- In March 2026, IQVIA Holdings Inc. announced at NVIDIA GTC the launch of IQVIA.ai, a unified agentic AI platform built with NVIDIA technologies to embed healthcare-grade AI into life sciences workflows across clinical, commercial and real-world domains, while aligning with strict regulatory and privacy standards.

- By positioning IQVIA.ai as a secure, workflow-embedded “digital command center” that orchestrates specialized AI agents rather than offering a generic tool, IQVIA is aiming to deepen its role at the core of how life sciences clients run research and decision-making processes.

- Next, we’ll explore how IQVIA.ai’s NVIDIA-powered, workflow-embedded design could influence IQVIA’s existing investment narrative around AI-driven differentiation.

Capitalize on the AI infrastructure supercycle with our selection of the 33 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

IQVIA Holdings Investment Narrative Recap

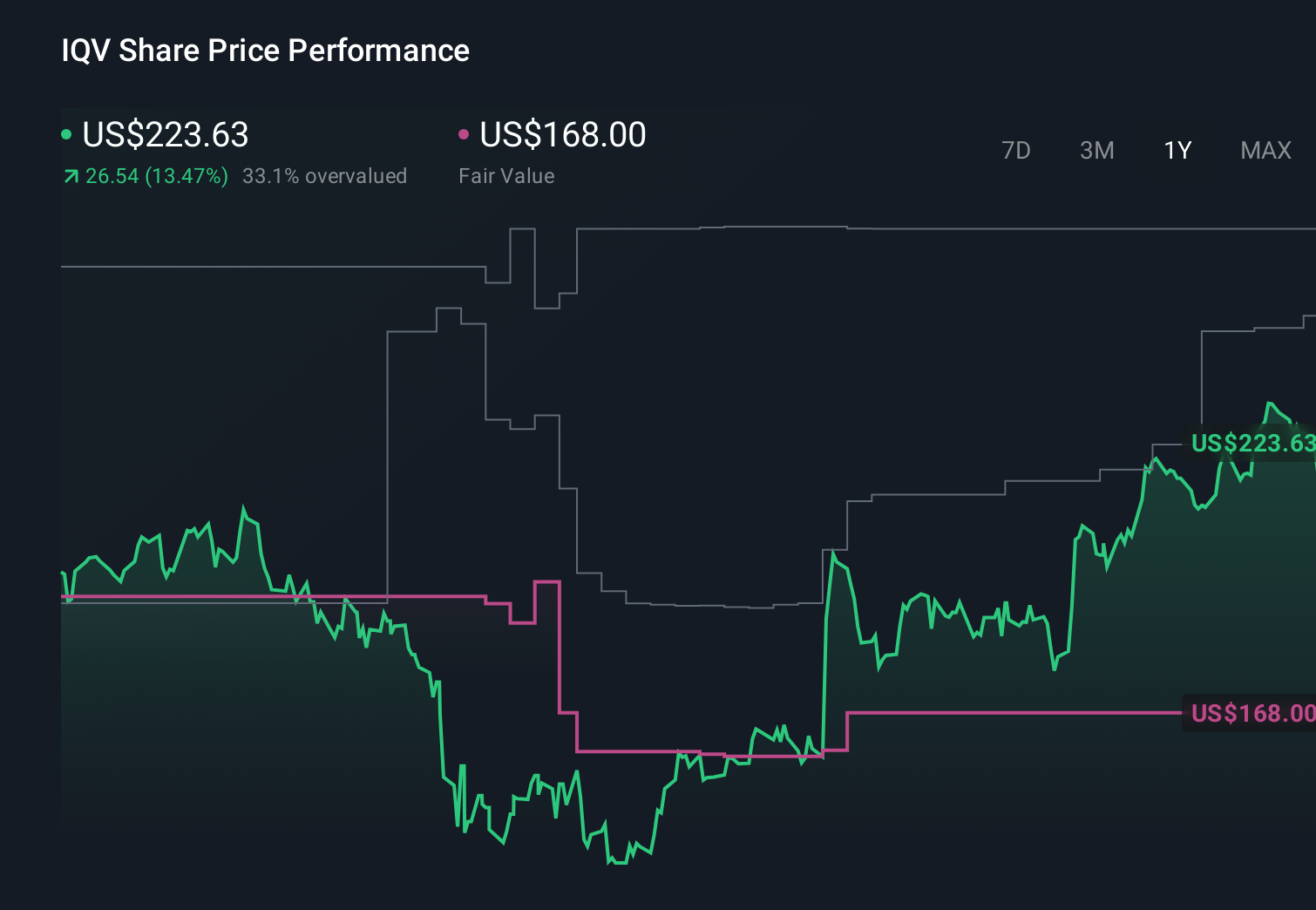

To own IQVIA, you need to believe its scale in data, clinical research, and software can offset pricing pressure, regulation, and high leverage. The IQVIA.ai launch fits that story by reinforcing the AI-driven differentiation catalyst, but it does not directly change the nearer term risks around margin pressure, client budget uncertainty, or the company’s elevated debt load.

Among recent developments, the February 2026 guidance for full year 2026 revenue of US$17,150 million to US$17,350 million is most relevant. It framed expectations for growth and margins before IQVIA.ai was announced, so investors now have to weigh whether this NVIDIA-powered, workflow-embedded platform eventually supports that outlook or mainly raises new questions about execution, capital intensity, and return on past AI investments.

But against this AI opportunity, investors should be aware that IQVIA’s high leverage and data privacy exposure could...

Read the full narrative on IQVIA Holdings (it's free!)

IQVIA Holdings’ narrative projects $18.4 billion revenue and $1.8 billion earnings by 2028. This requires 5.4% yearly revenue growth and a $0.6 billion earnings increase from $1.2 billion today.

Uncover how IQVIA Holdings' forecasts yield a $250.00 fair value, a 52% upside to its current price.

Exploring Other Perspectives

The most cautious analysts were already assuming only about 5 percent annual revenue growth and earnings of roughly US$1.6 billion by 2028, so if you worry about tighter data privacy rules limiting AI and data monetization, their more pessimistic view shows how far opinions can differ and why it is worth comparing several narratives as IQVIA.ai is digested.

Explore 4 other fair value estimates on IQVIA Holdings - why the stock might be worth just $250.00!

Reach Your Own Conclusion

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your IQVIA Holdings research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

- Our free IQVIA Holdings research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate IQVIA Holdings' overall financial health at a glance.

Searching For A Fresh Perspective?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 21 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

- Find 47 companies with promising cash flow potential yet trading below their fair value.

- Uncover the next big thing with 33 elite penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com