- In its most recent reported quarter, Vestis (NYSE: VSTS) posted US$663.4 million in revenue, a 3.2% decline year on year, with earnings per share aligning with analyst expectations.

- Management emphasized ongoing execution of a business transformation plan aimed at unlocking operating leverage and improving customer experience, which investors appear to be watching closely as a potential driver of future performance.

- Next, we will examine how Vestis’s focus on its business transformation plan may influence the existing investment narrative for the company.

Invest in the nuclear renaissance through our list of 85 elite nuclear energy infrastructure plays powering the global AI revolution.

Vestis Investment Narrative Recap

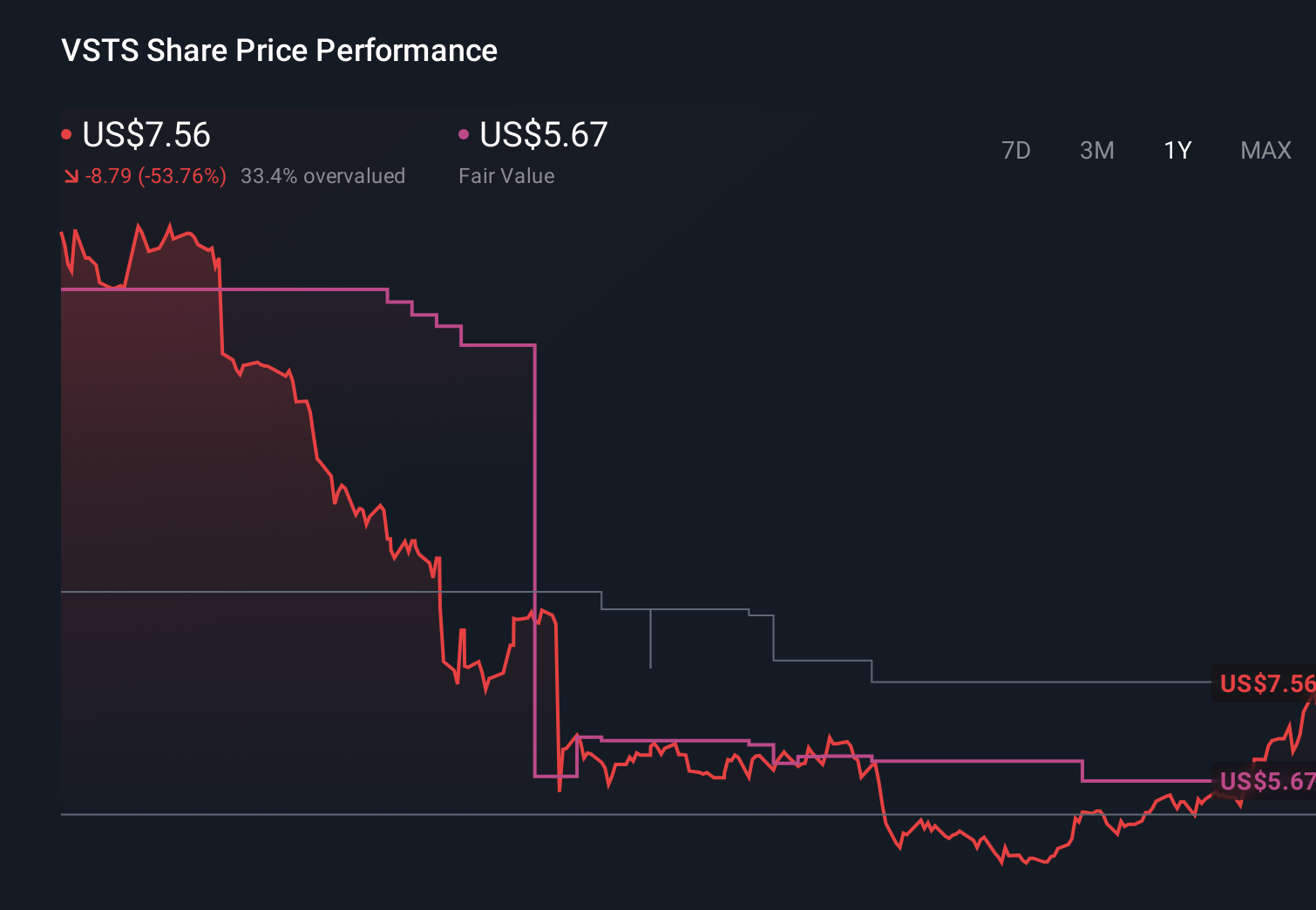

To own Vestis, you need to believe its transformation plan can convert a challenged uniform and facility services business into one with better pricing discipline, more efficient routes, and steadier cash generation. The latest quarter showed revenue down 3.2% to US$663.4 million and another small loss, so it does little to ease near term concerns about customer churn and margin pressure, while leverage and interest coverage remain a key overhang for the story.

The most relevant recent announcement is management’s decision on 10 February 2026 to reaffirm guidance for fiscal 2026 revenue to be flat to down 2%. That stance, despite softer Q1 trends, keeps attention squarely on execution of the business transformation and value based pricing as the main potential catalysts, while also reinforcing that a sustained reversal of revenue decline is still an open question for shareholders.

Yet even with management’s confidence, investors should be aware that Vestis’s elevated debt load and interest coverage constraints could...

Read the full narrative on Vestis (it's free!)

Vestis' narrative projects $2.9 billion revenue and $62.5 million earnings by 2028.

Uncover how Vestis' forecasts yield a $5.67 fair value, a 30% downside to its current price.

Exploring Other Perspectives

Some of the lowest ranked analysts paint a much tougher picture than consensus, assuming only about 1.2% annual revenue growth to roughly US$2.8 billion and modest margin repair, suggesting that if service issues or leverage constraints worsen after this softer quarter, the recovery path could look very different from what you might expect.

Explore another fair value estimate on Vestis - why the stock might be worth just $10.00!

Reach Your Own Conclusion

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Vestis research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Vestis research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Vestis' overall financial health at a glance.

Ready For A Different Approach?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- Explore 22 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- The future of work is here. Discover the 31 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- The latest GPUs need a type of rare earth metal called Terbium and there are only 29 companies in the world exploring or producing it. Find the list for free.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com