Why Corteva is on investors’ radar today

Corteva (CTVA) is drawing fresh attention after recent share price moves, including a small gain over the past day and a negative return over the past week. This is prompting investors to reassess the agriculture company’s fundamentals.

See our latest analysis for Corteva.

Zooming out, Corteva’s recent 1-day share price gain and 7-day share price pullback sit against a stronger backdrop, with a 90-day share price return of 16.61% and a 1-year total shareholder return of 28.33%. This pattern suggests momentum has been building over time.

If this agriculture name has your attention, it can also be a good moment to broaden your watchlist. You can use our screener of 28 elite gold producer stocks as another way to look at resource related opportunities.

With Corteva trading at $76.96, a company reported intrinsic value that sits above the current price and a modest discount to the average analyst target, you have to ask: is this an opening, or is the market already pricing in future growth?

Most Popular Narrative: 7% Undervalued

Compared to Corteva’s last close at $76.96, the most followed narrative points to a fair value of $82.76, putting a modest valuation gap in focus.

Advancements in Corteva's innovation pipeline, including premium trait launches (Vorceed, PowerCore), expansion of biological products, and gene editing, enable premium pricing, secure market share, and improve product mix, translating into higher gross margins and earnings growth.

Want to see what is baked into that $82.76 figure? Revenue stepping up, margins rebuilding, and a richer earnings multiple all sit at the core of this narrative.

Result: Fair Value of $82.76 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, the story can shift quickly if ongoing price pressure in Crop Protection persists or if currency swings in key markets continue to affect reported results.

Find out about the key risks to this Corteva narrative.

Another View: Earnings Multiple Sends a Different Signal

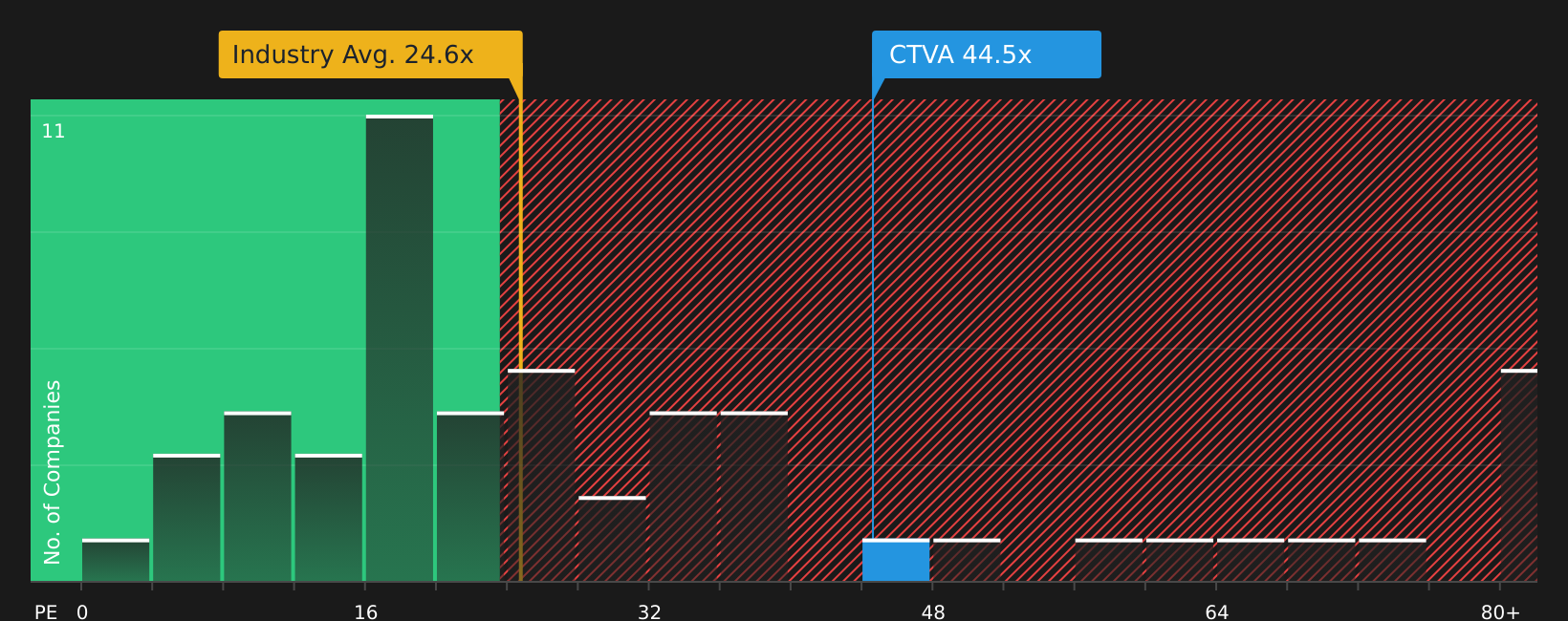

The fair value narrative at $82.76 paints Corteva as modestly undervalued, but the current P/E of 43.4x tells a tougher story. That is far above the US Chemicals industry at 23.3x, the peer average at 19.7x, and an estimated fair ratio of 27.9x. This combination points to meaningful valuation risk if sentiment cools.

Put simply, the share price already carries a premium that sits well above both peers and the fair ratio the market could move toward over time. As an investor, you need to decide whether the earnings profile justifies paying that kind of multiple.

See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

If this mix of optimism and concern feels familiar, do not sit on the fence. Review the full picture for yourself, including 2 key rewards and 1 important warning sign.

Looking for more investment ideas?

If Corteva has sharpened your focus, do not stop there. A few minutes with the right screeners can surface opportunities you would not want to miss.

- Target potential mispricings by checking our list of 50 high quality undervalued stocks that may offer a more attractive entry point right now.

- Prioritise resilience first and see which companies clear the bar in our 63 resilient stocks with low risk scores before you commit fresh capital.

- Hunt for tomorrow’s potential standouts by scanning the screener containing 24 high quality undiscovered gems that most investors might not be watching yet.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com