- Seadrill Limited recently reported that Sonadrill Holding Ltd, its 50:50 joint venture with a Sonangol affiliate, secured a seven-well priced option extension for the ultra-deepwater drillship Sonangol Quenguela in Angola, adding about 480 days of work and keeping the rig committed into June 2028.

- This extension not only lengthens operational activity in a key deepwater basin but also enhances visibility for the management fees Seadrill earns by providing management, operational and technical support to the joint venture.

- Next, we’ll examine how locking in the Sonangol Quenguela through mid-2028 may influence Seadrill’s investment narrative and perceived earnings resilience.

Find 49 companies with promising cash flow potential yet trading below their fair value.

Seadrill Investment Narrative Recap

To own Seadrill, you need to believe that tight supply of high spec deepwater rigs and a growing offshore backlog can gradually translate into more stable earnings, despite the company still posting net losses. The Sonangol Quenguela extension modestly improves near term visibility in Angola and partially offsets the risk of idle time and softer utilization, but it does not remove the broader pressure on day rates or the legal and regulatory uncertainties that still hang over the story.

Among recent announcements, the one year priced option exercised by Equinor Brasil for the West Saturn, adding about US$114 million of backlog and extending work through October 2027, is most relevant. Together with the Quenguela extension, it reinforces Seadrill’s push to secure multi year work for its ultra deepwater fleet, which matters for the key catalyst of improving backlog quality and earnings resilience, while still leaving open questions about older or idle rigs and future capital allocation.

Yet even with these contracts extending into 2028, investors should be aware that...

Read the full narrative on Seadrill (it's free!)

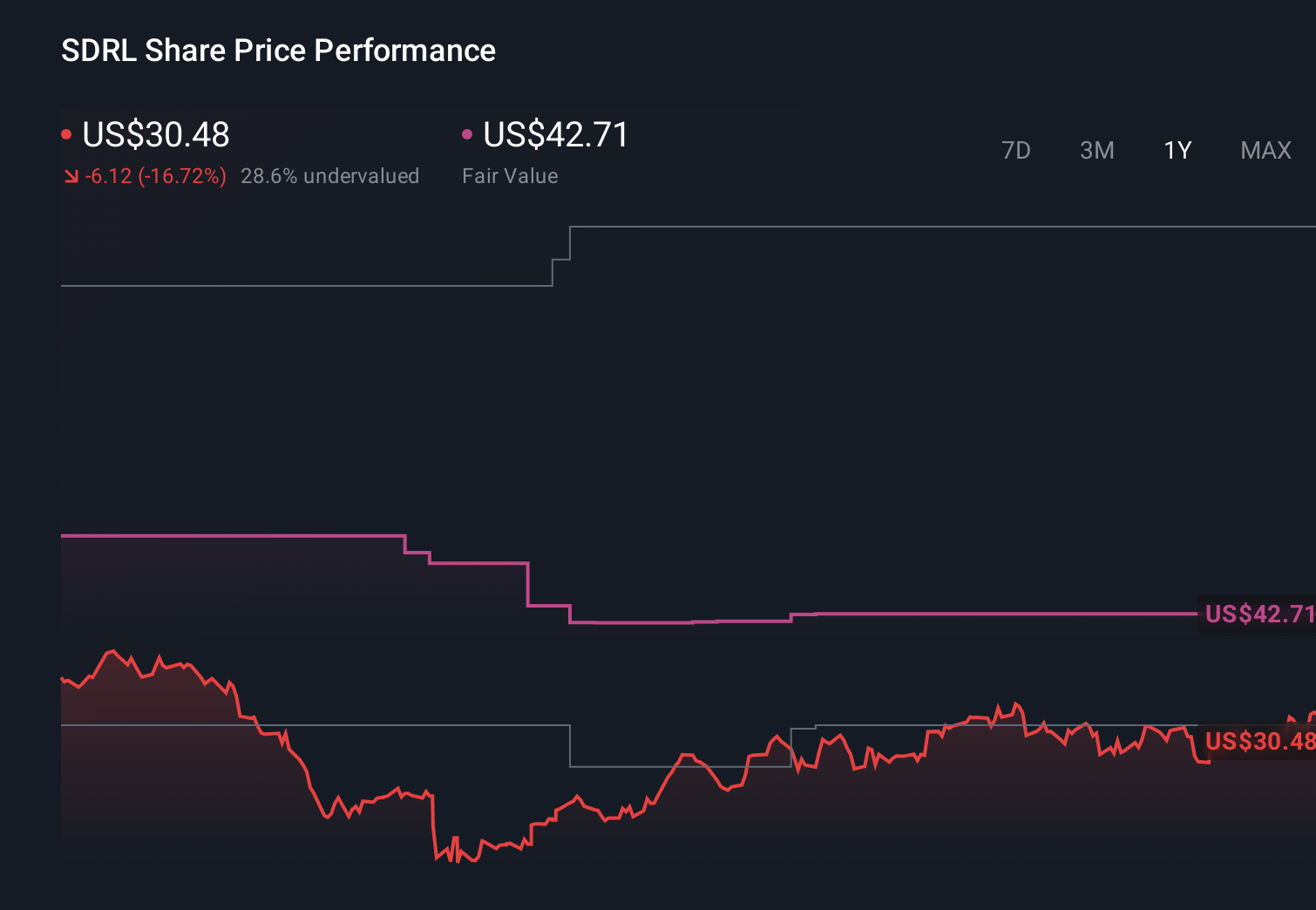

Seadrill’s narrative projects $1.6 billion revenue and $231.6 million earnings by 2028. This requires 7.2% yearly revenue growth and a $154.6 million earnings increase from $77.0 million today.

Uncover how Seadrill's forecasts yield a $43.50 fair value, a 4% downside to its current price.

Exploring Other Perspectives

Some of the lowest estimate analysts took a far more cautious view, assuming only about US$1.5 billion of revenue and US$187.5 million of earnings by 2028, highlighting how concerns about long term contract risk and political delays can look very different depending on your assumptions, and suggesting that new deals like Sonangol Quenguela’s extension could still shift those expectations over time.

Explore 6 other fair value estimates on Seadrill - why the stock might be worth just $43.50!

Decide For Yourself

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Seadrill research is our analysis highlighting 2 key rewards that could impact your investment decision.

- Our free Seadrill research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Seadrill's overall financial health at a glance.

Ready For A Different Approach?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- Outshine the giants: these 22 early-stage AI stocks could fund your retirement.

- Capitalize on the AI infrastructure supercycle with our selection of the 34 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- We've uncovered the 15 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com