RB Global (RBA) has put a new US$500 million share repurchase plan on the table, targeting up to 10,000,000 shares. The move immediately shifts attention to capital allocation and shareholder returns.

See our latest analysis for RB Global.

The buyback news comes after a softer period for the shares, with a 7 day share price return of 6.72% and a 90 day share price return of 5.29%. In contrast, the 3 year total shareholder return of 99.05% and 5 year total shareholder return of 91.35% indicate a much stronger longer term picture.

If this kind of capital return profile has your attention, it could be a good moment to widen your search and check out 20 top founder-led companies

With the shares now around US$98.68 and internal estimates pointing to an intrinsic value gap, alongside a 31% discount to the average analyst target of US$129.40, you have to ask: is there a buying opportunity here, or is the market already pricing in future growth?

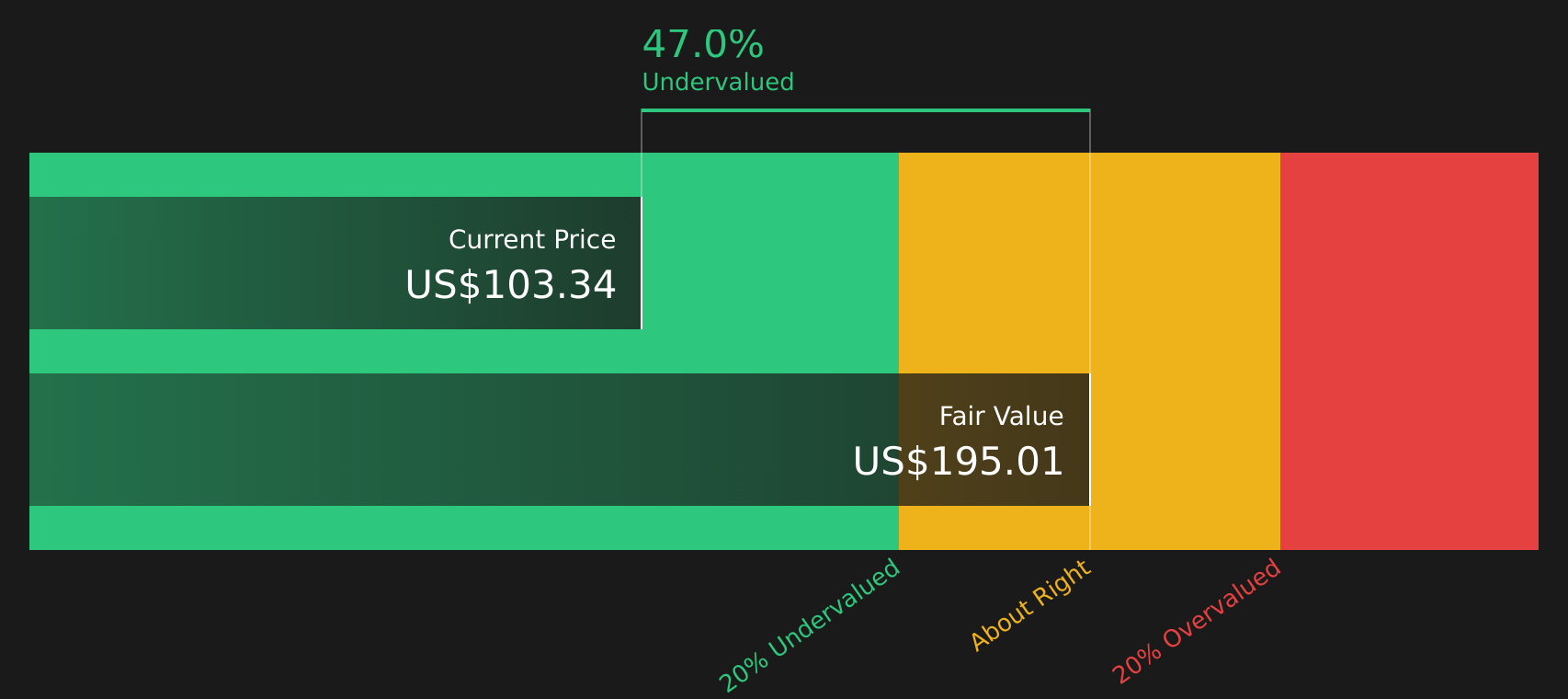

Most Popular Narrative: 20.5% Undervalued

RB Global's most followed narrative pegs fair value at about $124.20 per share, comfortably above the last close of $98.68, which is what underpins the recent optimism around the name.

Expansion of the international buyer base and new alliance partnerships, along with ongoing growth in e-commerce marketplace activities, are expected to drive higher transaction volumes and revenue as more asset sales and auctions move online.

Want to see what is backing that valuation gap? The narrative focuses on earnings growth, margins and a future earnings multiple that assumes real staying power.

Result: Fair Value of $124.20 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, you still need to weigh up headwinds such as subdued transaction volumes from macro pressures and the risk that direct digital sales platforms chip away at auction margins.

Find out about the key risks to this RB Global narrative.

Another Angle On What The Market Is Paying For RBA

While the SWS DCF model suggests RBA is trading at a wide discount to its future cash flow value of $198.30, the current P/E of 48x is high relative to the estimated fair ratio of 31.2x. That gap points to meaningful valuation risk if sentiment cools.

Look into how the SWS DCF model arrives at its fair value.

Next Steps

The tone here is cautiously positive. If you feel the clock is ticking, go straight to the underlying data and weigh it up for yourself with 4 key rewards.

Looking for more investment ideas?

If RB Global is on your radar, do not stop there. A few focused stock lists could surface opportunities that fit your style before others notice.

- Target potential mispricing by scanning for quality companies trading below estimates of worth with the 49 high quality undervalued stocks.

- Secure potential cash flow by hunting for companies with higher yields and resilient payouts through the 14 dividend fortresses.

- Prioritize resilience by focusing on businesses that pair financial strength with consistent fundamentals using the solid balance sheet and fundamentals stocks screener (42 results).

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com