is on large infrastructure and utility projects...

Read the full narrative on NPK International (it's free!)

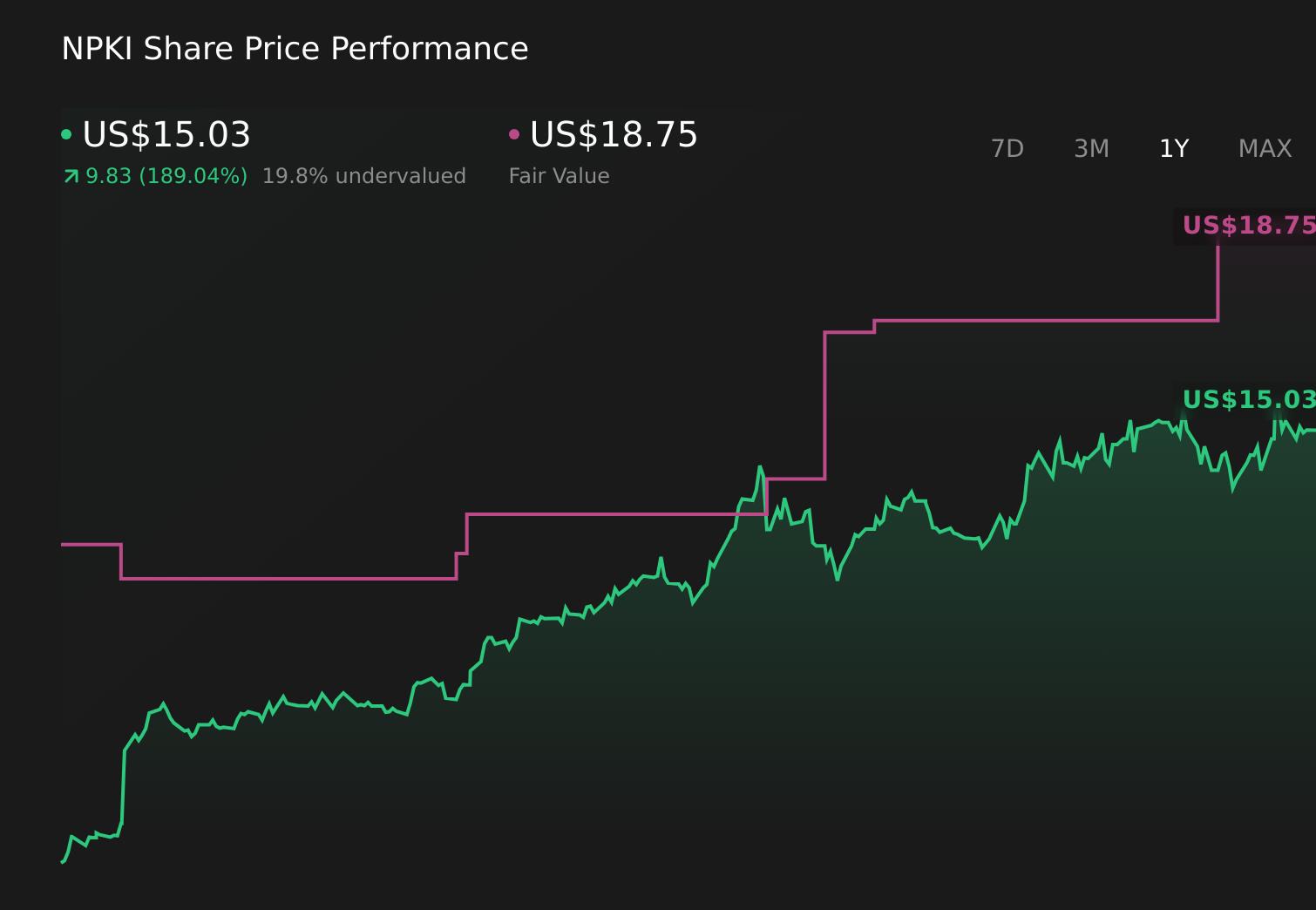

NPK International's narrative projects $329.6 million revenue and $42.8 million earnings by 2028.

Uncover how NPK International's forecasts yield a $16.75 fair value, a 12% upside to its current price.

Exploring Other Perspectives

Two fair value estimates from the Simply Wall St Community span from US$16.75 to US$81,793,883.12, showing how far apart individual views can be. Set against NPK’s reliance on large scale infrastructure projects and rental fleet demand, that gap underlines why you should weigh several independent perspectives when assessing the company’s potential resilience and revenue volatility.

Explore 2 other fair value estimates on NPK International - why the stock might be a potential multi-bagger!

Decide For Yourself

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your NPK International research is our analysis highlighting 5 key rewards that could impact your investment decision.

- Our free NPK International research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate NPK International's overall financial health at a glance.

Searching For A Fresh Perspective?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- Invest in the nuclear renaissance through our list of 84 elite nuclear energy infrastructure plays powering the global AI revolution.

- Uncover the next big thing with 29 elite penny stocks that balance risk and reward.

- We've uncovered the 15 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com