Babcock & Wilcox Enterprises (BW) just paired a profitable fourth quarter with a newly amended credit agreement, combining improved earnings with added borrowing capacity and extended debt maturities that could matter for investors watching its turnaround story.

See our latest analysis for Babcock & Wilcox Enterprises.

The turnaround signs appear to have caught the market’s attention, with a 1-day share price return of 5.13% and a 90-day share price return of 137.30% feeding into a very large 1-year total shareholder return. This suggests that momentum has picked up sharply compared with recent years.

If this kind of recovery story interests you, it might be worth broadening your search with our screener featuring 23 power grid technology and infrastructure stocks, where you can find other infrastructure names linked to the energy transition.

With BW trading close to its analyst price target but showing a large intrinsic discount estimate, you now have to decide whether this turnaround is still underappreciated or whether the market is already pricing in future growth.

Most Popular Narrative: 77.1% Overvalued

At a last close of $14.76 versus a narrative fair value of $8.33, Babcock & Wilcox Enterprises is framed as richly priced, with that gap hinging on how future growth and margins play out.

The company is tying a large part of its long term story to AI data center power demand, including a US$1.5b Applied Digital project and a US$3b to US$5b AI opportunity pipeline. If AI related electricity needs or data center build outs slow or are met by alternative technologies, the expected uplift in backlog conversion and revenue may not materialize, which could pressure earnings and compress margins.

Curious how a story built on AI driven power demand, rising margins and future earnings translates into that fair value gap? The narrative leans on specific revenue, profit and valuation assumptions that are anything but simple headline numbers.

Result: Fair Value of $8.33 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, this story still leans heavily on AI driven data center demand and the smooth execution of large, multi year projects, where delays or cost overruns could quickly change the picture.

Find out about the key risks to this Babcock & Wilcox Enterprises narrative.

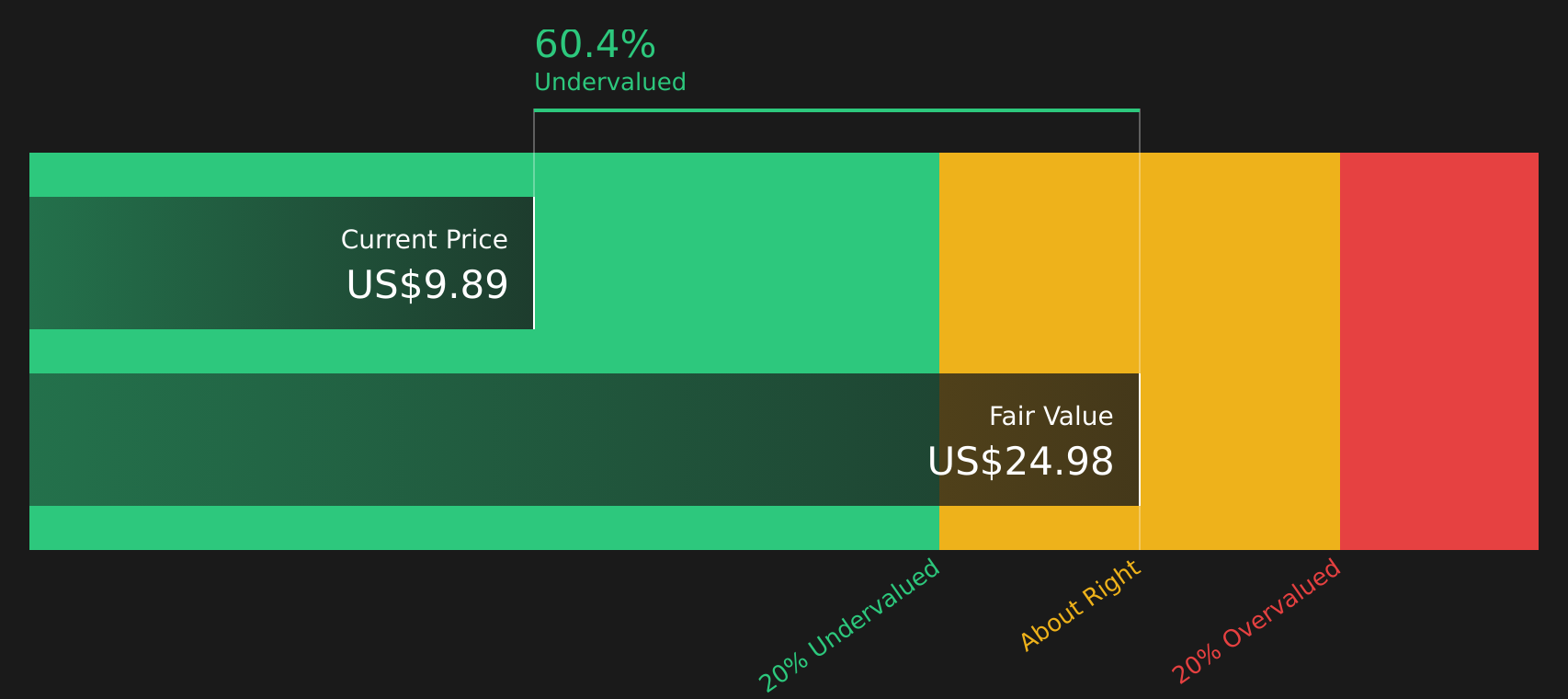

Another View: Cash Flows Tell a Different Story

While the narrative fair value of $8.33 points to a stretched price, our DCF model presents a contrasting view, with an estimated future cash flow value of $28.94 per share. That gap suggests the real question is whether earnings or cash flow assumptions feel more realistic to you.

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Babcock & Wilcox Enterprises for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 50 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

If this mix of upside potential and clear risk flags leaves you uncertain, take a closer look at the numbers yourself and move quickly to frame your own stance, starting with 2 key rewards and 3 important warning signs.

Ready for more investment ideas?

If BW has sharpened your appetite for opportunity, do not stop here; broaden your watchlist with focused stock ideas that match the way you like to invest.

- Target quality at a discount by checking stocks our screener tags as 50 high quality undervalued stocks, so you can focus on names where price and fundamentals may be out of sync.

- Secure your income stream by scanning companies in our 14 dividend fortresses, built for investors who care about sizeable yields backed by real businesses.

- Sleep a bit easier by reviewing companies highlighted in our 67 resilient stocks with low risk scores, where business stability and risk scores take center stage before anything else.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com