- NPK International Inc. recently reported its fourth-quarter and full-year 2025 results, with Q4 sales rising to US$75.2 million and full-year net income improving to US$38.94 million, and issued full-year 2026 revenue guidance of US$305 million to US$325 million.

- The completion of a US$20.29 million share repurchase program alongside this earnings turnaround highlights management’s focus on capital returns and balance sheet discipline.

- Now we’ll consider how this earnings improvement and 2026 revenue guidance might influence NPK International’s existing investment narrative.

Capitalize on the AI infrastructure supercycle with our selection of the 35 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

NPK International Investment Narrative Recap

NPK International’s story still centers on benefiting from long-duration infrastructure and utility projects, with rental demand and fleet utilization as key short term catalysts. The latest US$277.0 million in 2025 sales and US$305 million to US$325 million 2026 revenue guidance support that rental and product demand remain intact, while also highlighting execution risk around project timing and sector cyclicality. For now, this earnings improvement does not materially change the company’s biggest risk, which remains revenue volatility if large projects slow or are delayed.

The most relevant update here is NPK’s full year 2026 revenue guidance of US$305 million to US$325 million, coming on the back of a swing from a US$150.3 million loss in 2024 to US$38.9 million in net income for 2025. That guidance helps frame how management currently sees demand for infrastructure related rentals and products holding up relative to the existing multi year catalyst of robust utility and pipeline spending, even as investors weigh the timing and durability of those underlying projects.

Yet despite the stronger 2025 results, investors still need to consider how exposed NPK remains to large project delays and shifting infrastructure priorities...

Read the full narrative on NPK International (it's free!)

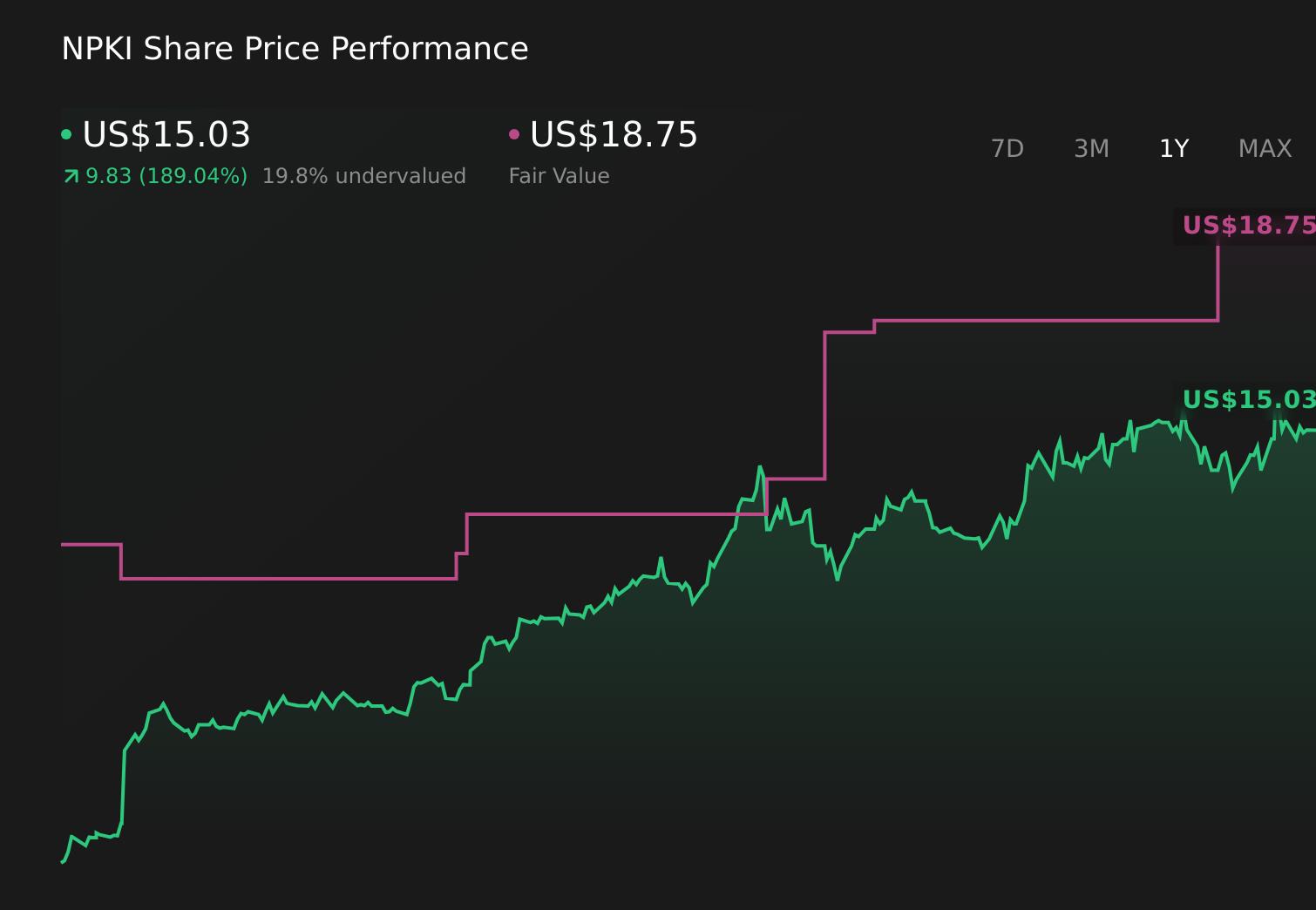

NPK International’s narrative projects $329.6 million revenue and $42.8 million earnings by 2028. This requires 12.0% yearly revenue growth and a modest $0.7 million earnings increase from $42.1 million today.

Uncover how NPK International's forecasts yield a $18.75 fair value, a 38% upside to its current price.

Exploring Other Perspectives

Two Simply Wall St Community fair value estimates span from US$6.02 to US$18.75 per share, underlining how far apart individual views can be. Against that backdrop, the latest 2026 revenue guidance and recent earnings recovery give you more concrete numbers to compare with those expectations and to weigh against the risk of infrastructure project timing swings affecting future performance.

Explore 2 other fair value estimates on NPK International - why the stock might be worth as much as 38% more than the current price!

Form Your Own Verdict

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your NPK International research is our analysis highlighting 3 key rewards that could impact your investment decision.

- Our free NPK International research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate NPK International's overall financial health at a glance.

No Opportunity In NPK International?

Our top stock finds are flying under the radar-for now. Get in early:

- The latest GPUs need a type of rare earth metal called Terbium and there are only 29 companies in the world exploring or producing it. Find the list for free.

- This technology could replace computers: discover 22 stocks that are working to make quantum computing a reality.

- We've uncovered the 16 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com