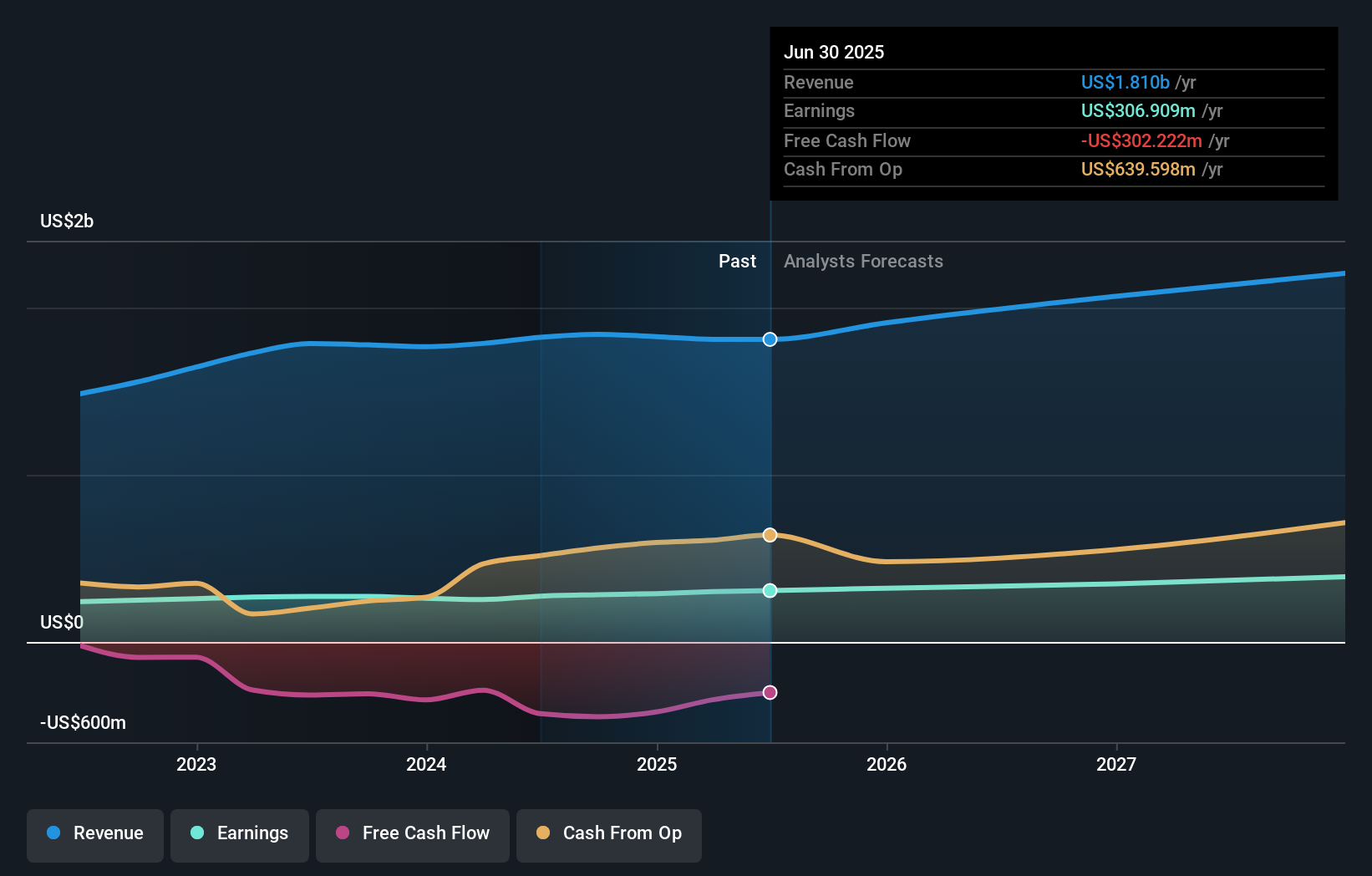

- IDACORP, Inc. recently reported its full-year 2025 results, with sales of US$1.81 billion, revenue of US$1.81 billion, and net income rising to US$323.47 million, alongside higher basic and diluted earnings per share from continuing operations compared with 2024.

- At the same time, the company issued 2026 earnings guidance of US$6.25 to US$6.45 per diluted share, highlighting management’s expectations while signaling limited use of additional tax credits under Idaho’s regulatory mechanism.

- With 2025 earnings per share rising and 2026 guidance set at US$6.25–US$6.45, we’ll examine how this updates IDACORP’s investment narrative.

Capitalize on the AI infrastructure supercycle with our selection of the 34 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

IDACORP Investment Narrative Recap

IDACORP appeals to investors who want exposure to a regulated electric utility with stable earnings and a growing service footprint. The key near term catalyst remains how regulators treat its rising capital needs, while the biggest risk is still regulatory outcomes and cost recovery. The latest 2025 results and 2026 EPS guidance do not materially change that balance, but they do give a clearer reference point for earnings expectations over the next year.

The most relevant update is the new 2026 earnings guidance of US$6.25 to US$6.45 per diluted share, which sits alongside IDACORP’s existing capital and regulatory agenda. Management’s expectation of using less than US$30 million of additional tax credits under Idaho’s regulatory mechanism reinforces how dependent future returns are on regulatory treatment of investment and tax items. Against the backdrop of ongoing capex and rate cases, this guidance frames how much room there might be if regulators tighten terms.

But investors should also be aware that if regulators restrict recovery of rising capital and tax related costs, the pressure on margins and returns could...

Read the full narrative on IDACORP (it's free!)

IDACORP's narrative projects $2.3 billion revenue and $441.8 million earnings by 2028.

Uncover how IDACORP's forecasts yield a $146.22 fair value, in line with its current price.

Exploring Other Perspectives

Four fair value estimates from the Simply Wall St Community span roughly US$112 to US$146 per share, showing how differently retail investors can size up IDACORP. When you set those against the central risk around regulatory approval of large capital programs, it underlines why many investors look at several independent views before deciding how IDACORP might fit into their portfolio.

Explore 4 other fair value estimates on IDACORP - why the stock might be worth as much as $146.22!

Decide For Yourself

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your IDACORP research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

- Our free IDACORP research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate IDACORP's overall financial health at a glance.

Searching For A Fresh Perspective?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- Find 46 companies with promising cash flow potential yet trading below their fair value.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 22 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

- This technology could replace computers: discover 22 stocks that are working to make quantum computing a reality.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com