Genesis Energy (GEL) has pulled investor focus after a series of refinancing moves, including a US$750 million senior notes issue due 2034 and a tender offer for its outstanding 7.75% notes due 2028.

See our latest analysis for Genesis Energy.

The refinancing push and recent conference appearance come after a period of solid momentum, with a 90 day share price return of 12.29% and a 1 year total shareholder return of 43.56%. This suggests investors are reassessing both growth prospects and balance sheet risk.

If Genesis Energy’s refinancing story has your attention, this could be a good moment to broaden your energy watchlist and check out 24 power grid technology and infrastructure stocks as another set of infrastructure driven opportunities.

With the units up strongly over 1 year and trading about 7% below the consensus price target, as well as at an implied discount to some intrinsic estimates, you have to ask: is Genesis Energy still mispriced, or is the market already banking on future growth?

Preferred Price-to-Sales of 1.4x: Is it justified?

On paper, Genesis Energy screens as good value against both its industry and peer group on P/S, yet it screens as expensive versus its own fair ratio estimate.

The preferred multiple here is the P/S ratio of 1.4x. For a midstream and infrastructure focused operator with $1,630.4m of revenue and a loss of $89.7m, investors often look at revenue based metrics when earnings are negative or volatile, so P/S can be a useful benchmark.

Compared with the wider US Oil and Gas industry average P/S of 1.8x and a peer average of 2.3x, Genesis Energy’s 1.4x stands at a clear discount. This suggests the market is assigning a lower value to each dollar of revenue than it does to many comparable names. However, against an estimated fair P/S ratio of 0.9x, the current 1.4x is materially higher. This hints at a level the market could move towards if sentiment or expectations were to cool.

Explore the SWS fair ratio for Genesis Energy

Result: Price-to-Sales of 1.4x (ABOUT RIGHT)

However, you still have to weigh the annual revenue contraction of 0.64% and the loss of US$89.7m, which could keep pressure on sentiment if refinancing benefits take time to show.

Find out about the key risks to this Genesis Energy narrative.

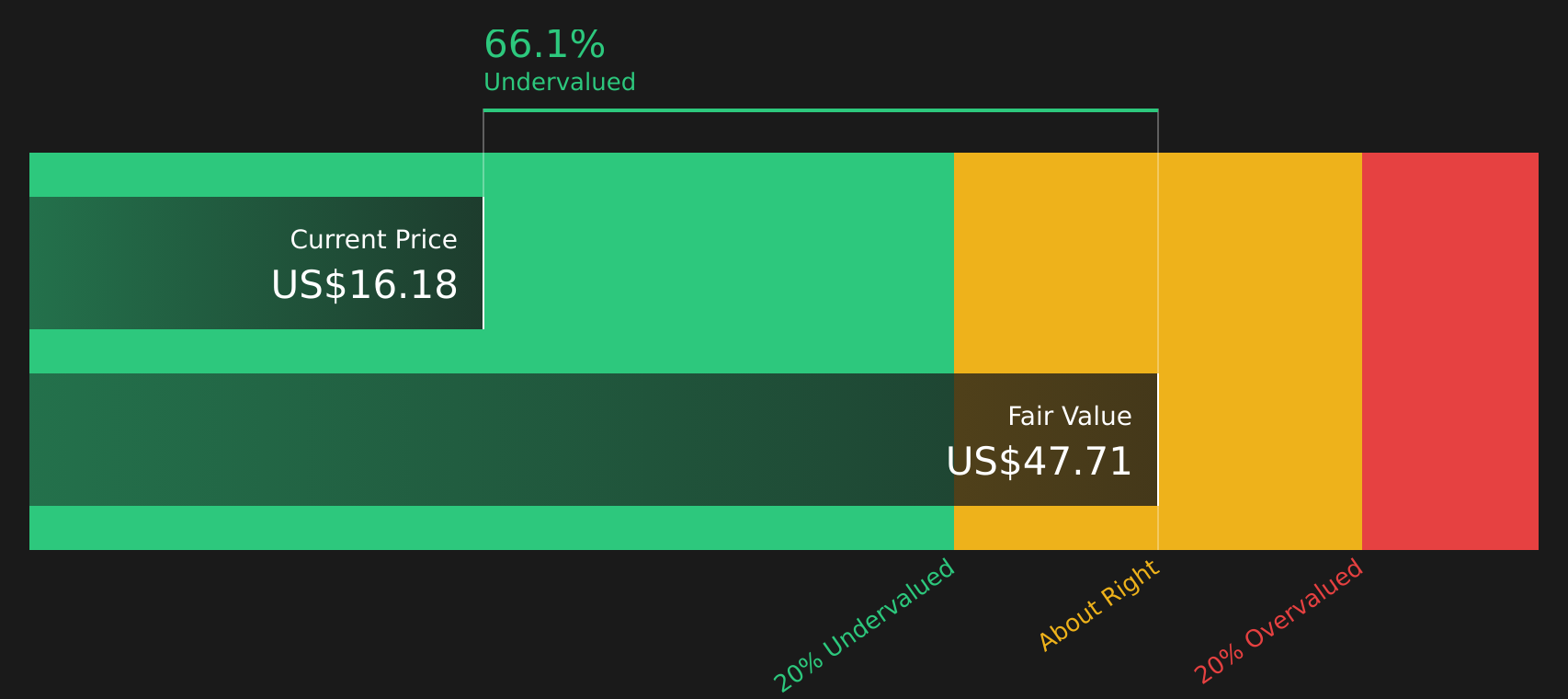

Another View: DCF Points to Deeper Upside

While the current P/S of 1.4x felt roughly in the right zone, our DCF model comes back with a very different message and puts fair value at $50.96 versus the current $18.09. That gap is wide, so is the market being too cautious about future cash flows?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Genesis Energy for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 50 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

Does this mix of caution and optimism match how you see Genesis Energy right now, or are you reading it differently? The full picture includes both the potential upsides and the issues on investors’ minds, so it is worth scanning the data and deciding where you stand with 2 key rewards and 1 important warning sign.

Looking for more investment ideas?

Before you move on, take a moment to line up your next ideas so you are not relying on a single story to shape your portfolio.

- Target potential mispricing by scanning companies that look like 50 high quality undervalued stocks based on strong fundamentals and more conservative assumptions.

- Build a steadier income base by reviewing our list of 16 dividend fortresses, focused on businesses offering higher yields with supporting data.

- Prioritise resilience by checking stocks in the 63 resilient stocks with low risk scores that pair lower risk scores with clear financial information you can scrutinise quickly.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com