- If you are looking at Tronox Holdings and wondering whether the current share price reflects its true worth, the key is to separate short term noise from underlying value.

- The stock is trading at US$6.54 after a 12.6% decline over the last 7 days and a 12.2% decline over the last 30 days, even though the year to date return sits at 53.2% and the 1 year return is a 9.0% loss.

- These swings also sit against a longer backdrop where the 3 year return is a 46.4% loss and the 5 year return is a 59.1% loss, which can affect how the market currently views risk around the stock. That context matters when you are trying to work out whether the recent strength this year is a reset in expectations or just another short term move.

- On Simply Wall St's valuation checks, Tronox Holdings scores 4 out of 6, as shown in this valuation score. Next, we will run through different ways to look at value and then finish with a method that can give you an even clearer read on whether the stock fits your approach.

Find out why Tronox Holdings's -9.0% return over the last year is lagging behind its peers.

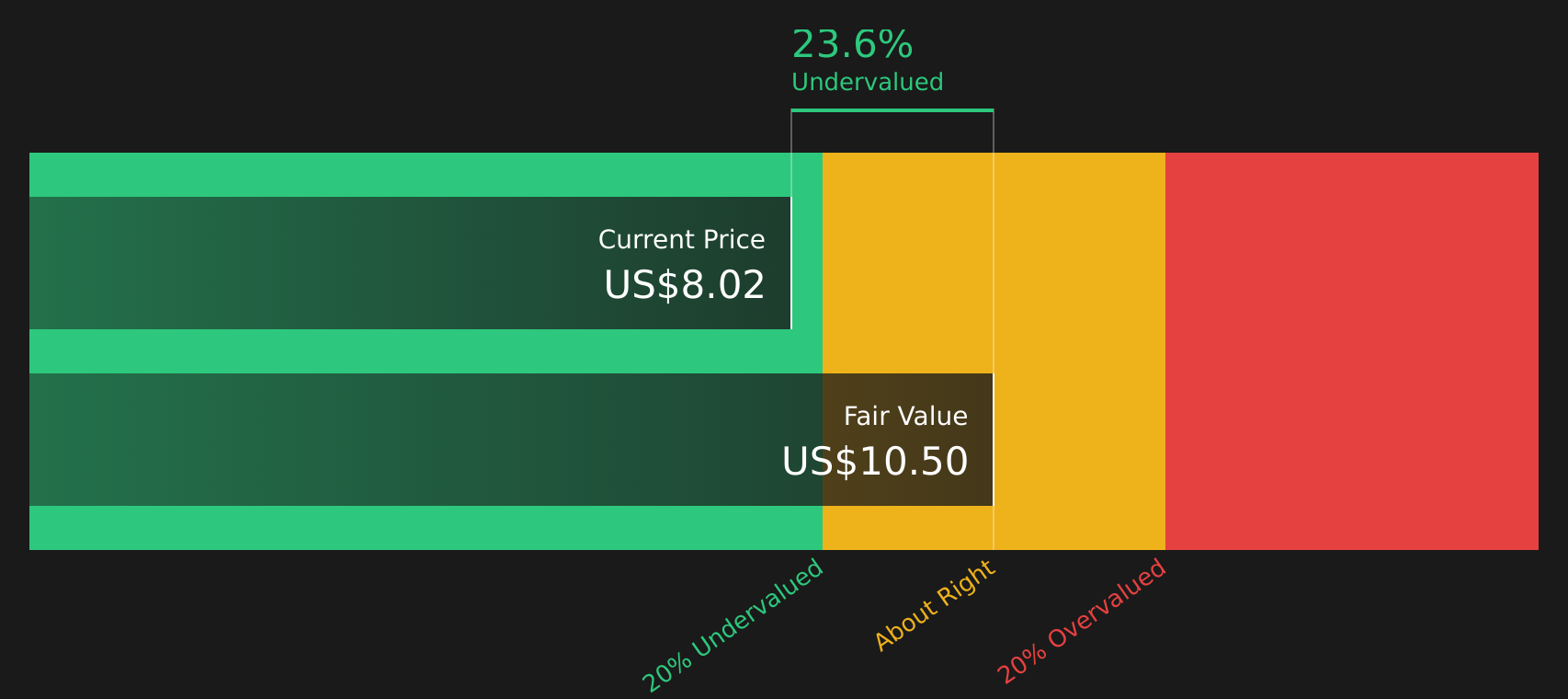

Approach 1: Tronox Holdings Discounted Cash Flow (DCF) Analysis

A DCF model takes estimates of the cash a business could generate in the future, then discounts those cash flows back to today to arrive at an estimate of what the company might be worth now.

