- Earlier in 2026, First Advantage released its 2026 Trends Report showing that most US employers now prioritize speed in background screening, while also planning to add more screening and identity verification tools to counter rising identity fraud.

- This report highlights a growing tension for employers between faster hiring and increasingly complex verification needs, an area where First Advantage is emphasizing technology and automation to offer more comprehensive solutions.

- Next, we'll examine how this stronger employer focus on faster, more comprehensive screening could influence First Advantage's existing investment narrative.

The latest GPUs need a type of rare earth metal called Dysprosium and there are only 28 companies in the world exploring or producing it. Find the list for free.

First Advantage Investment Narrative Recap

To own First Advantage, you need to believe that employers will keep outsourcing faster, tech driven background checks and identity verification, and that the company can turn that demand into sustainable profits despite intense competition and uneven hiring cycles. The 2026 Trends Report reinforces the near term catalyst of employer demand for speed and fraud prevention, but it does not remove the key risk that weaker hiring volumes or pricing pressure could still weigh on results.

Among recent announcements, the new US$100,000,000 share repurchase authorization stands out alongside this report. While buybacks do not change the core business, they matter in the context of a company working through integration challenges and uneven profitability, because they signal how management is choosing to use cash at a time when investors are focused on margin pressure, execution on the Sterling acquisition, and the path toward improved earnings quality.

Yet beneath the focus on faster screening, investors should be aware that profitability could still be pressured if Sterling’s lower margin mix and fixed costs...

Read the full narrative on First Advantage (it's free!)

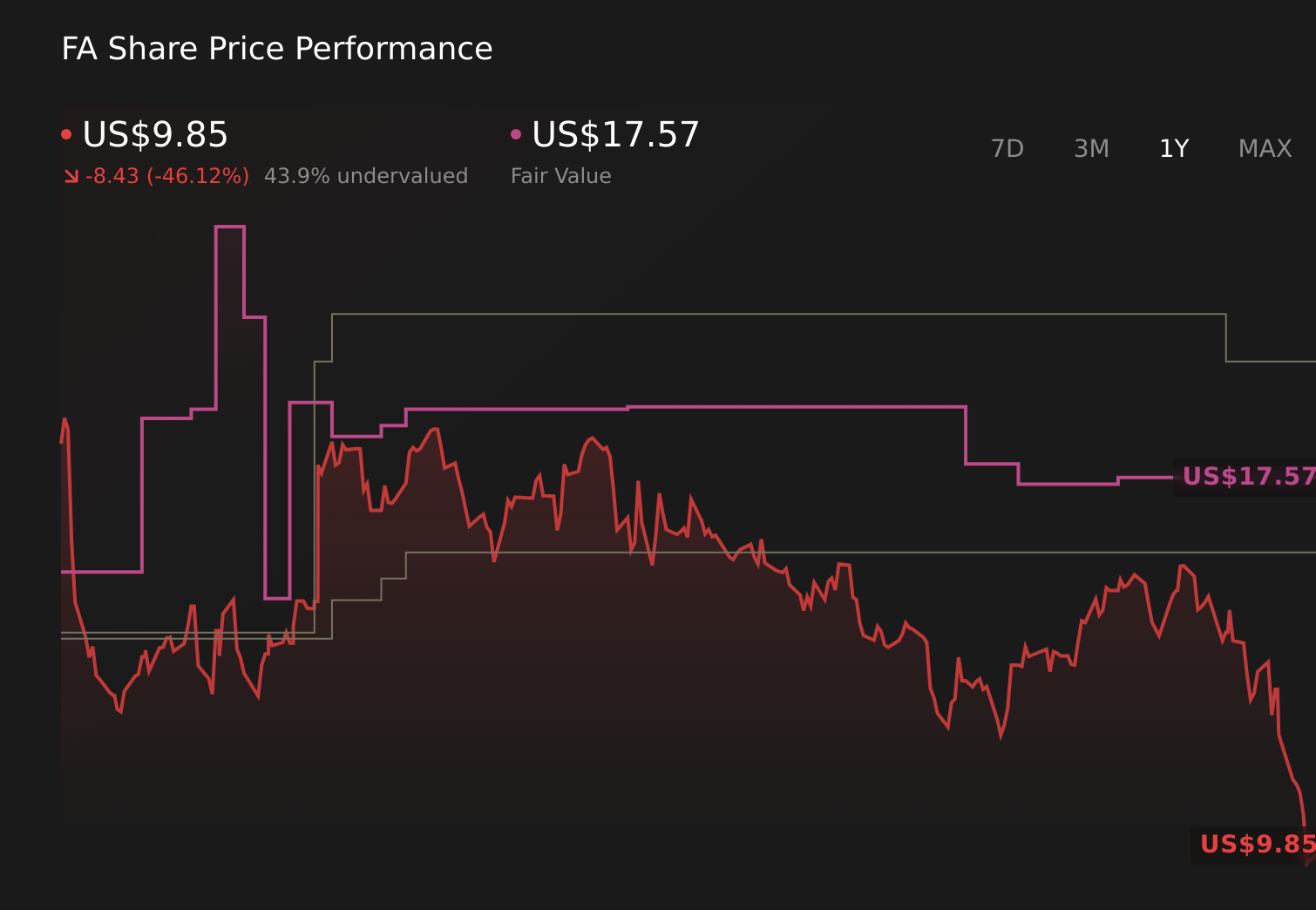

First Advantage’s narrative projects $1.9 billion revenue and $143.4 million earnings by 2028.

Uncover how First Advantage's forecasts yield a $17.57 fair value, a 65% upside to its current price.

Exploring Other Perspectives

Some of the lowest analysts were already cautious, assuming revenue of about US$1.7 billion and earnings near US$95.0 million by 2028, and the latest trends report could either soften or sharpen those concerns depending on how it affects perceptions of Sterling’s margin drag and the timing of any improvement.

Explore another fair value estimate on First Advantage - why the stock might be worth as much as 65% more than the current price!

Form Your Own Verdict

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your First Advantage research is our analysis highlighting 3 key rewards that could impact your investment decision.

- Our free First Advantage research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate First Advantage's overall financial health at a glance.

Interested In Other Possibilities?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- AI is about to change healthcare. These 35 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Outshine the giants: these 22 early-stage AI stocks could fund your retirement.

- Find 49 companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com