- Earlier this month, EMCOR Group presented at the 2026 Cantor Global Technology & Industrial Growth Conference in New York, with senior leadership including CEO Tony Guzzi, CFO Jason Nalbandian, and FP&A Director Lucas Sullivan outlining the company’s latest business and financial updates.

- Since then, EMCOR has reported revenue and earnings per share ahead of analyst expectations, prompting upward revisions to earnings estimates and drawing increased attention to the company’s operating performance and outlook.

- We’ll now examine how EMCOR’s recent earnings beat and upward estimate revisions may influence its existing investment narrative and risk profile.

Capitalize on the AI infrastructure supercycle with our selection of the 34 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

EMCOR Group Investment Narrative Recap

To own EMCOR Group, you need to believe in its ability to convert a large, diversified project and service portfolio into resilient earnings, despite labor, regulatory, and end market cyclicality. The recent earnings beat and upward estimate revisions appear to reinforce the near term earnings catalyst around execution on backlog and margin discipline. They do not materially change the biggest risk right now, which remains cost pressure and project volatility in more cyclical industrial and high tech segments.

Among recent announcements, the most relevant alongside the earnings beat is EMCOR’s updated 2026 guidance, which frames expectations for US$17.75 billion to US$18.50 billion of revenue and a 9.0% to 9.4% operating margin. For investors focused on how the company converts its record backlog and capital returns into sustainable earnings, this guidance provides a reference point for assessing whether the latest results and analyst upgrades reflect durable progress or more cyclical strength.

Yet beneath this strong execution, a key risk investors should be aware of is how persistent labor cost pressures could eventually...

Read the full narrative on EMCOR Group (it's free!)

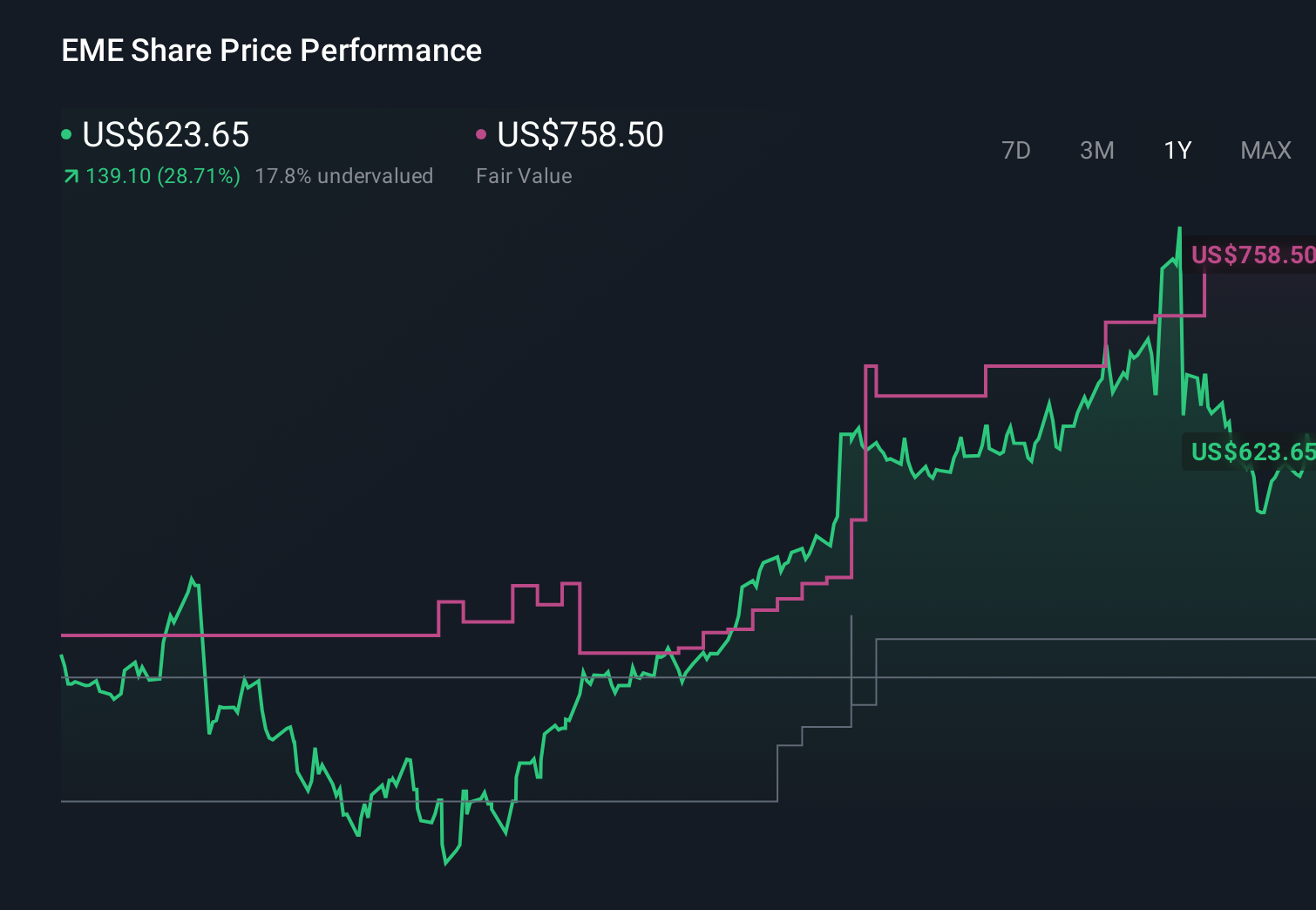

EMCOR Group's narrative projects $20.6 billion revenue and $1.4 billion earnings by 2028.

Uncover how EMCOR Group's forecasts yield a $869.29 fair value, a 19% upside to its current price.

Exploring Other Perspectives

Some of the lowest analysts were already cautious, assuming revenue near US$19.5 billion and earnings of about US$1.4 billion by 2028, and your view on whether automation and prefabrication threaten EMCOR’s traditional service demand could lead you to a very different conclusion about how this latest earnings beat might reshape those expectations.

Explore 7 other fair value estimates on EMCOR Group - why the stock might be worth as much as 26% more than the current price!

Form Your Own Verdict

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your EMCOR Group research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

- Our free EMCOR Group research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate EMCOR Group's overall financial health at a glance.

Ready To Venture Into Other Investment Styles?

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

- We've uncovered the 15 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- Invest in the nuclear renaissance through our list of 87 elite nuclear energy infrastructure plays powering the global AI revolution.

- Uncover the next big thing with 33 elite penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com