InnovAge Holding (INNV) has just been upgraded to a higher Zacks rank, supported by rising earnings estimate revisions and a hammer chart pattern that points to improving sentiment and renewed attention on the stock.

See our latest analysis for InnovAge Holding.

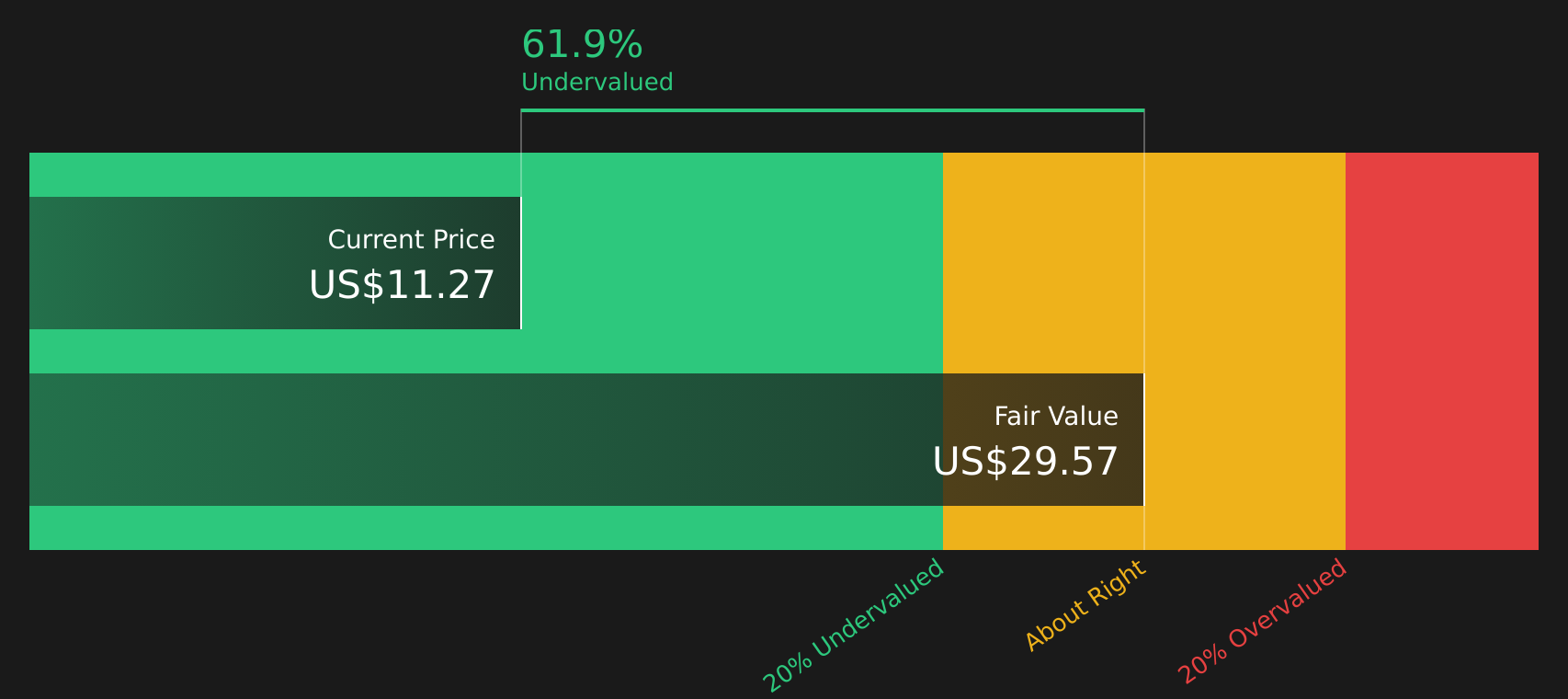

At a share price of $8.39, InnovAge Holding has seen short term share price pressure, with a 7 day share price return of a 4.22% decline, alongside strong recent momentum reflected in a 90 day share price return of 51.17% and a 1 year total shareholder return of 155.79%. This points to a stock where sentiment has shifted meaningfully over the past year.

If this shift in sentiment has you looking beyond a single name, it could be a good moment to broaden your search and discover 20 top founder-led companies

With InnovAge Holding trading at $8.39, a very large intrinsic value discount estimate of about 71% and a market cap of roughly US$1.1b sit alongside a price that is already above the average analyst target of $7. So is the market still underestimating the company, or are investors already paying up for the growth that analysts see ahead?

Most Popular Narrative: 19.9% Overvalued

The most followed valuation narrative puts InnovAge Holding’s fair value at $7, compared with the latest close at $8.39, framing the current price as meaningfully above that estimate while still grounded in detailed earnings and revenue work.

Enrollment growth and efficient geographic expansion are positioning the company for sustained revenue gains and scalable growth. Operational improvements and alignment with value-based care are driving margin improvements and better medical expense control.

Curious what kind of revenue profile and profit margins could support that $7 fair value with a higher future earnings multiple and a specific discount rate baked in? The narrative leans on a defined path for earnings to move from losses to sustained profitability and assumes investors will accept a richer valuation on those future numbers. The exact hurdles built into those projections might surprise you.

Result: Fair Value of $7 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, this depends on effective execution, as rising costs are outpacing revenue and newly opened centers are generating losses, which could pressure margins and challenge those upbeat assumptions.

Find out about the key risks to this InnovAge Holding narrative.

Another View: DCF Points in the Opposite Direction

While the popular narrative frames InnovAge Holding as 19.9% overvalued at $8.39 versus a $7 fair value, our DCF model presents a very different perspective, with an estimated future cash flow value of $28.96, implying a very large discount. Which story do you find more convincing?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out InnovAge Holding for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 49 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With sentiment clearly split between risk and reward, it makes sense to move quickly and test the numbers yourself before opinions harden. To weigh up the company’s potential against the concerns on the table, start by reviewing its 3 key rewards and 2 important warning signs

Looking for more investment ideas?

If InnovAge has sharpened your thinking, do not stop there. Use powerful screeners to quickly surface other opportunities that fit your style and risk appetite.

- Spot potential value plays early by scanning 49 high quality undervalued stocks and see which companies combine quality fundamentals with prices that may not fully reflect them.

- Prioritise resilience by checking 74 resilient stocks with low risk scores so you can focus your research on companies with comparatively lower overall risk profiles.

- Hunt for under-the-radar opportunities through the screener containing 26 high quality undiscovered gems and see which lesser known names show strong underlying fundamentals.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com