- In late February 2026, First Advantage Corporation reported fourth-quarter 2025 results showing revenue of US$420.02 million and a return to quarterly profitability, alongside full-year 2025 revenue of US$1.57 billion and a reduced annual net loss of US$34.82 million.

- On the same day, the company unveiled a new US$100 million open-ended share repurchase program funded from existing cash and issued 2026 revenue guidance of US$1.63 billion to US$1.70 billion, underscoring management’s confidence in its balance sheet and future business activity.

- Now, we’ll examine how First Advantage’s return to quarterly profitability and launch of a US$100 million buyback shape its investment narrative.

Invest in the nuclear renaissance through our list of 85 elite nuclear energy infrastructure plays powering the global AI revolution.

First Advantage Investment Narrative Recap

To own First Advantage, you need to believe that demand for compliance-focused background screening and identity services can offset hiring softness and intense competition. The immediate catalyst is whether recent revenue momentum and a return to quarterly profitability can be sustained; the key risk is that hiring volumes weaken again, pressuring growth and margins. The latest results and buyback do not remove this risk, but they do slightly strengthen the near term story around execution and capital discipline.

The new US$100 million open-ended share repurchase program is the announcement that most directly reinforces this narrative. It adds to First Advantage’s history of buybacks and signals that management is comfortable allocating existing cash to reduce the share count while still funding operations and integration work. For investors focused on upcoming earnings and margin progression, the buyback sits alongside 2026 revenue guidance as another reference point for how management is positioning around current catalysts.

Yet alongside the return to profitability, investors should still be aware of how persistent hiring hesitancy could...

Read the full narrative on First Advantage (it's free!)

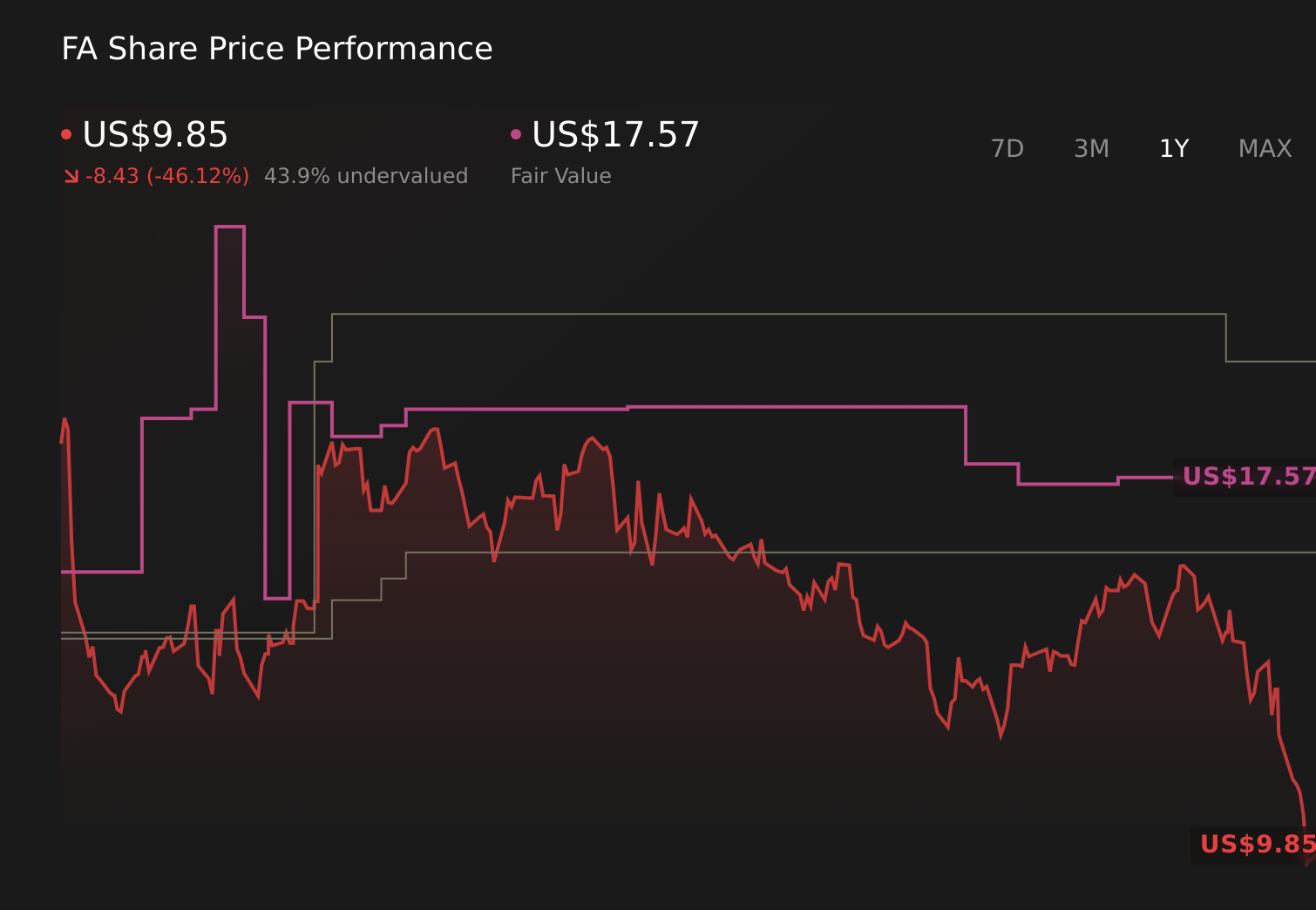

First Advantage's narrative projects $1.9 billion revenue and $143.4 million earnings by 2028.

Uncover how First Advantage's forecasts yield a $17.57 fair value, a 46% upside to its current price.

Exploring Other Perspectives

Compared with the consensus view, the most optimistic analysts were already assuming revenue could reach about US$1.7 billion and earnings about US$95 million, so this new profitability milestone and buyback may either support that upbeat thesis or prompt a rethink if privacy and data access risks start to bite more than expected.

Explore another fair value estimate on First Advantage - why the stock might be worth just $17.57!

The Verdict Is Yours

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your First Advantage research is our analysis highlighting 3 key rewards that could impact your investment decision.

- Our free First Advantage research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate First Advantage's overall financial health at a glance.

Interested In Other Possibilities?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- Find 50 companies with promising cash flow potential yet trading below their fair value.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 20 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

- Uncover the next big thing with 30 elite penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com