For Tronox Holdings, the model used is a 2 Stage Free Cash Flow to Equity approach based on cash flow projections. The latest twelve month free cash flow is a loss of $259.3 million. Analysts and internal estimates suggest free cash flow of $37.5 million in 2026 and $87 million in 2027, rising to $99.5 million in 2028. Beyond that, Simply Wall St extrapolates out to 2035, with discounted annual free cash flows ranging from about $33.4 million to $70.2 million through to mid decade and then into the $47.1 million to $68.5 million range in the later years.

When these projections are discounted back to today, the model arrives at an estimated intrinsic value of about $7.11 per share, compared with the current share price of $6.54. That implies the shares are around 8.0% undervalued, which is a small gap.

Result: ABOUT RIGHT

Tronox Holdings is fairly valued according to our Discounted Cash Flow (DCF), but this can change at a moment's notice. Track the value in your watchlist or portfolio and be alerted on when to act.

Approach 2: Tronox Holdings Price vs Sales

For companies where earnings are weak or volatile, the P/S ratio is often more useful than P/E because it focuses on revenue, which tends to be more stable. Investors usually expect higher P/S multiples when they see stronger growth potential and lower perceived risk, and lower multiples when growth expectations or confidence in the business are more muted.

Tronox Holdings currently trades on a P/S of 0.36x. That sits below the Chemicals industry average P/S of 1.22x and also below the peer group average of 0.41x. On the surface, that suggests the market is assigning a lower sales multiple to Tronox compared with many of its listed peers.

Simply Wall St’s Fair Ratio is a proprietary estimate of what Tronox’s P/S multiple might be, based on factors like its earnings growth profile, profit margins, industry, market cap and company specific risks. This can be more informative than a simple peer or industry comparison because it adjusts for differences in quality, growth outlook and risk. For Tronox, the Fair Ratio is 0.95x, which is above the current 0.36x, indicating the shares are trading below that modelled range.

Result: UNDERVALUED

P/S ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 20 top founder-led companies.

Upgrade Your Decision Making: Choose your Tronox Holdings Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives. These are Simply Wall St Community posts where you and other investors connect a clear story about Tronox Holdings to specific forecasts for revenue, earnings and margins, then link that to a Fair Value that you can weigh against the current share price.

On the Community page, Narratives are easy to use because they show you the assumptions behind a view, how those numbers roll into a Fair Value and how that compares to Price. They also refresh automatically when new data such as earnings, guidance, plant closures or rare earth financing updates are fed into the platform.

For example, one Tronox Holdings Narrative anchors to a higher Fair Value of US$8.00 with revenue growth of about 4.95%, a 5.01% profit margin and a future P/E of 10.82x. A more cautious Narrative works off a Fair Value closer to US$3.50 with revenue growth of about 2.85%, a 9.68% profit margin and a future P/E of 2.66x. This shows you how different stories about the same company can lead to very different decisions on whether the current price looks attractive or stretched.

For Tronox Holdings, here are previews of two leading Tronox Holdings Narratives that make it easier to explore different perspectives:

Fair Value: US$8.00

Gap to Fair Value: about 18.3% below this Narrative fair value based on the current US$6.54 share price

Revenue Growth Assumption: 4.95% a year

- Supports a higher fair value based on the view that cost savings, plant closures and rare earth financing contribute to stronger margins and cash flows over time.

- Assumes earnings recover to US$121.1 million by around 2028, with Tronox trading on a future P/E of 10.82x, below the current US Chemicals industry P/E assumption that analysts are using.

- Highlights risks related to debt, environmental regulation, competition from low cost producers and potential shifts away from traditional TiO₂, and asks you to consider whether the US$8.00 fair value is realistic in light of those factors.

Fair Value: US$6.11

Gap to Fair Value: about 7.0% above this Narrative fair value based on the current US$6.54 share price

Revenue Growth Assumption: 3.99% a year

- Presents Tronox as closer to fairly priced, with a consensus fair value of about US$6.11 based on moderate revenue growth, modest margin improvement and a future P/E of 3.88x.

- Notes potential benefits from cost programs, capacity reductions and growth areas such as India and rare earth side streams, while also applying a higher discount rate and a more conservative earnings path to US$45.2 million by around 2028.

- Emphasizes ongoing headwinds from regulation, overcapacity, leverage of about US$2.9b net debt and reliance on TiO₂, which could limit upside if demand or pricing do not develop in line with analyst expectations.

If you want to explore either perspective in more detail and see every assumption behind the numbers, you can start with these two previews, then move through to the full Community Narratives for Tronox, compare the fair values and decide which story, if any, aligns with your own expectations.

Curious how numbers become stories that shape markets? Explore Community Narratives

Do you think there's more to the story for Tronox Holdings? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com