Genesis Energy stock moves and recent return profile

Genesis Energy (GEL) has drawn attention after a recent move in its unit price, prompting investors to take a closer look at how its recent returns line up with the fundamentals disclosed here.

Over the past month, the stock shows a 4.6% return, with about 15.8% over the past 3 months and 13.7% year to date. On a 1 year basis, the total return figure stands at 46.8%, while the 3 year and 5 year total returns are 76.4% and approximately 16x respectively.

See our latest analysis for Genesis Energy.

At a share price of $18.06, Genesis Energy’s recent 7 day share price return of 2.38% and 90 day share price return of 15.84% sit alongside a 1 year total shareholder return of 46.78%. This suggests momentum has been building over both shorter and longer periods as investors reassess future prospects and risks.

If this move in Genesis Energy has you thinking about where else capital might flow in energy infrastructure, it could be worth scanning 23 power grid technology and infrastructure stocks as a starting list of potential ideas.

With GEL trading at $18.06, a value score of 4, an indicated intrinsic discount of 63.76% and a price target of $19.33, you have to ask: is this a genuine mispricing, or is the market already banking on future growth?

Preferred Price-to-Sales Multiple of 1.4x: Is it justified?

On the numbers provided, Genesis Energy is trading on a P/S of 1.4x, while our fair P/S estimate sits lower at 0.9x and the US Oil and Gas peer average is 1.7x.

The P/S ratio compares the company’s market value to its revenue, which can be a useful cross check for a midstream business where earnings are currently negative. In Genesis Energy’s case, the 1.4x P/S sits below the wider industry average, yet above the level our model suggests the market could eventually gravitate toward based on fundamentals.

Put simply, the current P/S implies the market is willing to pay more per dollar of revenue than our fair ratio estimate, but less than for the average peer. With revenue forecast to decline by around 0.6% per year over the next 3 years and the company still reporting a loss of $89.664m on revenue of $1,630.415m, that gap between 1.4x and the 0.9x fair ratio stands out as a key valuation tension investors may want to weigh against the broader sector context.

Explore the SWS fair ratio for Genesis Energy

Result: Price-to-Sales of 1.4x (ABOUT RIGHT)

However, you still have to weigh the ongoing loss of $89.664m on $1,630.415m revenue and the 0.6% annual revenue decline as potential brakes on sentiment.

Find out about the key risks to this Genesis Energy narrative.

Another take on value using our DCF model

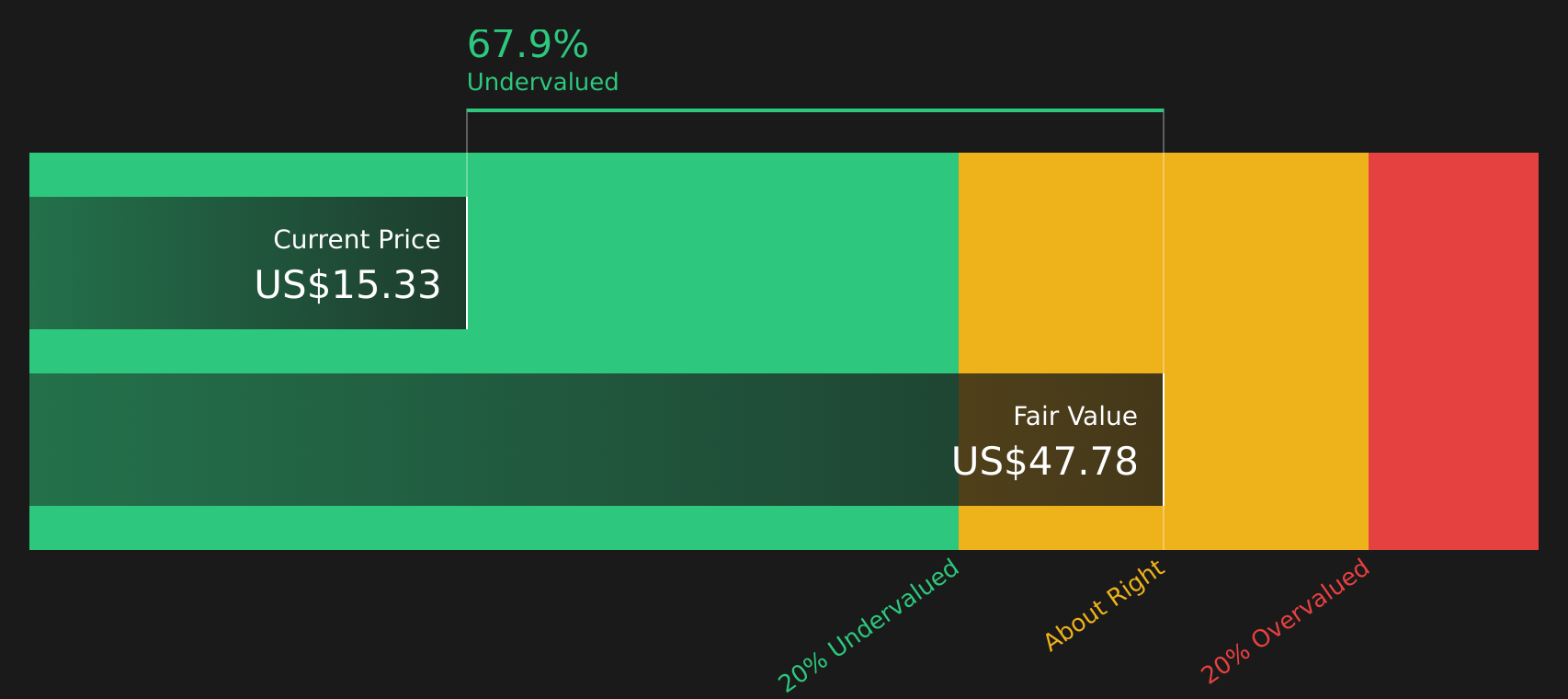

The market might see Genesis Energy as roughly fairly priced on a 1.4x P/S, but our DCF model tells a very different story. On those cash flow assumptions, we arrive at a fair value of $49.83 per unit versus the current $18.06, which implies a very large gap. Is that a genuine opportunity, or is the model leaning too heavily on optimistic inputs?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Genesis Energy for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 46 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

If the mixed signals in Genesis Energy have you on the fence, it may be helpful to act now and stress test the full picture using 2 key rewards and 1 important warning sign.

Looking for more investment ideas?

If Genesis Energy has sharpened your focus, do not stop here. Casting a wider net across quality ideas can help you build a more resilient portfolio.

- Target stronger fundamentals by scanning companies in the solid balance sheet and fundamentals stocks screener (39 results) and see which names pair financial stability with meaningful business momentum.

- Hunt for potential mispricings with our 46 high quality undervalued stocks and compare how these candidates stack up on earnings quality, balance sheets and cash flows.

- Build a steadier income stream by reviewing the 15 dividend fortresses and assess which high yield payers align with your risk tolerance and time horizon.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com