A Look At Carrier Global (CARR) Valuation After New Data Center Chiller Launch

Carrier Global (CARR) is back in focus after introducing the AquaEdge 30CF air cooled centrifugal chiller, a data center focused system aimed at maintaining cooling performance and uptime under demanding real world conditions.

See our latest analysis for Carrier Global.

At a share price of US$58.43, Carrier Global has seen pressure in the near term, with a 7 day share price return of a 4.48% decline and a 30 day share price return of an 8.59% decline. A 90 day share price return of 9.42% and a 3 year total shareholder return of 33.19% point to momentum that has played out more over the medium term than in the past few weeks, as investors weigh data center focused launches like AquaEdge 30CF against longer running expectations.

If this data center focused move has you thinking about the broader infrastructure theme, you might also want to see our screener of 24 power grid technology and infrastructure stocks as another way to source ideas.

With Carrier trading at US$58.43 and references to both an intrinsic discount and a gap to analyst targets, the key question is whether recent weakness sets up a value entry or if the market already reflects future growth.

Most Popular Narrative: 18.6% Undervalued

At $58.43 against a most followed fair value estimate of $71.80, the current price sits well below what that narrative considers reasonable based on its cash flow and earnings path.

Carrier's introduction of differentiated products, such as air cooled commercial heat pumps and the integration of HEMS technology with Google Cloud's AI, positions them to capture the growing demand for sustainable and smart energy solutions, potentially driving future revenue growth.

The company's strong performance in the aftermarket space, with double digit growth and increased attachment rates on chillers, is expected to bolster net margins through high margin service offerings and customer retention.

Want to see what kind of revenue growth, margin lift and valuation multiple this story leans on, all filtered through an 8.9% discount rate? The full narrative lays out the numbers that connect those assumptions to that $71.80 fair value.

Result: Fair Value of $71.80 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, there is still room for this story to break the other way if weaker performance in certain regions and lingering tariff exposure begin to affect earnings.

Find out about the key risks to this Carrier Global narrative.

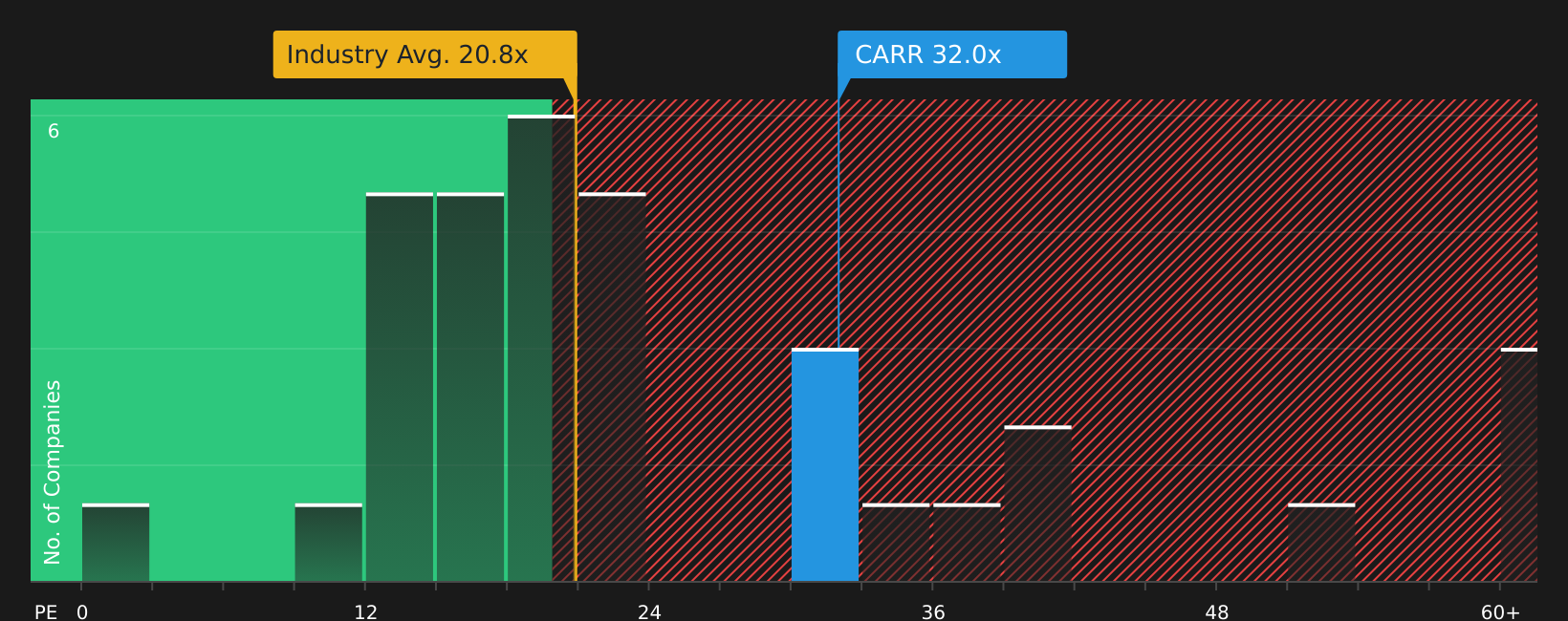

Another Angle: What The P/E Is Telling You

So far, the story leans on cash flows and fair value, but the current P/E ratio of 33.6x paints a different picture. It is higher than both the US Building industry at 21.2x and peer average at 29.2x, even though the fair ratio sits at 40x.

That gap suggests the market is already paying up for Carrier Global compared to its sector, while still leaving room if sentiment ever drifted closer to that 40x fair ratio. The real question is whether you see that premium as risk or as room for the story to grow into.

See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

If this combination of potential benefits and risks seems finely balanced, you may want to review the underlying data yourself and decide on your own view, beginning with 4 key rewards and 1 important warning sign.

Looking for more investment ideas?

If you are weighing your next move, do not stop at a single stock story. Broaden your watchlist with ideas that fit your own style and risk comfort.

- Target potential mispricings by scanning for quality names trading below their implied value with our 48 high quality undervalued stocks.

- Strengthen the income side of your portfolio by focusing on reliable payouts through our 14 dividend fortresses.

- Prioritise financial resilience by filtering for companies with robust balance sheets using the solid balance sheet and fundamentals stocks screener (41 results).

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com