Without a clear single event driving headlines, Stellar Bancorp (STEL) is drawing attention as investors weigh its recent share performance, current valuation signals, and the bank’s underlying earnings and revenue profile.

See our latest analysis for Stellar Bancorp.

At a share price of $37.66, Stellar Bancorp has seen a 22.43% year to date share price return and a 32.00% total shareholder return over the past year, with recent weekly softness tempering the strong 90 day share price momentum of 18.24%.

If this banking story has you thinking about what else is moving, it could be a good moment to broaden your search with our 19 top founder-led companies.

With the share price sitting close to the US$38 analyst target and intrinsic value estimates suggesting a premium, it raises a key question for you: is Stellar Bancorp undervalued today or is the market already pricing in future growth?

Most Popular Narrative: 0.9% Undervalued

With Stellar Bancorp last closing at $37.66 against a narrative fair value of $38.00, the latest storyline leans toward a small valuation cushion built on specific earnings and multiple assumptions.

The share price likely prices in full and timely realization of merger-related synergies from Allegiance and CBTX, with little room for integration setbacks or cost overhang, which could dampen near-term earnings and inflate the expense base if synergies fall short.

Want to see what is sitting behind that merger optimism? The fair value reflects assumptions about measured revenue growth, easing margins, and a richer future earnings multiple. Curious which forecasts make that math work?

Result: Fair Value of $38 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, this storyline could be shaken if digital-first rivals pressure margins faster than expected or if rising compliance and technology costs compress long term profitability.

Find out about the key risks to this Stellar Bancorp narrative.

Another Angle: Earnings Multiple Sends A Different Signal

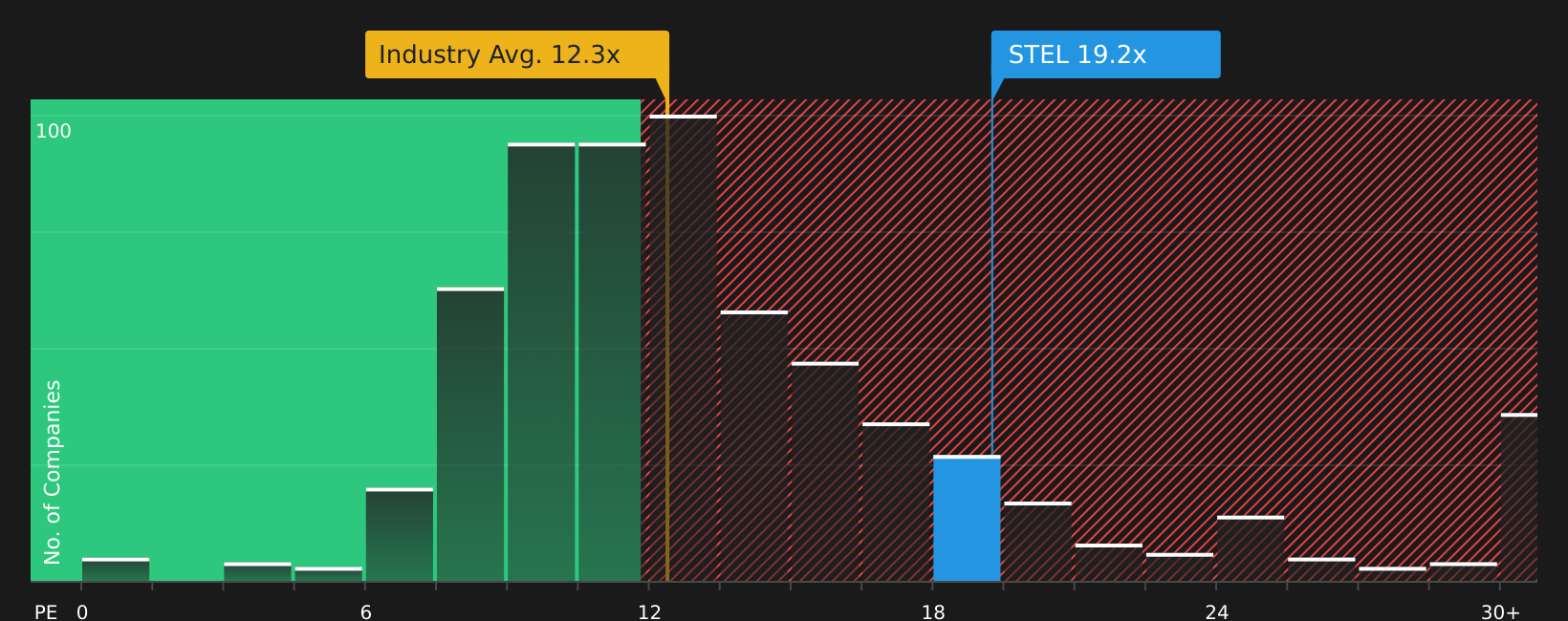

While the narrative fair value pegs Stellar Bancorp at roughly 0.9% undervalued, the current P/E of 18.6x tells a different story. It sits above the US Banks industry at 11.4x, above peer average at 13x, and above a fair ratio of 11.4x, which points to valuation risk if expectations slip.

That gap suggests the share price already bakes in stronger earnings quality or resilience than the averages. The key question for you is simple: do you think Stellar’s future justifies paying that much extra for each dollar of earnings?

See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

If this mix of cautious and optimistic signals feels finely balanced, take a moment to review the numbers yourself and move quickly to shape your own stance; our work highlights 2 key rewards and 1 important warning sign.

Looking for more investment ideas?

If this story has sharpened your view on Stellar Bancorp, do not stop here. Use the same tools to spot other opportunities before they race away from you.

- Target potential value opportunities by scanning our 46 high quality undervalued stocks that pair quality fundamentals with prices that may not fully reflect them.

- Prioritize resilience and sleep better at night by filtering for companies in our 74 resilient stocks with low risk scores with comparatively lower risk scores.

- Hunt for early stage potential by reviewing our 30 elite penny stocks with strong financials featuring smaller names that still meet strict financial criteria.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com