Event context and recent share performance

Enterprise Financial Services (EFSC) has drawn investor attention after recent trading, with the stock down about 1% over the past day, 6% over the past week, and roughly 10% over the past month.

Those shorter term moves contrast with a small positive total return over the past year, as well as higher three and five year total returns. This has prompted some investors to reassess how the bank’s current pricing lines up with its fundamentals.

See our latest analysis for Enterprise Financial Services.

With the share price at $54.03, the recent 1 month and 7 day share price declines contrast with a positive 1 year total shareholder return, suggesting weaker short term momentum alongside a still positive longer term outcome.

If EFSC’s recent pullback has you looking beyond regional banks, this could be a good moment to scan 20 top founder-led companies as potential next ideas on your list.

EFSC now trades at $54.03, with recent declines sitting alongside a 1 year total return of about 1% and a value score of 6. Is this pullback a genuine opening, or is the market already pricing in future growth?

Preferred P/E of 10.1x: Is it justified?

On a P/E of 10.1x at a share price of $54.03, Enterprise Financial Services is being valued below both its peer average and the wider US Banks industry. This points to the market assigning a lower earnings multiple than many of its closest comparables.

The P/E ratio compares the current share price to earnings per share. For a bank like EFSC it is a quick way to see how much investors are paying for each dollar of profit. With EFSC trading at 10.1x earnings while its peer average sits at 14.4x, the current pricing suggests investors are paying a lower premium for those earnings than they are for similar banks.

EFSC is also trading below the US Banks industry average P/E of 11.3x, so the discount is not just relative to a small peer set. In addition, our analysis indicates that a fair P/E for EFSC, based on the SWS fair ratio work, is closer to 11x. This is above where the shares trade today and could be a level the market moves toward if sentiment aligns more closely with that benchmark. Result: Price-to-Earnings of 10.1x (UNDERVALUED)

Explore the SWS fair ratio for Enterprise Financial Services

However, you still need to weigh risks such as continued weak share price momentum and any shift in market sentiment if EFSC’s lower P/E is viewed as justified.

Find out about the key risks to this Enterprise Financial Services narrative.

Another view: DCF paints a very different picture

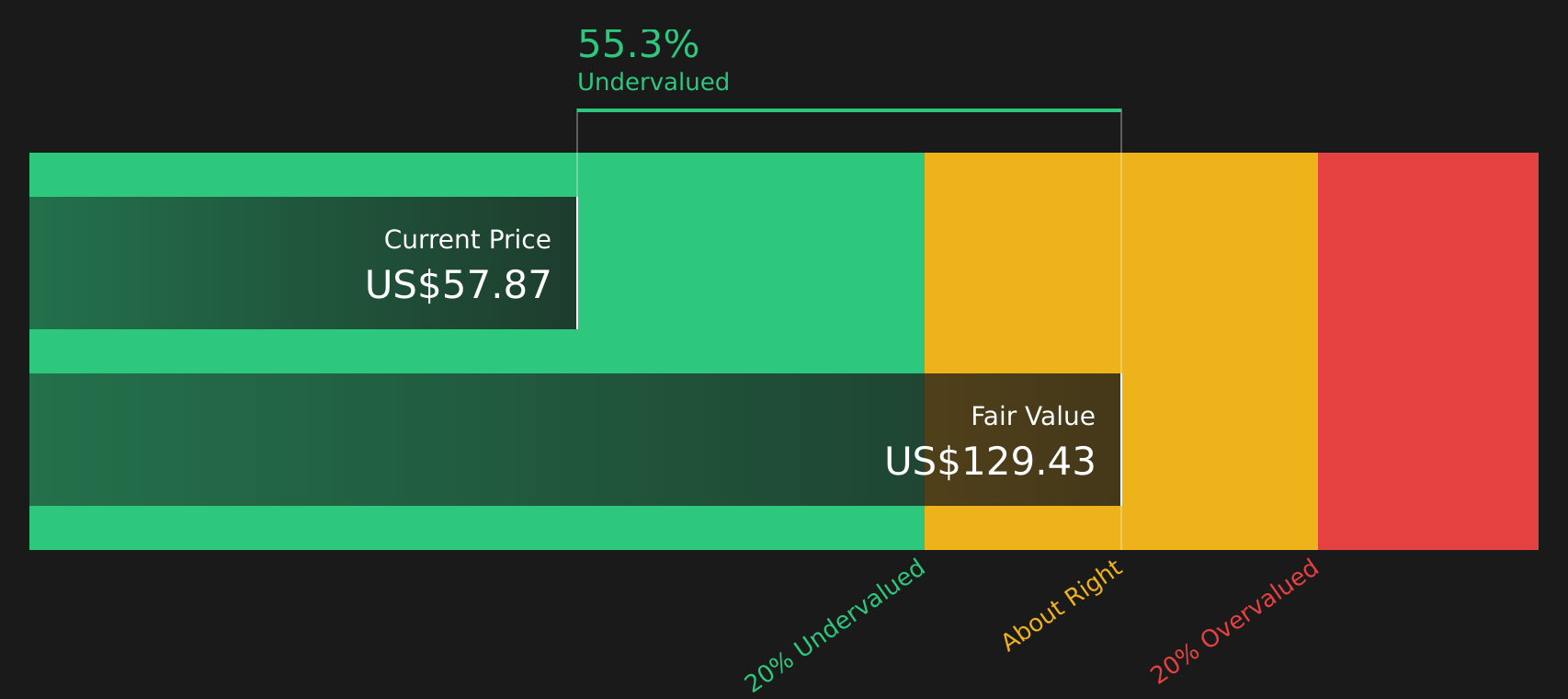

While the current 10.1x P/E suggests EFSC looks inexpensive next to peers and the US Banks industry, our DCF model tells a stronger story. On that basis, the shares at $54.03 sit around 50.8% below an estimated future cash flow value of $109.81, which also screens as undervalued.

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Enterprise Financial Services for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 46 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

Curious whether the tone of this analysis fits how you see EFSC right now? Take a closer look at the underlying data and form your own view quickly, then weigh it against the 6 key rewards to see what optimism in the market is focusing on.

Looking for more investment ideas?

If EFSC is just one piece of your watchlist, do not stop here. Use the tools available to surface other stocks that fit your own style and priorities.

- Target potential value opportunities by scanning our list of 46 high quality undervalued stocks that combine pricing and fundamentals in a way that might appeal to long term investors.

- Prioritise resilience first and check out 63 resilient stocks with low risk scores, highlighting companies that score well on stability so you can focus your deeper research where it counts.

- Hunt for lesser known names by reviewing a screener containing 23 high quality undiscovered gems that could broaden your opportunity set beyond the usual tickers on your radar.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com