- Trinity Industries has declared a quarterly dividend of US$0.31 per share on its US$0.01 par value common stock, marking its 248th consecutive dividend payment and scheduled for payment on April 30, 2026 to holders of record as of April 15, 2026.

- The dividend affirmation comes shortly after Trinity delivered full-year 2025 results that exceeded revenue expectations and improved EPS through higher lease rates, lease portfolio sale gains, lower administrative costs, and a non-cash benefit from restructuring a railcar partnership.

- We’ll now examine how Trinity’s stronger-than-expected revenues and EPS, helped by lease portfolio sales and cost efficiencies, influence its investment narrative.

Invest in the nuclear renaissance through our list of 87 elite nuclear energy infrastructure plays powering the global AI revolution.

Trinity Industries Investment Narrative Recap

To own Trinity Industries, you need to believe in the long term role of rail in North American freight and Trinity’s ability to earn through cycles despite heavy exposure to energy and agriculture demand. The latest dividend affirmation and stronger 2025 earnings do not materially change the near term picture, where the key catalyst is railcar replacement and leasing demand, while the biggest risk remains a downturn or prolonged pause in customer capital spending that slows new orders and leasing activity.

The most relevant recent development here is Trinity’s full year 2025 earnings beat, with higher EPS supported by stronger lease rates, gains on lease portfolio sales, and lower administrative costs. While the one off benefits from portfolio and partnership actions helped results, they sit alongside the core catalyst of an improving railcar market, and investors will be weighing how sustainable these earnings drivers are if secondary leasing market conditions or customer investment appetites shift.

Yet beneath the steady dividend record, investors should be aware of how reliant recent EPS has been on one off gains and...

Read the full narrative on Trinity Industries (it's free!)

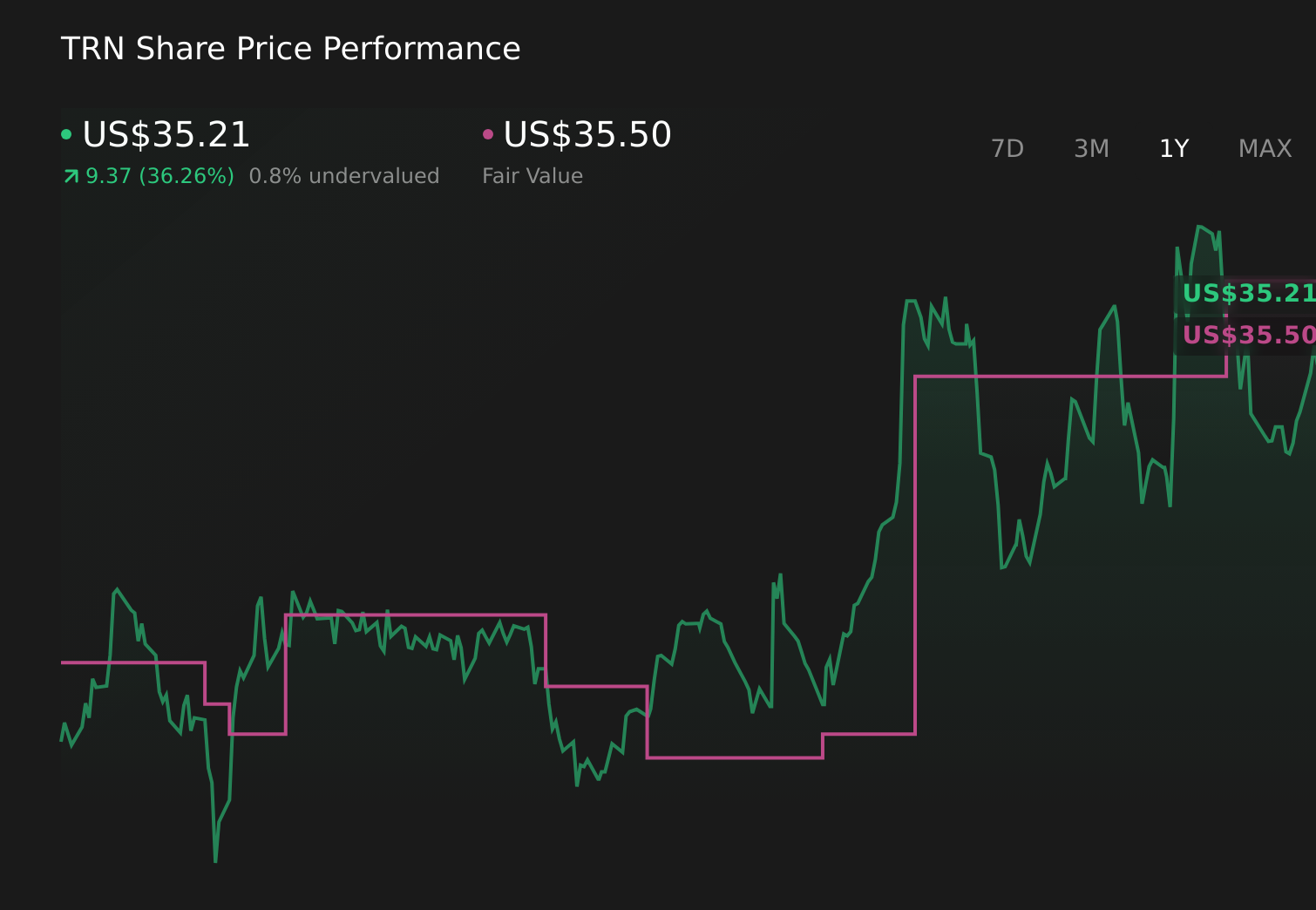

Trinity Industries' narrative projects $2.6 billion revenue and $207.4 million earnings by 2028. This requires 1.3% yearly revenue growth and about a $98.8 million earnings increase from $108.6 million today.

Uncover how Trinity Industries' forecasts yield a $33.50 fair value, a 10% upside to its current price.

Exploring Other Perspectives

Two fair value estimates from the Simply Wall St Community cluster in a tight US$33.50 to US$35.71 range, underscoring how differently individual investors can see the same stock. You can weigh those views against the current reliance on secondary leasing gains and consider how a weaker railcar market or slower customer spending could affect Trinity’s future performance.

Explore 2 other fair value estimates on Trinity Industries - why the stock might be worth as much as 17% more than the current price!

Decide For Yourself

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Trinity Industries research is our analysis highlighting 3 key rewards and 4 important warning signs that could impact your investment decision.

- Our free Trinity Industries research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Trinity Industries' overall financial health at a glance.

Ready To Venture Into Other Investment Styles?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

- Find 49 companies with promising cash flow potential yet trading below their fair value.

- AI is about to change healthcare. These 36 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Uncover the next big thing with 33 elite penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com